SunTrust 2011 Annual Report Download - page 196

Download and view the complete annual report

Please find page 196 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

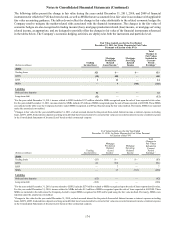

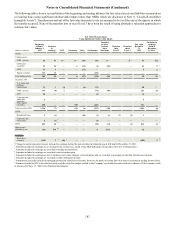

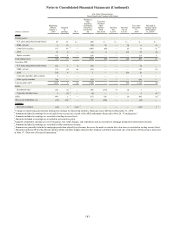

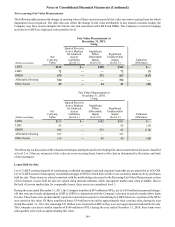

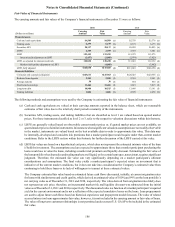

Notes to Consolidated Financial Statements (Continued)

180

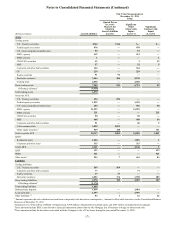

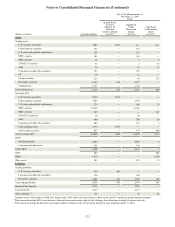

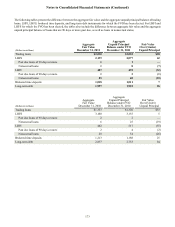

million, respectively, due to changes in fair value attributable to borrower-specific credit risk. In addition to borrower-

specific credit risk, there are other, more significant, variables that drive changes in the fair values of the loans, including

interest rates and general conditions in the principal markets for the loans.

Corporate and other LHFS

As discussed in Note 11, “Certain Transfers of Financial Assets and Variable Interest Entities,” the Company has

determined that it is the primary beneficiary of a CLO vehicle, which resulted in the Company consolidating the loans

of that vehicle. Because the CLO trades its loans from time to time and in order to fairly present the economics of the

CLO, the Company elected to carry the loans of the CLO at fair value. The Company is able to obtain fair value estimates

for substantially all of these loans using a third party valuation service that is broadly used by market participants. While

most of the loans are traded in the markets, the Company does not believe the loans qualify as level 1 instruments, as the

volume and level of trading activity is subject to variability and the loans are not exchange-traded, such that the Company

believes that level 2 is more representative of the general market activity for the loans.

LHFI

Level 3 LHFI predominantly includes mortgage loans that have been deemed not marketable, largely due to borrower

defaults or the identification of other loan defects. The Company values these loans using a discounted cash flow approach

based on assumptions that are generally not observable in the current markets, such as prepayment speeds, default rates,

loss severity rates, and discount rates.

Other Intangible Assets

Other intangible assets that the Company records at fair value are the Company’s MSR assets. The fair values of MSRs are

determined by projecting cash flows, which are then discounted to estimate an expected fair value. The fair values of MSRs are

impacted by a variety of factors, including prepayment assumptions, discount rates, delinquency rates, contractually specified

servicing fees, servicing costs, and underlying portfolio characteristics. For additional information, see Note 9, "Goodwill and

Other Intangible Assets." The underlying assumptions and estimated values are corroborated by values received from independent

third parties based on their review of the servicing portfolio. Because these inputs are not transparent in market trades, MSRs are

considered to be level 3 assets.

Other Assets/Liabilities, net

The Company’s other assets/liabilities that are carried at fair value on a recurring basis include IRLCs that satisfy the criteria to

be treated as derivative financial instruments, derivative financial instruments that are used by the Company to economically hedge

certain loans and MSRs, and the derivative that the Company obtained as a result of its sale of Visa Class B shares.

The fair value of IRLCs on residential mortgage LHFS, while based on interest rates observable in the market, is highly dependent

on the ultimate closing of the loans. These “pull-through” rates are based on the Company’s historical data and reflect the Company’s

best estimate of the likelihood that a commitment will ultimately result in a closed loan. Servicing value is included in the fair

value of IRLCs, and the fair value of servicing is determined by projecting cash flows which are then discounted to estimate an

expected fair value. The fair value of servicing is impacted by a variety of factors, including prepayment assumptions, discount

rates, delinquency rates, contractually specified servicing fees, servicing costs, and underlying portfolio characteristics. Because

these inputs are not transparent in market trades, IRLCs are considered to be level 3 assets.

During the years ended December 31, 2011 and 2010, the Company transferred $271 million and $398 million, respectively, of

IRLCs out of level 3 as the associated loans were closed.

The Company is exposed to interest rate risk associated with MSRs, IRLCs, mortgage LHFS, and mortgage LHFI reported at fair

value. The Company hedges these exposures with a combination of derivatives, including MBS forward and option contracts,

interest rate swap and swaption contracts, futures contracts, and eurodollar options. The Company estimates the fair values of

such derivative instruments consistent with the methodologies discussed herein under “Derivative contracts” and accordingly

these derivatives are considered to be level 2 instruments.

During the second quarter of 2009, in connection with its sale of Visa Class B shares, the Company entered into a derivative

contract whereby the ultimate cash payments received or paid, if any, under the contract are based on the ultimate resolution of

litigation involving Visa. The value of the derivative was estimated based on the Company’s expectations regarding the ultimate

resolution of that litigation, which involved a high degree of judgment and subjectivity. Accordingly, the value of the derivative

liability was classified as a level 3 instrument.