SunTrust 2011 Annual Report Download - page 121

Download and view the complete annual report

Please find page 121 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

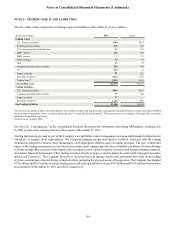

Notes to Consolidated Financial Statements (Continued)

105

Securities and Trading Activities

Securities are classified at trade date as trading or securities AFS. Trading account assets and liabilities are carried at fair value

with changes in fair value recognized within noninterest income. Realized and unrealized gains and losses are recognized as a

component of noninterest income in the Consolidated Statements of Income/(Loss). Securities AFS are used as part of the overall

asset and liability management process to optimize income and market performance over an entire interest rate cycle. Interest

income and dividends on securities are recognized in interest income on an accrual basis. Premiums and discounts on debt securities

are amortized as an adjustment to yield over the estimated life of the security. Securities AFS are carried at fair value with unrealized

gains and losses, net of any tax effect, included in AOCI as a component of shareholders’ equity. Realized gains and losses,

including OTTI, are determined using the specific identification method and are recognized as a component of noninterest income

in the Consolidated Statements of Income/(Loss).

On a quarterly basis, securities AFS are reviewed for possible OTTI. In determining whether OTTI exists for securities in an

unrealized loss position, the Company assesses whether it has the intent to sell the security or, for debt securities, the Company

assesses the likelihood of selling the security prior to the recovery of its amortized cost basis. If the Company intends to sell the

debt security or it is more-likely-than-not that the Company will be required to sell the debt security prior to the recovery of its

amortized cost basis, the debt security is written down to fair value, and the full amount of any impairment charge is recognized

as a component of noninterest income in the Consolidated Statements of Income/(Loss). If the Company does not intend to sell

the debt security and it is more-likely-than-not that the Company will not be required to sell the debt security prior to recovery of

its amortized cost basis, only the credit component of any impairment of a debt security is recognized as a component of noninterest

income in the Consolidated Statements of Income/(Loss), with the remaining impairment recorded in OCI.

The OTTI review for equity securities includes an analysis of the facts and circumstances of each individual investment and focuses

on the severity of loss, the length of time the fair value has been below cost, the expectation for that security's performance, the

financial condition and near-term prospects of the issuer, and management's intent and ability to hold the security to recovery. A

decline in value of an equity security that is considered to be other-than-temporary is recognized as a component of noninterest

income in the Consolidated Statements of Income/(Loss).

On a quarterly basis, the Company reviews nonmarketable equity securities, which include venture capital equity and certain

mezzanine securities that are not publicly traded as well as equity investments acquired for various purposes. These securities are

accounted for under the cost or equity method and are included in other assets. The Company reviews nonmarketable securities

accounted for under the cost method on a quarterly basis and reduces the asset value when declines in value are considered to be

other-than-temporary. Equity method investments are recorded at cost, adjusted to reflect the Company’s portion of income, loss

or dividends of the investee. Realized income, realized losses and estimated other-than-temporary unrealized losses on cost and

equity method investments are recognized in noninterest income in the Consolidated Statements of Income/(Loss).

For additional information on the Company’s securities activities, see Note 5, “Securities Available for Sale.”

Securities Sold Under Repurchase Agreements

Securities sold under agreements to repurchase are accounted for as collateralized financing transactions and are recorded at the

amounts at which the securities were sold, plus accrued interest. The fair value of collateral pledged is continually monitored and

additional collateral is pledged or requested to be returned to the Company as deemed appropriate. For additional information on

the collateral pledged to secure repurchase agreements, see Note 4, "Trading Assets and Liabilities," and Note 5, "Securities

Available for Sale."

Loans Held for Sale

The Company’s LHFS generally includes certain residential mortgage loans, commercial loans, and student loans. Loans are

initially classified as LHFS when they are identified as being available for immediate sale and a formal plan exists to sell them.

LHFS are recorded at either fair value, if elected, or the lower of cost or fair value on an individual loan basis. Origination fees

and costs for LHFS recorded at LOCOM are capitalized in the basis of the loan and are included in the calculation of realized

gains and losses upon sale. Origination fees and costs are recognized in earnings at the time of origination for LHFS that are

recorded at fair value. Fair value is derived from observable current market prices, when available, and includes loan servicing

value. When observable market prices are not available, the Company uses judgment and estimates fair value using internal models,

in which the Company uses its best estimates of assumptions it believes would be used by market participants in estimating fair

value. Adjustments to reflect unrealized gains and losses resulting from changes in fair value and realized gains and losses upon

ultimate sale of the loans are classified as noninterest income in the Consolidated Statements of Income/(Loss).