SunTrust 2011 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

87

declined due to a fourth quarter 2011 reduction in incentive expense based upon our full year financial performance. Other

noninterest expense increased by $53 million from the fourth quarter of 2010. This increase included a $27 million accrual in

other staff expense, which was related to severance expense associated with our PPG Expense Program, a $14 million increase in

consulting fees associated with the Consent Order, and a $7 million increase in mortgage insurance expense.

The income tax benefit for the fourth quarter of 2011 was $57 million, compared with the income tax provision of $45 million for

the fourth quarter of 2010. The decrease in the income tax provision was primarily the result of a decline in pre-tax income adjusted

for net favorable permanent tax items, such as interest income from lending to tax-exempt entities and federal tax credits from

community reinvestment activities in addition to favorable discrete items.

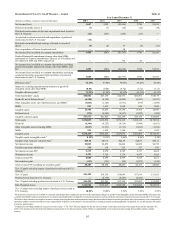

BUSINESS SEGMENTS

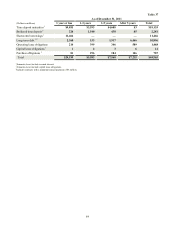

The following table presents net income/(loss) for our reportable business segments for the years ended December 31:

Net Income/(Loss) by Segment

(Dollars in millions)

Retail Banking

Diversified Commercial Banking

CRE

CIB

Mortgage

W&IM

Corporate Other and Treasury

2011

$193

269

(310)

355

(693)

160

447

2010

$73

203

(329)

320

(787)

138

489

Table 39

2009

($203)

157

(591)

117

(975)

100

381

The following table presents average loans and average deposits for our reportable business segments for the years ended December

31:

Average Loans and Deposits by Segment

(Dollars in millions)

Retail Banking

Diversified Commercial Banking

CRE

CIB

Mortgage

W&IM

Corporate Other and Treasury

Average Loans

2011

$35,648

23,097

7,045

13,717

29,128

7,503

170

2010

$33,511

22,571

9,704

10,876

29,043

8,015

205

2009

$33,156

24,396

12,509

12,843

29,599

8,346

192

Average Consumer and Commercial Deposits

2011

$76,751

19,519

1,541

8,511

3,084

12,349

917

2010

$75,143

18,539

1,546

6,723

3,135

11,315

728

Table 40

2009

$72,751

17,652

1,885

5,855

3,134

11,185

702

See Note 21, “Business Segment Reporting,” to the Consolidated Financial Statements in this Form 10-K for discussion of our

segment structure, basis of presentation and internal management reporting methodologies.

BUSINESS SEGMENT RESULTS

Twelve Months Ended December 31, 2011 vs. 2010

Retail Banking

Retail Banking reported net income of $193 million for the twelve months ended December 31, 2011, an increase of $120 million,

compared with the same period in 2010. The increase in net income was predominantly due to lower provision for credit losses

and higher net interest income that was partially offset by lower noninterest income.

Net interest income was $2.5 billion, an increase of $43 million, or 2%, from the same period in 2010. The increase was driven

by the benefits derived from higher average loan balances and higher average deposit balances, partially offset by the impact of

lower deposit spreads. Average loan balances increased $2.1 billion, or 6%. Indirect installment loans increased $2.2 billion, driven

by organic indirect auto production and by the acquisition of $1.7 billion of consumer auto loans in the third and fourth quarters

of 2010. Additional consumer loan growth was the result of the purchase of $1.6 billion of guaranteed student loans during the