SunTrust 2011 Annual Report Download - page 153

Download and view the complete annual report

Please find page 153 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

Notes to Consolidated Financial Statements (Continued)

137

consolidation for U.S. GAAP purposes. The liquidity commitments are revolving facilities that are sized based on the

current commitments provided by Three Pillars to its customers. The liquidity facilities may generally be used if new CP

cannot be issued by Three Pillars to repay maturing CP. However, the liquidity facilities are available in all circumstances,

except certain bankruptcy-related events with respect to Three Pillars. Draws on the facilities are subject to the purchase

price (or borrowing base) formula that, in many cases, excludes defaulted assets to the extent that they exceed available

over-collateralization in the form of non-defaulted assets, and may also provide the liquidity banks with loss protection

equal to a portion of the loss protection provided for in the related securitization agreement. Additionally, there are

transaction specific covenants and triggers that are tied to the performance of the assets of the relevant seller/servicer

that may result in a transaction termination event, which, if continuing, would require funding through the related liquidity

facility. Finally, in a termination event of Three Pillars, such as if its tangible net worth falls below $5,000 for a period

in excess of 15 days, Three Pillars would be unable to issue CP, which would likely result in funding through the liquidity

facilities. Draws under the credit enhancement are also available in all circumstances, but are generally used to the extent

required to make payment on any maturing CP if there are insufficient funds from collections of receivables or the use

of liquidity facilities. The required amount of credit enhancement at Three Pillars will vary from time to time as new

receivable pools are purchased or removed from its asset portfolio, but is generally equal to 10% of the aggregate

commitments of Three Pillars.

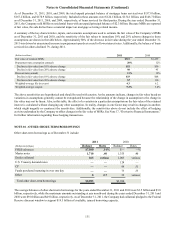

Due to the consolidation of Three Pillars, the Company’s maximum exposure to potential loss was $4.3 billion and $4.2

billion as of December 31, 2011 and 2010, respectively, which represents the Company’s exposure to the lines of credit

that Three Pillars had extended to its clients. The Company did not recognize any liability on its Consolidated Balance

Sheets related to the liquidity facilities and other credit enhancements provided to Three Pillars as of December 31, 2011

and 2010, as no amounts had been drawn, nor were any draws probable to occur, such that a loss should have been accrued.

In January 2012, the Company initiated the process of liquidating Three Pillars. The commitments and outstanding loans

of Three Pillars will be transferred to the Bank. The Bank will fund the loans through wholesale funding sources, and

Three Pillars' CP will be repaid in full. The liquidation is expected to be complete by the second quarter of 2012, and

upon completion, the Bank will terminate the liquidity arrangements and standby letter of credit. The liquidation is not

expected to have a material impact to the Company's financial condition, results of operations, or cash flows.

Total Return Swaps

The Company recommenced involvement with various VIEs related to its TRS business during 2010. Under the matched

book TRS business model, the VIEs purchase assets (typically loans) from the market, which are identified by third party

clients, that serve as the underlying reference assets for a TRS between the VIE and the Company and a mirror TRS

between the Company and its third party clients. The TRS contracts between the VIEs and the Company hedge the

Company’s exposure to the TRS contracts with its third party clients. These third parties are not related parties to the

Company, nor are they and the Company de facto agents of each other. In order for the VIEs to purchase the reference

assets, the Company provides senior financing, in the form of demand notes, to these VIEs. The TRS contracts pass

through interest and other cash flows on the assets owned by the VIEs to the third parties, along with exposing the third

parties to depreciation on the assets and providing them with the rights to appreciation on the assets. The terms of the

TRS contracts require the third parties to post initial collateral, in addition to ongoing margin as the fair values of the

underlying assets change. Although the Company has always caused the VIEs to purchase a reference asset in response

to the addition of a reference asset by its third party clients, there is no legal obligation between the Company and its

third party clients for the Company to purchase the reference assets or for the Company to cause the VIEs to purchase

the assets.

The Company considered the VIE consolidation guidance, which requires an evaluation of the substantive contractual

and non-contractual aspects of transactions involving VIEs established subsequent to January 1, 2010. The Company

and its third party clients are the only VI holders. As such, the Company evaluated the nature of all VIs and other interests

and involvement with the VIEs, in addition to the purpose and design of the VIEs, relative to the risks they were designed

to create. The purpose and design of a VIE are key components of a consolidation analysis and any power should be

analyzed based on the substance of that power relative to the purpose and design of the VIE. The VIEs were designed

for the benefit of the third parties and would not exist if the Company did not enter into the TRS contracts with the third

parties. The activities of the VIEs are restricted to buying and selling reference assets with respect to the TRS contracts

entered into between the Company and its third party clients and the risks/benefits of any such assets owned by the VIEs

are passed to the third party clients via the TRS contracts. The TRS contracts between the Company and its third party

clients have a substantive effect on the design of the overall transaction and the VIEs. Based on its evaluation, the Company

has determined that it is not the primary beneficiary of the VIEs, as the design of the TRS business results in the Company

having no substantive power to direct the significant activities of the VIEs.