SunTrust 2011 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

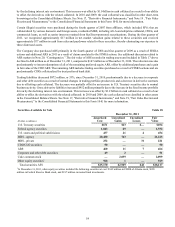

52

and/or deed-in-lieu arrangements. For loans secured by income producing commercial properties, we perform a rigorous and

ongoing programmatic review. We review a number of factors, including cash flows, loan structures, collateral values, and

guarantees, to identify loans within our income producing commercial loan portfolio that are most likely to experience distress.

Based on our review of these factors and our assessment of overall risk, we evaluate the benefits of proactively initiating

discussions with our clients to improve a loan’s risk profile. In some cases, we may renegotiate terms of their loans so that

they have a higher likelihood of continuing to perform. To date, we have restructured loans in a variety of ways to help our

clients service their debt and to mitigate the potential for additional losses. The primary restructuring methods being offered

to our residential clients are reductions in interest rates and extensions of terms. For commercial loans, the primary restructuring

method is the extensions of terms.

Accruing loans with modifications deemed to be economic concessions resulting from borrower difficulties are reported as

accruing TDRs. Nonaccruing loans that are modified and demonstrate a history of repayment performance in accordance with

their modified terms are reclassified to accruing restructured status, typically after six months of repayment performance.

Generally, once a residential loan becomes a TDR, we expect that the loan will likely continue to be reported as a TDR for

its remaining life even after returning to accruing status as the modified rates and terms at the time of modification were

typically more favorable than those generally available in the market. We note that some restructurings may not ultimately

result in the complete collection of principal and interest (as modified by the terms of the restructuring), culminating in default,

which could result in additional incremental losses. These potential incremental losses have been factored into our overall

ALLL estimate through the use of loss forecasting methodologies. Roll rate models used to forecast losses on the residential

mortgage and consumer TDRs are calculated and analyzed separately using their own portfolio attributes and history, thereby

reflecting an increased PD compared to loans that have not been restructured. The level of re-defaults will likely be affected

by future economic conditions. At December 31, 2011 and 2010, specific reserves included in the ALLL for residential TDRs

were $401 million and $422 million, respectively. See Note 6, "Loans," to the Consolidated Financial Statements in this Form

10-K for more information.

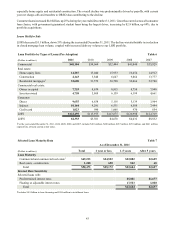

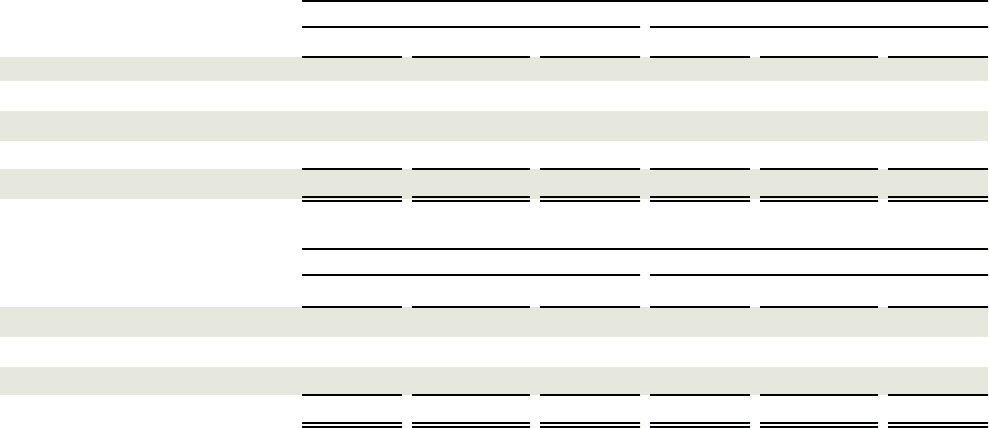

The following tables display our residential real estate TDR portfolio by modification type and payment status at December

31. Loans that have been repurchased from Ginnie Mae under an early buyout clause and subsequently modified have been

excluded from the table. Such loans totaled $65 million and $82 million at December 31, 2011 and 2010, respectively.

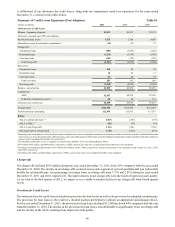

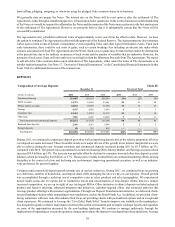

Selected Residential TDR Data

(Dollars in millions)

Rate reduction

Term extension

Rate reduction and term extension

Other 2

Total

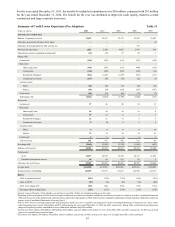

(Dollars in millions)

Rate reduction

Rate reduction and term extension

Other 2

Total

2011

Accruing TDRs

Current

$473

20

1,682

20

$2,195

2010

Accruing TDRs

Current

$375

1,722

42

$2,139

Delinquent1

$40

10

290

3

$343

Delinquent1

$48

305

15

$368

Total

$513

30

1,972

23

$2,538

Total

$423

2,027

57

$2,507

Nonaccruing TDRs

Current

$16

2

35

2

$55

Nonaccruing TDRs

Current

$26

66

3

$95

Delinquent1

$69

24

439

15

$547

Delinquent1

$68

465

31

$564

Table 16

Total

$85

26

474

17

$602

Total

$94

531

34

$659

1 TDRs considered delinquent for purposes of this table were those at least thirty days past due.

2 Primarily consists of extensions and deficiency notes.

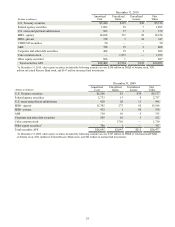

At December 31, 2011, our total TDR portfolio was $3.6 billion and was composed of $3.1 billion, or 87%, of residential

loans (predominantly first and second lien residential mortgages and home equity lines of credit), $442 million, or 12%, of

commercial loans (predominantly income-producing properties), and $39 million, or 1%, of direct consumer loans.

Accruing TDRs increased $207 million, up 8% during the year ended December 31, 2011. The increase in accruing TDRs

was partly attributable to an increase in the number of loan modifications during the year and partly related to the adoption

of new accounting guidance during 2011. Applying the new guidance, which required a review and evaluation of loan

modifications completed since January 1, 2011, resulted in the identification of $93 million of additional TDRs as of July 1,