SunTrust 2011 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

93

recognized in 2009 and higher servicing income. Partially offsetting these improvements were lower mortgage production income,

lower net interest income and higher provision for credit losses.

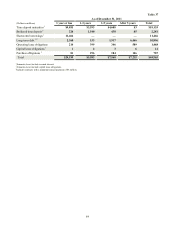

Net interest income was $458 million, down $42 million, or 8%. Net interest income on total average loans of $29.0 billion was

up $54 million, or 25%, due to higher spreads. Offsetting this positive variance was a decline in income from LHFS of $93 million

due to a decline in average LHFS of $2.1 billion, or 46%.

Provision for credit losses increased $58 million, or 5%. The increase was predominantly due to specific actions taken in the first

quarter of 2010 which resulted in additional charge-offs recognized on severely delinquent residential mortgage NPLs,

predominantly in Florida, as well as $51 million in additional charge-offs related to $211 million loans that were reclassified to

LHFS and subsequently sold.

Total noninterest income was $521 million, down $166 million, or 24%. The decline was predominantly due to lower production

income. Mortgage loan production income declined $251 million, or 69%, predominantly due to lower loan production. Loan

originations were $29.3 billion in 2010, a 42% decrease from the prior year. Mortgage servicing income was up $66 million driven

by lower decay due to slower prepayments on MSR values. Total loans serviced at December 31, 2010 were $167.2 billion compared

with $178.9 billion at December 31, 2009, a 7% decline predominantly due to the sale of MSRs on residential loans with unpaid

principal balances of $7.0 billion.

Total noninterest expense declined $324 million, or 23%, predominantly due to a $279 million non-cash goodwill impairment

charge recorded in first quarter of 2009. Total staff expense declined $76 million, or 16%, due to lower commission expense

resulting from lower loan production. Captive reinsurance reserve expense also decreased as a result of trust reserve limits being

reached. These decreases were partially offset by higher allocated credit and technology costs.

Wealth and Investment Management

W&IM's net income for the twelve months ended December 31, 2010 was $138 million, an increase of $38 million, or 38%,

compared with the same period in 2009. The increase in net income was predominantly due to an increase in net interest income,

higher trust and trading income, and the net gain from the sale of the RidgeWorth Money Market Fund business to Federated

Investors, Inc., partially offset by an increase in noninterest expense.

Net interest income was $385 million, an increase of $40 million, or 12%, driven mostly by deposit-related net interest income.

Average loan balances declined $331 million, or 4% with decreases in construction, home equity lines, commercial real estate,

residential mortgages, and consumer direct categories, but were partially offset by increases in personal credit lines and commercial

loans. Loan-related net interest income increased $10 million, or 8%, as higher loan spreads more than offset the decrease in

average loan balances. Average customer deposits increased $130 million, or 1%, as money market accounts increased $1.3 billion,

or 48%. Additionally, demand deposits increased $139 million, or 7%, while time deposits decreased $703 million, or 34%, and

NOW accounts decreased $612 million, or 14%. Deposit-related net interest income increased $21 million, or 9%, due to the

combination of higher average balances and improved deposit spreads.

Provision for credit losses was $61 million, a decrease of $18 million, or 23%, due to decreased net charge-offs in both consumer

and commercial loan products.

Total noninterest income was $821 million, an increase of $67 million, or 9%. Trust income increased $17 million, or 3%,

predominantly due to higher market valuations on managed equity assets and fixed income asset inflows partially offset by lower

MMMF revenue. Trading income increased $29 million due to higher valuations on trading assets and the sale of certain CLO

equity positions. Additionally, other income increased $26 million predominantly due to an $18 million gain from the sale of the

RidgeWorth Money Market Fund business. These increases were partially offset by a $9 million, or 5%, decline in retail investment

income primarily driven by lower fixed annuity revenue. The fixed annuity revenue decline was partially offset by increased

recurring brokerage revenue and increased transactional revenue from variable annuities, mutual fund sales, and managed account

fees.

As of December 31, 2010, assets under management were approximately $105.1 billion compared with $119.5 billion as of

December 31, 2009. Assets under management include individually managed assets, the RidgeWorth Funds, managed institutional

assets, and participant-directed retirement accounts. The December 31, 2009 assets under management included approximately

$18.0 billion of MMMF assets. SunTrust completed the sale of the money market fund business to Federated Investors, Inc. in

the fourth quarter 2010. SunTrust's total assets under advisement were approximately $195.5 billion, which includes $105.1 billion

in assets under management, $46.0 billion in non-managed trust assets, $34.6 billion in retail brokerage assets, and $9.8 billion

in non-managed corporate trust assets.