SunTrust 2011 Annual Report Download - page 195

Download and view the complete annual report

Please find page 195 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

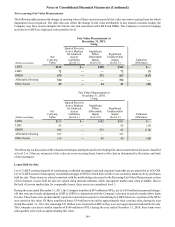

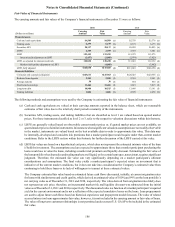

Notes to Consolidated Financial Statements (Continued)

179

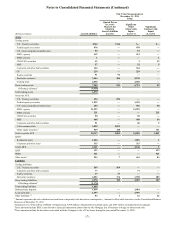

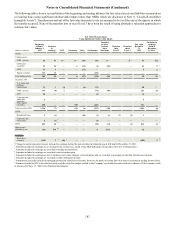

Trading loans

The Company engages in certain businesses whereby the election to carry loans at fair value for financial reporting aligns

with the underlying business purposes. Specifically, the loans that are included within this classification are: (i) loans

made or acquired in connection with the Company’s TRS business (see Note 11, "Certain Transfers of Financial Assets

and Variable Interest Entities," and Note 17, “Derivative Financial Instruments,” for further discussion of this business),

(ii) loans backed by the SBA, and (iii) the loan sales and trading business within the Company’s CIB line of business.

All of these loans have been classified as level 2, due to the market data that the Company uses in its estimates of fair

value.

The loans made in connection with the Company’s TRS business are short-term, demand loans, whereby the repayment

is senior in priority and whose value is collateralized. While these loans do not trade in the market, the Company believes

that the par amount of the loans approximates fair value and no unobservable assumptions are made by the Company to

arrive at this conclusion. At December 31, 2011 and 2010, the Company had outstanding $1.7 billion and $972 million,

respectively, of such short-term loans carried at fair value.

SBA loans are similar to SBA securities discussed herein under “Federal agency securities,” except for their legal form.

In both cases, the Company trades instruments that are fully guaranteed by the U.S. government as to contractual principal

and interest and has sufficient observable trading activity upon which to base its estimates of fair value.

The loans from the Company’s sales and trading business are commercial and corporate leveraged loans that are either

traded in the market or for which similar loans trade. The Company elected to carry these loans at fair value in order to

reflect the active management of these positions. The Company is able to obtain fair value estimates for substantially all

of these loans using a third party valuation service that is broadly used by market participants. While most of the loans

are traded in the markets, the Company does not believe that trading activity qualifies the loans as level 1 instruments,

as the volume and level of trading activity is subject to variability and the loans are not exchange-traded, such that the

Company believes that level 2 is a more appropriate presentation of the underlying market activity for the loans. At

December 31, 2011 and 2010, $323 million and $381 million, respectively, of loans related to the Company’s trading

business were held in inventory.

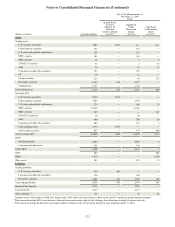

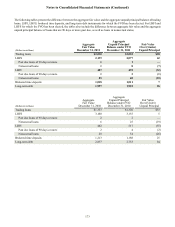

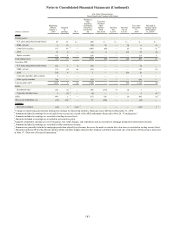

Loans and Loans Held for Sale

Residential LHFS

The Company recognized at fair value certain newly-originated mortgage LHFS based upon defined product criteria.

The Company chooses to fair value these mortgage LHFS in order to eliminate the complexities and inherent difficulties

of achieving hedge accounting and to better align reported results with the underlying economic changes in value of the

loans and related hedge instruments. This election impacts the timing and recognition of origination fees and costs, as

well as servicing value. Specifically, origination fees and costs are recognized in earnings when earned or incurred. The

servicing value, which had been recorded as MSRs at the time the loan was sold, is included in the fair value of the loan

and initially recognized at the time the Company enters into IRLCs with borrowers. The Company uses derivatives to

economically hedge changes in servicing value as a result of including the servicing value in the fair value of the loan.

The mark to market adjustments related to LHFS and the associated economic hedges are captured in mortgage production

related (loss)/income.

Level 2 LHFS are primarily agency loans which trade in active secondary markets and are priced using current market

pricing for similar securities adjusted for servicing and risk. Level 3 loans are primarily non-agency residential mortgages

for which there is little to no observable trading activity of similar instruments in either the new issuance or secondary

loan markets as either whole loans or as securities. Prior to the non-agency residential loan market disruption, which

began during the third quarter of 2007 and continues, the Company was able to obtain certain observable pricing from

either the new issuance or secondary loan market. However, as the markets deteriorated and certain loans were not actively

trading as either whole loans or as securities, the Company began employing the same alternative valuation methodologies

used to value level 3 residential MBS to fair value the loans.

As disclosed in the tabular level 3 rollforwards, transfers of certain mortgage LHFS into level 3 during 2011 were not

due to using alternative valuation approaches, but were largely due to borrower defaults or the identification of other loan

defects impacting the marketability of the loans.

For residential loans that the Company has elected to carry at fair value, the Company has considered the component of

the fair value changes due to instrument-specific credit risk, which is intended to be an approximation of the fair value

change attributable to changes in borrower-specific credit risk. For the years ended December 31, 2011, 2010, and 2009,

the Company recognized losses in the Consolidated Statements of Income/(Loss) of $15 million, $18 million, and $24