SunTrust 2011 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

60

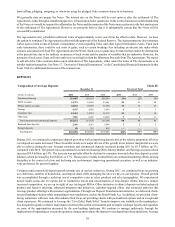

Long-Term Debt

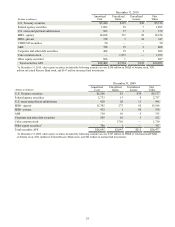

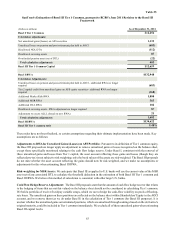

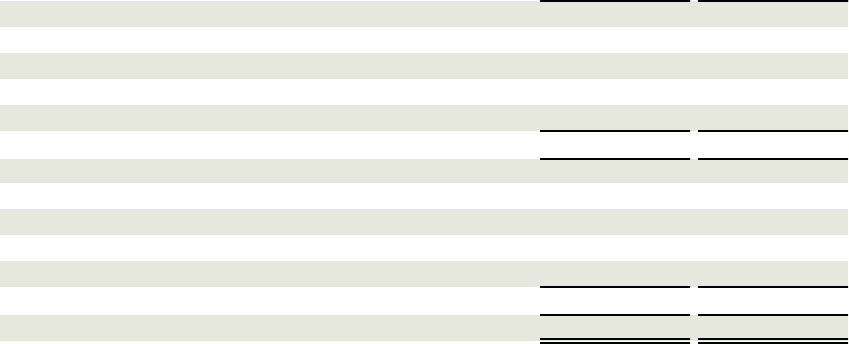

Long-term debt at December 31 consisted of the following:

Long-Term Debt

(Dollars in millions)

Parent Company Only

Senior, fixed rate 1

Senior, variable rate

Subordinated, fixed rate

Junior subordinated, fixed rate

Junior subordinated, variable rate

Total Parent Company debt

Subsidiaries

Senior, fixed rate

Senior, variable rate 2

Subordinated, fixed rate 3

Subordinated, variable rate

Total subsidiaries debt

Total long-term debt

2011

$2,719

1,527

200

1,197

651

6,294

350

2,504

1,260

500

4,614

$10,908

Table 23

2010

$922

1,512

200

1,693

651

4,978

2,640

3,443

2,087

500

8,670

$13,648

1 Debt recorded at fair value, $448 million and $460 million, at December 31, 2011 and 2010, respectively.

2 Debt recorded at fair value, $289 million and $290 million, at December 31, 2011 and 2010, respectively.

3 Debt recorded at fair value.

During the year ended December 31, 2011, our long-term debt decreased by $2.7 billion, or 20%. The change was predominantly

due to the maturity of $2.1 billion, three-year, 3.00% senior notes; $1.1 billion, five-year, variable rate foreign denominated

senior notes; and $852 million of our ten year 6.375% subordinated notes. During 2011, we also repurchased and retired $395

million and $101 million of junior subordinated notes that were due in 2036 and 2042, respectively. These decreases were

partially offset by our issuance of $1.0 billion of 3.60% senior notes that mature in 2016, and $750 million of 3.50% senior

notes that mature in 2017.

In November 2011, SunTrust Preferred Capital I successfully remarketed $102 million of our 5.588% junior subordinated

notes due 2042. In connection with the remarketing, we repurchased and retired all of these notes held by the Trust. As part

of the stock purchase contract between us and the Trust, we issued $103 million of preferred stock that the Trust purchased

with the proceeds from the remarketing. See the "Capital Resources" section below for further discussion of the Series B

Preferred Stock issued as part of this transaction.

CAPITAL RESOURCES

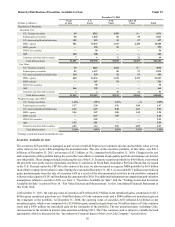

Our primary regulator, the Federal Reserve, measures capital adequacy within a framework that makes capital requirements

sensitive to the risk profiles of individual banking companies. The guidelines weight assets and off-balance sheet risk exposures

(RWA) according to predefined classifications, creating a base from which to compare capital levels. Tier 1 capital primarily

includes realized equity and qualified preferred instruments, less purchase accounting intangibles such as goodwill and core

deposit intangibles. Total capital consists of Tier 1 capital and Tier 2 capital, which includes qualifying portions of subordinated

debt, ALLL up to a maximum of 1.25% of RWA, and 45% of the unrealized gain on equity securities. Additionally, for purposes

of computing regulatory capital, mark to market adjustments related to our own creditworthiness for debt and index linked

CDs accounted for at fair value are excluded from regulatory capital.

Both the Company and the Bank are subject to minimum Tier 1 capital and Total capital ratios of 4% and 8%, respectively,

of RWA. To be considered “well-capitalized,” ratios of 6% and 10%, respectively, are required. Additionally, the Company

and the Bank are subject to requirements for the Tier 1 leverage ratio, which measures Tier 1 capital against average assets,

as calculated in accordance with regulatory guidelines. The minimum and well-capitalized leverage ratios are 3% and 5%,

respectively.