SunTrust 2011 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

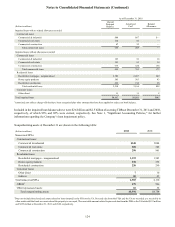

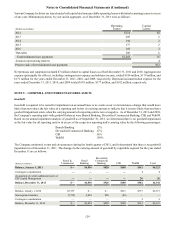

Notes to Consolidated Financial Statements (Continued)

133

securitization transactions, the Company does not have power over the VIE as a result of these rights held by the master

servicer. In certain transactions, the Company does have power as the servicer; however, the Company does not also have

an obligation to absorb losses or the right to receive benefits that could potentially be significant to the securitization.

The absorption of losses and the receipt of benefits would generally manifest itself through the retention of senior or

subordinated interests. No events occurred during the year ended December 31, 2011 that would change the Company’s

previous conclusion that it is not the primary beneficiary of any of these securitization entities. Total assets as of December

31, 2011 and 2010 of the unconsolidated trusts in which the Company has a VI are $529 million and $651 million,

respectively.

The Company’s maximum exposure to loss related to the unconsolidated VIEs in which it holds a VI is comprised of the

loss of value of any interests it retains and any repurchase obligations it incurs as a result of a breach of its representations

and warranties.

Commercial and Corporate Loans

In 2007, the Company completed a $1.9 billion structured sale of corporate loans to multi-seller CP conduits, which are

VIEs administered by unrelated third parties. From the sale, the Company retained a 3% residual interest in the pool of

loans transferred, which does not constitute a VI in the third party conduits as it relates to the unparticipated portion of

the loans. In conjunction with the transfer of the loans, the Company also provided commitments in the form of liquidity

facilities to these conduits. In January 2010, the administrator of the conduits drew on these commitments in full, resulting

in a funded loan to the conduits that was recorded on the Company’s Consolidated Balance Sheets. As of December 31,

2010, the market value of the residual interest was $13 million. During the first quarter of 2011, the Company exercised

its clean up call rights on the structured participation and repurchased the remaining corporate loans. In conjunction with

the clean up call, the outstanding amount of the liquidity facilities and the residual interest were paid off. The exercise

of the clean up call was not material to the Company’s financial condition, results of operations, or cash flows.

The Company has involvement with CLO entities that own commercial leveraged loans and bonds, certain of which were

transferred by the Company to the CLOs. In addition to retaining certain securities issued by the CLOs, the Company

also acts as collateral manager for these CLOs. The securities retained by the Company and the fees received as collateral

manager represent a VI in the CLOs, which are considered to be VIEs.

In accordance with the VIE consolidation guidance beginning January 1, 2010, the Company determined that it was the

primary beneficiary of, and thus, would consolidate one of these CLOs as it has both the power to direct the activities

that most significantly impact the entity’s economic performance and the obligation to absorb losses and the right to

receive benefits from the entity that could potentially be significant to the CLO. In addition to fees received as collateral

manager, including eligibility for performance incentive fees, and owning certain preference shares, the Company’s multi-

seller conduit, Three Pillars, owns a senior interest in the CLO, resulting in economics that could potentially be significant

to the VIE. On January 1, 2010, the Company consolidated $307 million in total assets and $279 million in net liabilities

of the CLO entity. The Company elected to consolidate the CLO at fair value and to carry the financial assets and financial

liabilities of the CLO at fair value subsequent to adoption. The initial consolidation of the CLO did not have a material

impact on the Company’s Consolidated Statements of Shareholders’ Equity. Substantially all of the assets and liabilities

of the CLO are loans and issued debt, respectively. The loans are classified within LHFS at fair value and the debt is

included within long-term debt at fair value on the Company’s Consolidated Balance Sheets (see Note 19, “Fair Value

Election and Measurement,” for a discussion of the Company’s methodologies for estimating the fair values of these

financial instruments). At December 31, 2011 and 2010, the Company’s Consolidated Balance Sheets reflected $315

million and $316 million, respectively, of loans held by the CLO and $289 million and $290 million, respectively, of

debt issued by the CLO. The Company is not obligated, contractually or otherwise, to provide financial support to this

VIE nor has it previously provided support to this VIE. Further, creditors of the VIE have no recourse to the general credit

of the Company, as the liabilities of the CLO are paid only to the extent of available cash flows from the CLO’s assets.

For the remaining CLOs, which are also considered to be VIEs, the Company has determined that it is not the primary

beneficiary as it does not have an obligation to absorb losses or the right to receive benefits from the entities that could

potentially be significant to the VIE. The Company was able to liquidate a number of its positions in these CLO preference

shares during 2010. Its remaining preference share exposure was valued at $2 million as of December 31, 2011 and 2010.

Upon liquidation of the preference shares, the Company’s only remaining involvement with these VIEs was through its

collateral manager role. The Company receives fees for managing the assets of these vehicles; these fees are considered

adequate compensation and are commensurate with the level of effort required to provide such services. The fees received

by the Company from these entities are recorded as trust and investment management income in the Consolidated

Statements of Income/(Loss). Senior fees earned by the Company are generally not considered at risk; however,

subordinate fees earned by the Company are subject to the availability of cash flows and to the priority of payments. The

estimated assets and liabilities of these entities that were not included on the Company’s Consolidated Balance Sheets