SunTrust 2011 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2011 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

|

|

30

adversely affect loan portfolios and operations and increase the cost of doing business; negative public opinion could damage

our reputation and adversely impact business and revenues; a failure in or breach of our operational or security systems or

infrastructure, or those of our third party vendors and other service providers, including as a result of cyber attacks, could

disrupt our businesses, result in the disclosure or misuse of confidential or proprietary information, damage our reputation,

increase our costs and cause losses; we rely on other companies to provide key components of our business infrastructure;

the soundness of other financial institutions could adversely affect us; we depend on the accuracy and completeness of

information about clients and counterparties; regulation by federal and state agencies could adversely affect the business,

revenue, and profit margins; competition in the financial services industry is intense and could result in losing business or

margin declines; maintaining or increasing market share depends on market acceptance and regulatory approval of new

products and services; we might not pay dividends on your common stock; our ability to receive dividends from our subsidiaries

could affect our liquidity and ability to pay dividends; disruptions in our ability to access global capital markets may adversely

affect our capital resources and liquidity; any reduction in our credit rating could increase the cost of our funding from the

capital markets; we have in the past and may in the future pursue acquisitions, which could affect costs and from which we

may not be able to realize anticipated benefits; we are subject to certain litigation, and our expenses related to this litigation

may adversely affect our results; we may incur fines, penalties and other negative consequences from regulatory violations,

possibly even inadvertent or unintentional violations; we depend on the expertise of key personnel, and if these individuals

leave or change their roles without effective replacements, operations may suffer; we may not be able to hire or retain additional

qualified personnel and recruiting and compensation costs may increase as a result of turnover, both of which may increase

costs and reduce profitability and may adversely impact our ability to implement our business strategies; our accounting

policies and processes are critical to how we report our financial condition and results of operations, and they require

management to make estimates about matters that are uncertain; changes in our accounting policies or in accounting standards

could materially affect how we report our financial results and condition; our stock price can be volatile; our framework for

managing risks may not be effective in mitigating risk and loss to us; our disclosure controls and procedures may not prevent

or detect all errors or acts of fraud; our financial instruments carried at fair value expose us to certain market risks; our revenues

derived from our investment securities may be volatile and subject to a variety of risks; and we may enter into transactions

with off-balance sheet affiliates or our subsidiaries.

INTRODUCTION

We are one of the nation’s largest commercial banking organizations and our headquarters are located in Atlanta, Georgia.

Our principal banking subsidiary, SunTrust Bank, offers a full line of financial services for consumers and businesses through

its branches located primarily in Florida, Georgia, Maryland, North Carolina, South Carolina, Tennessee, Virginia, and the

District of Columbia. Within our geographic footprint, we operate under six business segments: Retail Banking, Diversified

Commercial Banking, CRE, CIB, Mortgage, and W&IM, with the remainder in Corporate Other and Treasury. In addition to

deposit, credit, and trust and investment services offered by the Bank, our other subsidiaries provide mortgage banking, credit-

related insurance, asset management, securities brokerage, capital market services, and credit-related insurance.

This MD&A is intended to assist readers in their analysis of the accompanying consolidated financial statements and

supplemental financial information. It should be read in conjunction with the Consolidated Financial Statements and Notes

in Item 8 of this Form 10-K. When we refer to “SunTrust,” “the Company,” “we,” “our” and “us” in this narrative, we mean

SunTrust Banks, Inc. and subsidiaries (consolidated). In the MD&A, net interest income and the net interest margin and

efficiency ratios are presented on an FTE and annualized basis. The FTE basis adjusts for the tax-favored status of net interest

income from certain loans and investments. We believe this measure to be the preferred industry measurement of net interest

income and it enhances comparability of net interest income arising from taxable and tax-exempt sources. Additionally, we

present certain non-U.S. GAAP metrics to assist investors in understanding management’s view of particular financial

measures, as well as, to align presentation of these financial measures with peers in the industry who may also provide a

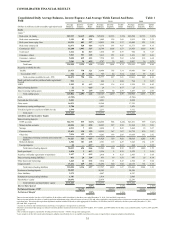

similar presentation. Reconcilements for all non-U.S. GAAP measures are provided below in Tables 41 and 42.

EXECUTIVE OVERVIEW

Economic and regulatory

The economic recovery remained slow and uneven during 2011, with many economic indicators having only improved

modestly or remaining unchanged to levels seen at the end of 2010. Unemployment remained high, the U.S. housing market

continued to show signs of weakness, and consumer confidence remained low. Unemployment remained above 9% for a

majority of the year, but improved to slightly below 9% during the fourth quarter. The U.S. housing market continued to be

weak as evidenced by the large inventory of foreclosed or distressed properties, home prices remaining under pressure,

construction on new single-family homes remaining at historically low levels, and uncertainty about future home prices

causing sales of existing homes to remain weak. Consumer confidence was stagnant throughout the year and ended 2011 at

a level comparable to the end of 2010, as consumer spending increased at only a moderate pace due in part to inflationary

pressures during the year that included elevated commodity prices. Additionally, the financial markets witnessed high levels