PNC Bank 2007 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2007 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

|

|

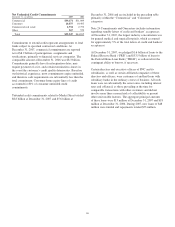

PNC Bank, N.A. provides certain administrative services, a

portion of the program-level credit enhancement and 99% of

liquidity facilities to Market Street in exchange for fees

negotiated based on market rates. PNC recognized program

administrator fees and commitments fees related to PNC’s

portion of the liquidity facilities of $12.6 million and $4.1

million, respectively, for the year ended December 31, 2007.

Neither creditors nor investors in Market Street have any

recourse to our general credit. The commercial paper

obligations at December 31, 2007 and 2006 were effectively

collateralized by Market Street’s assets. While PNC may be

obligated to fund under liquidity facilities for events such as

commercial paper market disruptions, borrower bankruptcies,

collateral deficiencies or covenant violations, our credit risk

under the liquidity facilities is secondary to the risk of first

loss provided by the borrower or another third party in the

form of deal-specific credit enhancement – for example, by

the over collateralization of the assets. Deal-specific credit

enhancement that supports the commercial paper issued by

Market Street is generally structured to cover a multiple of

expected losses for the pool of assets and is sized to generally

meet rating agency standards for comparably structured

transactions. Of the $8.8 billion of liquidity facilities provided

by PNC at December 31, 2007, only $2.8 billion required

PNC to fund if the assets are in default.

Program-level credit enhancement in the amount of 10% of

commitments, excluding explicitly rated AAA/Aaa facilities, is

provided by PNC and a monoline insurer. PNC provides 25% of

the enhancement in the form of a cash collateral account funded

by a loan facility. This facility expires on March 23, 2012. See

Note 5 Loans, Commitments To Extend Credit and

Concentrations of Credit Risk and Note 24 Commitments and

Guarantees for additional information. The monoline insurer

provides the remaining 75% of the enhancement in the form of

a surety bond. The cash collateral account is subordinate to the

surety bond.

Market Street was restructured as a limited liability company

in October 2005 and entered into a Subordinated Note

Purchase Agreement (“Note”) with an unrelated third party.

The Note provides first loss coverage whereby the investor

absorbs losses up to the amount of the Note, which was $8.6

million as of December 31, 2007. Proceeds from the issuance

of the Note are held by Market Street in a first loss reserve

account that will be used to reimburse any losses incurred by

Market Street, PNC Bank, N.A. or other providers under the

liquidity facilities and the credit enhancement arrangements.

As a result of the Note issuance, we reevaluated the design of

Market Street, its capital structure and relationships among the

variable interest holders under the provisions of FIN 46R.

Based on this analysis, we determined that we were no longer

the primary beneficiary as defined by FIN 46R and

deconsolidated Market Street from our Consolidated Balance

Sheet effective October 17, 2005.

PNC considers changes to the variable interest holders (such

as new expected loss note investors and changes to program-

level credit enhancement providers), terms of expected loss

notes, and new types of risks (such as foreign currency or

interest rate) in Market Street as reconsideration events. PNC

reviews the activities of Market Street on at least a quarterly

basis to determine if a reconsideration event has occurred.

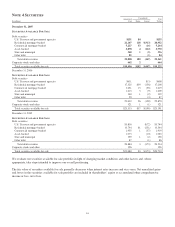

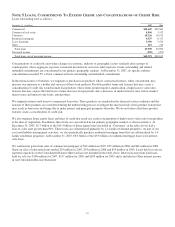

The aggregate assets and liabilities of VIEs that we have

consolidated in our financial statements are as follows:

Consolidated VIEs – PNC Is Primary Beneficiary

In millions

Aggregate

Assets

Aggregate

Liabilities

Partnership interests in low income housing

projects

December 31, 2007 $1,110 $1,110

December 31, 2006 $ 834 $ 834

Low Income Housing Projects

We make certain equity investments in various limited

partnerships that sponsor affordable housing projects utilizing

the Low Income Housing Tax Credit (“LIHTC”) pursuant to

Section 42 of the Internal Revenue Code. The purpose of these

investments is to achieve a satisfactory return on capital, to

facilitate the sale of additional affordable housing product

offerings and to assist us in achieving goals associated with the

Community Reinvestment Act. The primary activities of the

limited partnerships include the identification, development and

operation of multi-family housing that is leased to qualifying

residential tenants. Generally, these types of investments are

funded through a combination of debt and equity, with equity

typically comprising 30% to 60% of the total project capital.

We consolidated those LIHTC investments in which we own a

majority of the limited partnership interests and are deemed to

be the primary beneficiary. We also consolidated entities in

which we, as a national syndicator of affordable housing

equity, serve as the general partner (together with the

aforementioned investments, the “LIHTC investments”), and

no other entity owns a majority of the limited partnership

interests. In these syndication transactions, we create funds in

which our subsidiary is the general partner and sells limited

partnership interests to third parties, and in some cases may

also purchase a limited partnership interest in the fund. The

fund’s limited partners can generally remove the general

partner without cause at any time. The purpose of this

business is to generate income from the syndication of these

funds and to generate servicing fees by managing the funds.

General partner activities include selecting, evaluating,

structuring, negotiating, and closing the fund investments in

operating limited partnerships, as well as oversight of the

ongoing operations of the fund portfolio. The assets are

primarily included in Equity Investments on our Consolidated

Balance Sheet. Neither creditors nor equity investors in the

LIHTC investments have any recourse to our general credit.

The consolidated aggregate assets and debt of these LIHTC

82