PNC Bank 2007 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2007 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

|

|

During the next twelve months, we expect to reclassify to

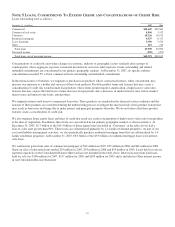

earnings $75 million of pretax net gains, or $49 million after-

tax, on cash flow hedge derivatives currently reported in

accumulated other comprehensive income (loss). This amount

could differ from amounts actually recognized due to changes

in interest rates and the addition of other hedges subsequent to

December 31, 2007. These net gains are anticipated to result

from net cash flows on receive fixed interest rate swaps that

would impact interest income recognized on the related

floating rate commercial loans.

As of December 31, 2007 we have determined that there were

no hedging positions where it was probable that certain

forecasted transactions may not occur within the originally

designated time period.

For those hedge relationships that require testing for

ineffectiveness, any ineffectiveness present in the hedge

relationship is recognized in current earnings. The ineffective

portion of the change in value of these derivatives resulted in

net losses of $1 million for 2007 and $4 million for 2006.

Free-Standing Derivatives

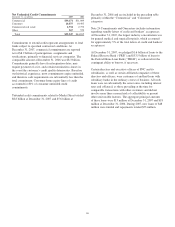

To accommodate customer needs, we also enter into financial

derivative transactions primarily consisting of interest rate

swaps, interest rate caps and floors, futures, swaptions, and

foreign exchange and equity contracts. We primarily manage

our market risk exposure from customer positions through

transactions with third-party dealers. The credit risk associated

with derivatives executed with customers is essentially the

same as that involved in extending loans and is subject to

normal credit policies. We may obtain collateral based on our

assessment of the customer. For derivatives not designated as

an accounting hedge, the gain or loss is recognized in

noninterest income.

Also included in free-standing derivatives are transactions that

we enter into for risk management and proprietary purposes

that are not designated as accounting hedges, primarily

interest rate, basis and total rate of return swaps, interest rate

caps, floors and futures contracts, credit default swaps, option

and foreign exchange contracts and certain interest rate-locked

loan origination commitments as well as commitments to buy

or sell mortgage loans.

Basis swaps are agreements involving the exchange of

payments, based on notional amounts, of two floating rate

financial instruments denominated in the same currency, one

pegged to one reference rate and the other tied to a second

reference rate (e.g., swapping payments tied to one-month

LIBOR for payments tied to three-month LIBOR). We use

these contracts to mitigate the impact on earnings of exposure

to a certain referenced interest rate.

We purchase credit default swaps (“CDS”) to mitigate the risk

of economic loss on a portion of our loan exposure. We also

sell loss protection to mitigate the net premium cost and the

impact of mark-to-market accounting on the CDS in cases

where we buy protection to hedge the loan portfolio and to

take proprietary trading positions. The fair values of these

derivatives typically are based on the change in value, due to

changing credit spreads.

Interest rate lock commitments for, as well as commitments to

buy or sell, mortgage loans that we intend to sell are

considered free-standing derivatives. Our interest rate

exposure on certain commercial mortgage interest rate lock

commitments is economically hedged with pay-fixed interest

rate swaps and forward sales agreements. These contracts

mitigate the impact on earnings of exposure to a certain

referenced rate.

Free-standing derivatives also include positions we take based

on market expectations or to benefit from price differentials

between financial instruments and the market based on stated

risk management objectives.

Derivative Counterparty Credit Risk

By purchasing and writing derivative contracts we are exposed

to credit risk if the counterparties fail to perform. Our credit

risk is equal to the fair value gain in the derivative contract.

We minimize credit risk through credit approvals, limits,

monitoring procedures and collateral requirements. We

generally enter into transactions with counterparties that carry

high quality credit ratings.

We enter into risk participation agreements to share some of

the credit exposure with other counterparties related to interest

rate derivative contracts or to take on credit exposure to

generate revenue. We will make/receive payments under these

guarantees if a customer defaults on its obligation to perform

under certain credit agreements. Risk participation agreements

entered into prior to July 1, 2003 were considered financial

guarantees and therefore are not included in derivatives.

Agreements entered into subsequent to June 30, 2003 are

included in the derivatives table that follows. We determine

that we meet our objective of reducing credit risk associated

with certain counterparties to derivative contracts when the

participation agreements share in their proportional credit

losses of those counterparties.

We generally have established agreements with our major

derivative dealer counterparties that provide for exchanges of

marketable securities or cash to collateralize either party’s

positions. At December 31, 2007 we held short-term

investments, US government securities and mortgage-backed

securities with a fair value of $354 million. We pledged short-

term investments with a fair value of $226 million under these

agreements.

95