PNC Bank 2007 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2007 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

|

|

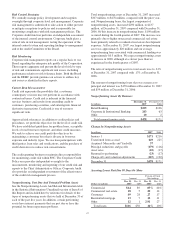

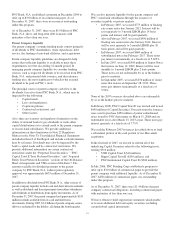

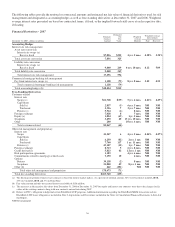

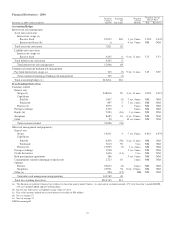

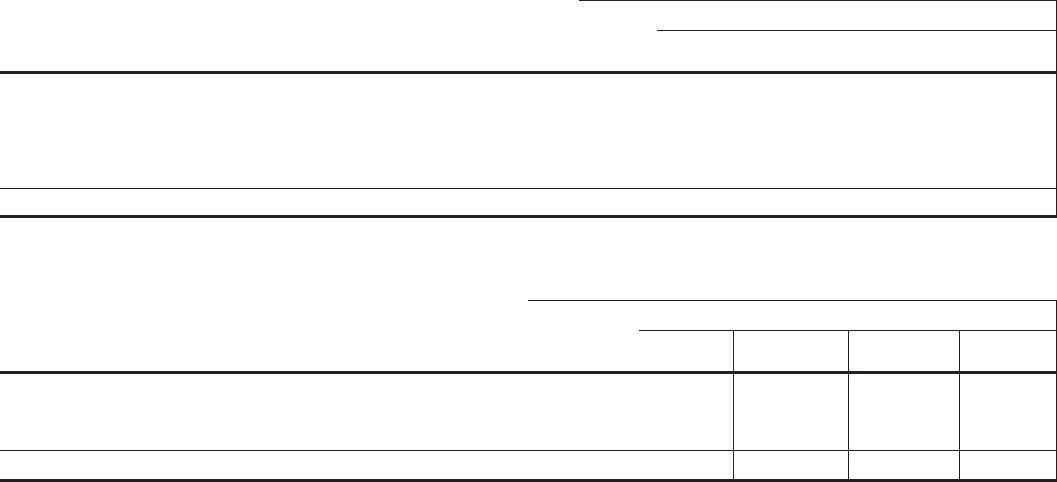

Commitments

The following tables set forth contractual obligations and various other commitments representing required and potential cash

outflows as of December 31, 2007.

Contractual Obligations Payment Due By Period

December 31, 2007 - in millions Total

Less than

one year

One to three

years

Four to five

years

After five

years

Remaining contractual maturities of time deposits $26,402 $22,500 $2,443 $349 $1,110

Borrowed funds 30,931 18,309 6,967 1,282 4,373

Minimum annual rentals on noncancellable leases 1,239 172 296 233 538

Nonqualified pension and post-retirement benefits 314 32 67 66 149

Purchase obligations (a) 441 103 179 90 69

Total contractual cash obligations (b) $59,327 $41,116 $9,952 $2,020 $6,239

(a) Includes purchase obligations for goods and services covered by noncancellable contracts and contracts including cancellation fees.

(b) Excludes amounts related to our adoption of FIN 48 due to the uncertainty in terms of timing and amount of future cash outflows. Note 19 Income Taxes in our

Notes To Consolidated Financial Statements in Item 8 of this Report includes additional information regarding our adoption of FIN 48 in 2007.

Other Commitments (a) Total

Amounts

Committed

Amount Of Commitment Expiration By Period

December 31, 2007 - in millions

Less than

one year

One to three

years

Four to five

years

After five

years

Loan commitments $53,347 $20,401 $21,886 $10,128 $932

Standby letters of credit (b) 4,761 2,427 1,317 862 155

Other commitments (c) 473 108 64 259 42

Total commitments $58,581 $22,936 $23,267 $11,249 $1,129

(a) Other commitments are funding commitments that could potentially require performance in the event of demands by third parties or contingent events. Loan

commitments are reported net of participations, assignments and syndications.

(b) Includes $1.8 billion of standby letters of credit that support remarketing programs for customers’ variable rate demand notes.

(c) Includes private equity funding commitments related to equity management, low income housing projects and other investments.

M

ARKET

R

ISK

M

ANAGEMENT

O

VERVIEW

Market risk is the risk of a loss in earnings or economic value

due to adverse movements in market factors such as interest

rates, credit spreads, foreign exchange rates, and equity prices.

We are exposed to market risk primarily by our involvement

in the following activities, among others:

• Traditional banking activities of taking deposits and

extending loans,

• Private equity and other investments and activities

whose economic values are directly impacted by

market factors, and

• Trading in fixed income products, equities,

derivatives, and foreign exchange, as a result of

customer activities, underwriting, and proprietary

trading.

We have established enterprise-wide policies and

methodologies to identify, measure, monitor, and report

market risk. Market Risk Management provides independent

oversight by monitoring compliance with these limits and

guidelines, and reporting significant risks in the business to

the Joint Risk Committee of the Board.

M

ARKET

R

ISK

M

ANAGEMENT

–I

NTEREST

R

ATE

R

ISK

Interest rate risk results primarily from our traditional banking

activities of gathering deposits and extending loans. Many

factors, including economic and financial conditions,

movements in interest rates, and consumer preferences, affect

the difference between the interest that we earn on assets and

the interest that we pay on liabilities and the level of our

noninterest-bearing funding sources. Due to the repricing term

mismatches and embedded options inherent in certain of these

products, changes in market interest rates not only affect

expected near-term earnings, but also the economic values of

these assets and liabilities.

Asset and Liability Management centrally manages interest

rate risk within limits and guidelines set forth in our risk

management policies approved by the Asset and Liability

Committee and the Risk Committee of the Board.

52