MoneyGram 2010 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2010 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

Table of Contents

In the second quarter of 2008, we repriced our official check product to an average of federal funds effective rate less 85 basis points to

better match our investment commission rate with our lower yield realigned portfolio. In the current environment, the federal funds

effective rate is so low that most of our financial institution customers are in a "negative" commission position, in that we do not owe any

commissions to our customers. While many of our contracts require the financial institution customers to pay us the negative commission

amount, we have opted not to require such payment at this time. As the revenue earned by our financial institution customers from the

sale of our official checks primarily comes from the receipt of their investment commissions from us, the negative commissions reduce

the revenue our financial institution customers earn from our product. Accordingly, our financial institution customers may sharply

reduce their issuances of official checks or choose to not renew their contracts with us if the negative commission positions continue. A

substantial decline in the amount of official checks sold would reduce our investment balances, which would in turn result in lower

investment revenue for us. As official checks are still required for many financial transactions, including home closings and vehicle

purchases, we believe that risk is naturally mitigated in part. We continue to assess the potential impact of negative commissions on our

official check business. While there are currently no plans for changes to our business as a result of the negative commissions, we may

elect in the future to change some portion of our compensation structure for select financial institution customers to mitigate the risk of

substantial declines in our investment balances.

Our senior facility is floating rate debt, resulting in decreases to interest expense in a declining rate environment and increases to interest

expense when rates rise. The Company may elect an interest rate for the senior facility at each reset period based on the United States

prime bank rate or the Eurodollar rate. For the revolving credit facility and Tranche A, the interest rate is either the United States prime

bank rate plus 250 basis points or the Eurodollar rate plus 350 basis points. As of December 31, 2010 the Company has no outstanding

balance related to the revolving credit facility. For Tranche B, the interest rate is either the United States prime bank rate plus 400 basis

points or the Eurodollar rate plus 500 basis points. Under the terms of the senior facility, the interest rate determined using the Eurodollar

index has a minimum rate of 2.50 percent. Throughout 2010, the Company elected to use the United States prime bank rate as its basis.

Elections are based on the index which we believe will yield the lowest interest rate until the next reset date. Interest rate risk is managed

in part through index election.

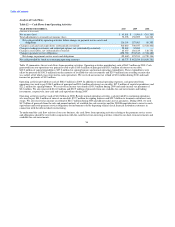

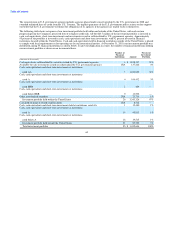

The income statement simulation analysis below incorporates substantially all of our interest rate sensitive assets and liabilities, together

with forecasted changes in the balance sheet and assumptions that reflect the current interest rate environment. This analysis assumes the

yield curve increases gradually over a one-year period. Components of our pre-tax income that are interest rate sensitive include

"Investment revenue," "Investment commissions expense" and "Interest expense." As a result of the current federal funds rate

environment, the outcome of the income statement simulation analysis on "Investment commissions expense" in a declining rate scenario

is not meaningful as we have no downside risk. In the current federal funds rate environment, the worst case scenario is that we would not

owe any commissions to our financial institution customers as the commission rate would decline to zero or become negative.

Accordingly, we have not presented the impact of the simulation in a declining rate environment for "Investment commissions expense."

The following table summarizes the changes to affected components of the income statement under various scenarios.

Basis Point Change in Interest Rates

Down Down Down Up Up Up

(Amounts in thousands) 200 100 50 50 100 200

Interest income $ (974) $ (862) $ (765) $ 3,398 $ 6,802 $ 13,512

Percent change (6.1)% (5.4)% (4.8)% 21.3% 42.6% 84.6%

Investment commissions expense NM NM NM $ (72) $ (502) $ (7,347)

Percent change NM NM NM (11.5)% (80.4)% (1177.4)%

Interest expense NM NM NM $ (188) $ (230) $ (250)

Percent change NM NM NM (0.2)% (0.3)% (0.3)%

Pre-tax loss from continuing operations NM NM NM $ 3,137 $ 6,069 $ 5,915

Percent change NM NM NM 4.2% 8.1% 7.9%

63