MoneyGram 2010 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2010 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

Table of Contents

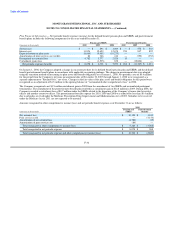

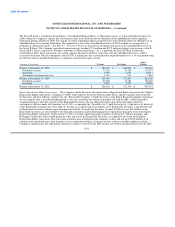

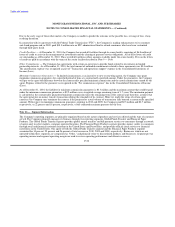

MONEYGRAM INTERNATIONAL, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Pursuant to the terms of options granted in 2009 and 2010, 50 percent of the options awarded become exercisable through the passage of

time (the "Time-based Tranche") and 50 percent of the options awarded become exercisable upon the achievement of certain conditions

(the "Performance-based Tranche"). The Time-based Tranche generally becomes exercisable over a five-year period in either (a) an equal

number of shares each year or (b) for some issuances in 2009, a tranched vesting schedule whereby 15 percent of the Time-based Tranche

vests immediately and then at rates of 10 to 20 percent each year. The Performance-based Tranche becomes exercisable upon the

achievement within five years of grant of the earlier of (a) a pre-defined common stock price for any period of 20 consecutive trading

days, (b) a change in control of the Company resulting in a pre-defined per share consideration or (c) in the event the Company's common

stock does not trade on a United States exchange or trading market, a public offering resulting in the Company's common stock meeting

pre-defined equity values. All options granted in 2009 and 2010 have a term of 10 years.

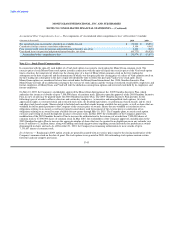

For purposes of determining the fair value of stock option awards, the Company uses the Black-Scholes single option pricing model for

the Time-based Tranches and a combination of Monte-Carlo simulation and the Black-Scholes single option pricing model for the

Performance-based Tranches. Expected volatility is based on the historical volatility of the price of the Company's common stock since

the spin-off on June 30, 2004. The Company used the simplified method to estimate the expected term of the award and historical

information to estimate the forfeiture rate. As the pattern of changes in the value of the Company's common stock since late 2007 is

substantially different from historical patterns, the nature of options granted since 2008 is substantially different from historical grants

and there have been minimal stock option exercises since 2007, the Company is unable to make a more refined estimate than the use of

the simplified method. The expected term represents the period of time that options are expected to be outstanding and the forfeiture rate

represents the number of unvested options that will be forfeited by grantees due to termination of employment. In addition, the Company

considers any expectations regarding future activity which could impact the expected term and forfeiture rate. The risk-free rate for the

Black-Scholes model is based on the United States Treasury yield curve in effect at the time of grant for periods within the expected term

of the option, while the risk-free rate for the Monte-Carlo simulation is based on the five-year United States Treasury yield in effect at the

time of grant. Compensation cost, net of expected forfeitures, is recognized using a straight-line method over the vesting or service

period. The following table provides weighted-average grant-date fair value and assumptions utilized to estimate the grant-date fair value

of the options granted during the years ended December 31:

2010 2009

Expected dividend yield 0.0% 0.0%

Expected volatility 72.9%-74.8% 72.8%-76.9%

Risk-free interest rate 1.8%-3.3% 2.3%-3.2%

Expected life 5.3-6.5 years 5.3-6.5 years

Weighted-average grant-date fair value per option $2.05 $1.49

F-44