MoneyGram 2010 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2010 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

Table of Contents

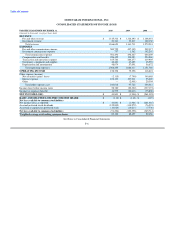

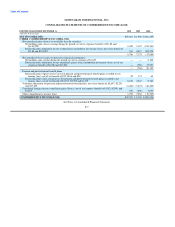

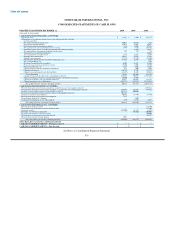

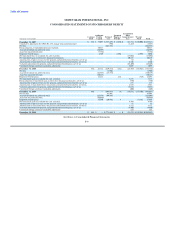

MONEYGRAM INTERNATIONAL, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Securities with gross unrealized losses at the balance sheet date are subject to a process for identifying other-than-temporary impairments.

Securities that the Company deems to be other-than-temporarily impaired are written down to fair value in the period the impairment

occurs. The assessment of whether such impairment has occurred is based on management's evaluation of the underlying reasons for the

decline in fair value on an individual security basis. The Company considers a wide range of factors about the security and uses its best

judgment in evaluating the cause of the decline in the estimated fair value of the security and the prospects for recovery. The Company

considers an investment to be other-than-temporarily impaired when it is deemed probable that the Company will not receive all of the

cash flows contractually stipulated for the investment. The Company evaluates mortgage-backed and other asset-backed investments

rated A and below for which risk of credit loss is deemed more than remote for impairment. When an adverse change in expected cash

flows occurs, and if the fair value of a security is less than its carrying value, the investment is written down to fair value through a

permanent reduction to its amortized cost. Securities gains and losses are recognized upon the sale, call or maturity of securities using the

specific identification method to determine the cost basis of securities sold. Unrealized gains and losses resulting from changes in the fair

value of trading investments and put options related to trading investments are recognized in the period in which the change occurs. Any

impairment charges and other securities gains and losses are included in the Consolidated Statements of Income (Loss) under "Net

securities (gains) losses."

Payment Service Obligations — Payment service obligations primarily consist of: outstanding payment instruments; amounts owed to

financial institutions for funds paid to the Company to cover clearings of official check payment instruments, remittances and clearing

adjustments; amounts owed to agents for funds paid to consumers on behalf of the Company; commissions owed to financial institution

customers and agents for instruments sold; amounts owed to investment brokers for purchased securities; and unclaimed instruments

owed to various states. These obligations are recognized by the Company at the time the underlying transactions occur.

Fair Value of Financial Instruments — Financial instruments consist of cash and cash equivalents, investments, derivatives and debt. The

carrying values of cash and cash equivalents and short-term investments approximate fair value due to the short-term nature of these

instruments. The carrying value of the Company's senior facility approximates fair value as interest related to the debt is variable rate.

The carrying value of the Company's fixed-rate notes also approximates fair value as the contractual interest rate is comparable to debt

with similar maturities issued by companies with similar credit qualities. See Note 4 — Fair Value Measurement for information

regarding the principles and processes used to estimate the fair value of investments and derivatives.

Derivative Financial Instruments — The Company recognizes derivative instruments in the Consolidated Balance Sheets at fair value.

The accounting for changes in the fair value depends on the intended use of the derivative and the resulting designation. For a derivative

instrument designated as a fair value hedge, the Company recognizes the change in fair value in earnings in the period of change, together

with the offsetting change in the hedged item. For a derivative instrument designated as a cash flow hedge, the Company initially reports

the effective portion of the derivative's change in fair value in "Accumulated other comprehensive loss" in the Consolidated Balance

Sheets, and subsequently reclassifies the net change in fair value into earnings when the hedged exposure affects earnings.

The Company evaluated the hedge effectiveness of its derivatives designated as cash flow hedges at inception and on an on-going basis.

Hedge ineffectiveness, if any, is recorded in earnings on the same line as the underlying transaction risk. When a derivative is no longer

expected to be highly effective, hedge accounting is discontinued. Gain or loss on derivatives designated as cash flow hedges that were

terminated or discontinued was recorded in "Investment commissions expense" or "Interest expense" in the Consolidated Statements of

Income (Loss) based on the underlying transaction risk the derivative was originally hedging. For a derivative instrument that does not

qualify, or is not designated, as a hedge, the change in fair value is recognized in "Transaction and operations support" under the

operating section or in "Other" expense in the non-operating section in the Consolidated Statements of Income (Loss) based on the

Company's purpose for entering into the derivatives.

Cash flows resulting from derivative financial instruments are classified in the same category as the cash flows from the items being

hedged. The Company does not use derivative instruments for trading or speculative purposes.

F-15