MoneyGram 2010 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2010 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

Table of Contents

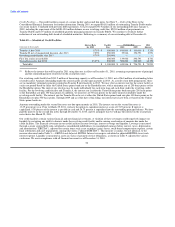

Receivables — Credit risk related to receivables is the risk that we are unable to collect the funds owed to us by our agents and financial

institution customers who have collected the principal amount and fees associated with the sale of our payment instruments from the

consumer on our behalf. Substantially all of the business conducted by our Global Funds Transfer segment is conducted through

independent agents, while the business conducted by the Financial Paper Products segment is conducted through both independent

financial institution customers and agents. Our agents and financial institution customers receive the principal amount and fees related to

the sale of our payment instruments, and we must then collect these funds from them. As a result, we have credit exposure to our agents

and financial institution customers. Agents typically have from one to three days to remit the funds, with longer remittance schedules

granted to international agents and certain domestic agents. As of December 31, 2010, we had credit exposure to our agents of

$594.0 million in the aggregate spread across over 15,000 agents, of which three agents owed us in excess of $15.0 million each. As of

December 31, 2010, we had a credit exposure to our official check financial institution customers of approximately $375.7 million in the

aggregate spread across 1,400 financial institutions, of which one owed us in excess of $15.0 million.

Our strategy in managing credit risk related to receivables is to ensure that the revenue generation from an agent or financial institution

customer is sufficient to provide for an appropriate level of credit risk and to reduce concentrations of risk through diversification,

termination of agents or financial institution customers with poor risk-reward ratios or other means. Management's decision during the

fourth quarter of 2008 to terminate its ACH Commerce business was based primarily on a review of the credit risk associated with that

business.

As our official checks are issued solely through financial institution customers, we do not consider our credit exposure related to

receivables to be significant for official checks. Due to the larger average principal amount of money orders, we consider our credit

exposure from money orders to be of higher risk than exposure due to money transfers. However, in the current macroeconomic

environment and as a result of our international growth, credit risk related to our money transfer products is increasing. While the extent

of credit risk may vary by product, the process for mitigating risk is substantially the same. We assess the creditworthiness of each

potential agent before accepting them into our distribution network. This underwriting process includes not only a determination of

whether to accept a new agent, but also the remittance schedule and volume of transactions that the agent will be allowed to perform in a

given timeframe. We actively monitor the credit risk of our existing agents by conducting periodic comprehensive financial reviews and

cash flow analyses of our agents that average high volumes of transactions and monitoring remittance patterns versus reported sales on a

daily basis. In the current macroeconomic environment, we have tightened our underwriting requirements and have initiated earlier action

against agents with a pattern of delayed or late remittances. We also utilize software embedded in our money transfer and retail money

order point of sale equipment which provides credit risk management abilities. First, this software allows us to control both the number

and dollar amount of transactions that can be completed by both agent and location in a particular timeframe. Second, this software

allows us to monitor for suspicious transactions or volumes of sales, which assists us in uncovering irregularities such as money

laundering, fraud or agent self-use. Finally, the software allows us to remotely disable the point of sale equipment to prevent agents from

transacting if suspicious activity is noted or remittances are not received according to the agent's contract. The point of sale software

requires each location to be re-authorized on a daily basis for transaction processing. Where appropriate, we will also require bank-issued

lines of credit to support our receivables and guarantees from the owners or parent companies, although such guarantees are often

unsecured.

The risk related to official checks is mitigated by only selling these products through financial institution customers, who have never

defaulted on their remittances to us and have had only rare instances of delayed remittances. Substantially all of our financial institution

customers have a next-day remit requirement, which reduces the build-up of credit exposure at each financial institution. In addition, the

termination of our top 10 financial institution customers in connection with the restructuring of our official check business in 2008 has

resulted in less credit exposure at a relatively small number of financial institutions.

61