ICICI Bank 2010 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2010 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

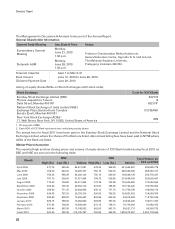

Business Overview

z International Banking Group, comprising the Bank’s international operations, including operations in various

overseas markets as well as products and services for non-resident Indians, international trade finance,

correspondent banking and wholesale resource mobilisation.

z Global Markets Group, comprising our global client-centric treasury operations.

z Corporate Centre, comprising financial reporting, planning and strategy, asset liability management, investor

relations, secretarial, corporate branding, corporate communications, risk management, compliance, internal

audit, legal, financial crime prevention and reputation risk management, accounts and taxation and the Bank’s

proprietary trading operations across various markets.

z Human Resources Management Group, which is responsible for the Bank’s recruitment, training, leadership

development and other personnel management functions and initiatives.

z Global Operations and Middle Office Groups, which are responsible for back-office operations, controls and

monitoring for our domestic and overseas operations.

z Customer Services Group, which is responsible for initiatives towards building and maintaining long-term

customer relationships.

z Information Technology Group, which is responsible for enterprise-wide technology initiatives, with dedicated

teams serving individual business groups and managing information security and shared infrastructure.

z Global Infrastructure & Administration Group, which is responsible for management of corporate facilities

and administrative support functions.

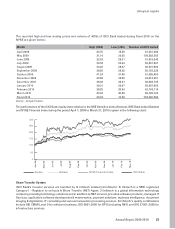

BUSINESS REVIEW

During fiscal 2010, the Bank continued to focus on improving its funding mix, conserving capital, liquidity

management and risk containment and increasing operating efficiencies. We continued to grow our branch

network and became the first private sector bank in India to have 2,000 branches in May 2010. We believe that the

success achieved with respect to our strategy in fiscal 2010 and the enhanced branch network have positioned

us well to capitalise on future growth opportunities.

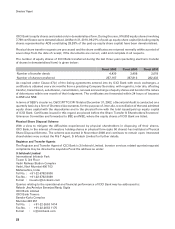

Retail Banking

Retail credit growth in the banking system continued to moderate in fiscal 2010. As per data published by RBI for

the period upto February 26, 2010, year-on-year retail credit growth was about 5%.

Our retail disbursements remained moderate during fiscal 2010, as we focused on opportunities in residential

mortgages and vehicle finance, while reducing our unsecured retail loan and credit card receivables portfolio.

There were also substantial repayments and prepayments from the portfolio during the year. Our retail portfolio

(including builder finance and dealer funding) at March 31, 2010 was Rs. 790.45 billion, constituting 43.6% of our

overall loan portfolio. Within the retail portfolio, unsecured retail loans where we had witnessed higher credit

losses, declined from about 10% of our loan portfolio at March 31, 2008 to 8% at March 31, 2009 and further

to below 5% at March 31, 2010. We continue to believe that retail credit in India has robust long-term growth

potential, driven by sound fundamentals, namely, rising income levels and favourable demographic profile. We

will continue to focus on select retail asset segments like housing and vehicle loans where we expect significant

demand going forward.

During fiscal 2010, we focused on increasing the proportion of low-cost retail deposits in our funding base.

Our current and savings account (CASA) deposits as a percentage of total deposits increased from 28.7% at

March 31, 2009 to 41.7% at March 31, 2010. We continued to expand our branch network during the year.

Our branch network has now increased from 1,419 branches & extension counters at March 31, 2009 to

1,707 branches & extension counters at March 31, 2010 and further to 2,000 branches & extension counters

at May 3, 2010. We also increased our ATM network from 4,713 ATMs at March 31, 2009 to 5,219 ATMs at

March 31, 2010.

We expect our branches to become key points of customer acquisition and service. Accordingly, during fiscal

2010 we changed our organisation structure to provide greater empowerment to our branches. The branch

network is expected to serve as an integrated channel for deposit mobilisation, selected retail asset origination

and distribution of third party products as well as the focal point for customer service and acquisition.

36