ICICI Bank 2010 Annual Report Download - page 181

Download and view the complete annual report

Please find page 181 of the 2010 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

-

193

-

194

-

195

-

196

|

|

F101

6. CREDIT RISK: PORTFOLIOS SUBJECT TO THE STANDARDISED APPROACH

a. External ratings

The Bank uses the standardised approach to measure the capital requirements for credit risk. As per the

standardised approach, regulatory capital requirements for credit risk on corporate exposures is measured

based on external credit ratings assigned by External Credit Assessment Institutions (ECAI) specified by RBI in

its guidelines on Basel II. As stipulated by RBI, the risk weights for resident corporate exposures are assessed

based on the external ratings assigned by domestic ECAI and the risk weights for non-resident corporate

exposures are assessed based on the external ratings assigned by international ECAI. For this purpose, the

domestic ECAI specified by RBI are CRISIL Limited, Credit Analysis & Research Limited, ICRA Limited and

Fitch India and the international ECAI specified by RBI are Standard & Poor’s, Moody’s and Fitch. Further, the

RBI’s Basel II framework stipulates guidelines on the scope and eligibility of application of external ratings. The

Bank reckons the external rating on the exposure for risk weighting purposes, if the external rating assessment

complies with the guidelines stipulated by RBI.

The key aspects of the Bank’s external ratings application framework are as follows:

z The Bank uses only those ratings that have been solicited by the counterparty.

z Foreign sovereign and foreign bank exposures are risk-weighted based on issuer ratings assigned to them.

z The risk-weighting of corporate exposures based on the external credit ratings includes the following:

i) The Bank reckons external ratings of corporates either at the credit facility level or at the borrower

(issuer) level. The Bank considers the facility rating where both the facility and the borrower rating

are available given the more specific nature of the facility credit assessment.

ii) The Bank ensures that the external rating of the facility/borrower has been reviewed at least once by

the ECAI during the previous 15 months and is in force on the date of its application.

iii) When a borrower is assigned a rating that maps to a risk weight of 150%, then this rating is applied

on all the unrated facilities of the borrower and risk weighted at 150%.

iv) Unrated short-term claim on counterparty is assigned a risk weight of at least one level higher than

the risk weight applicable to the rated short term claim on that counterparty.

z The RBI guidelines outline specific conditions for facilities that have multiple ratings. In this context, the

lower rating, where there are two ratings and the second-lowest rating where there are three or more

ratings are used for a given facility.

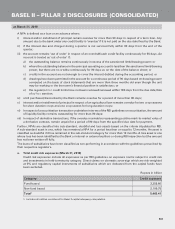

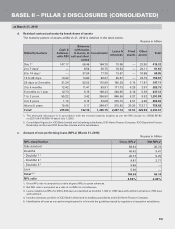

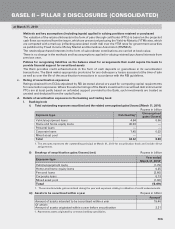

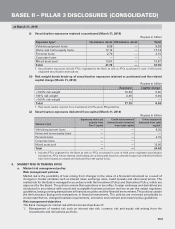

b. Credit exposures by risk weights

At March 31, 2010, the net credit exposures subject to the standardised approach and after adjusting for credit

risk mitigation by risk weights were as follows:

Rupees in billion

Exposure category Amount outstanding1,2

Less than 100% risk weight 1,910.58

100% risk weight 3,120.95

More than 100% risk weight 323.20

Deducted from capital 47.69

Total35,402.42

1. Credit risk exposures include all exposures as per RBI guidelines on exposure norms subject to credit risk and investments in

held-to-maturity category. Direct claims on domestic sovereign which are risk-weighted at 0% and regulatory capital instruments

of subsidiaries which are deducted from the capital funds have been excluded.

2. Net of credit risk mitigants.

3. Includes all entities considered for Basel II capital adequacy computation.

7. CREDIT RISK MITIGATION

a. Collateral management and credit risk mitigation

The Bank has a Board approved policy framework for collateral management and credit risk mitigation

techniques, which include among other aspects guidelines on acceptable types of collateral, ongoing

monitoring of collateral including the frequency and basis of valuation and application of credit risk mitigation

techniques.

BASEL II – PILLAR 3 DISCLOSURES (CONSOLIDATED)

at March 31, 2010