ICICI Bank 2010 Annual Report Download - page 190

Download and view the complete annual report

Please find page 190 of the 2010 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196

|

|

F110

at risk for the purpose of ICAAP. The operational value at risk is estimated based on the principles of advanced

measurement approach by using internal loss data, scenario analysis and external loss data. The operational

value at risk is stress tested on a periodic basis to ensure adequacy of the capital provided for operational risk

and is also back-tested by comparing with actual losses.

Operational risk profiles are presented to the business and operations management on a periodic basis.

Operational risk exposures (risk and control self assessment results, operational risk incidents analysis, adverse

key risk indicators and open risks) are monitored by ORMC on a quarterly basis. Operational risk management

status along with significant incidents analysis is updated to the Risk Committee and to the Board on a half-

yearly basis. Operational risk profile at the Bank level is monitored by the Board on a periodic basis through

bank-wide key risk indicators.

For facilitating effective operational risk management, the Bank has implemented a comprehensive operational

risk management system in the financial year 2010. The software comprises five modules namely incident

management, risk and control self assessment, key indicators, scenario analysis, issues and action. The Bank is

in the process of implementing economic capital system for operational risk during the financial year 2011.

Operational risk management in international locations

ORMG is responsible for design, development and continuous enhancement of the operational risk management

framework across the Bank including overseas banking subsidiaries and overseas branches. While the

common framework is adopted, suitable modifications in the processes are carried out depending upon the

requirements of the local regulatory guidelines. ORMG exercises oversight through the process of periodic

review of operational risk management in the international locations.

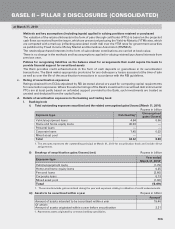

b. Capital requirement for operational risk (March 31, 2010)

As per the RBI guidelines on Basel II, the Bank has adopted basic indicator approach for computing capital

charge for operational risk.

Rupees in billion

Amount

Capital required for operational risk as per basic indicator approach 24.59

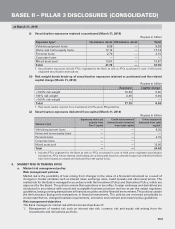

11. INTEREST RATE RISK IN THE BANKING BOOK (IRRBB)

a. Risk Management Framework for IRRBB

Interest rate risk is the risk of potential variability in earnings and capital value resulting from changes in

market interest rates. IRRBB refers to the risk of deterioration in the positions held on the banking book of an

institution due to movement in interest rates over time. The Bank holds assets, liabilities and off balance sheet

items across various markets with different maturity or re-pricing dates and linked to different benchmark

rates, thus creating exposure to unexpected changes in the level of interest rates in such markets.

Organisational set-up

ALCO is responsible for management of the balance sheet of the Bank with a view to manage the market risk

exposure assumed by the Bank within the risk parameters laid down by the Board of Directors/Risk Committee.

A Global Asset Liability Management (GALM) Group at the Bank monitors and manages the risk under the

supervision of ALCO. Further, the Asset Liability Management (ALM) groups in overseas branches manage

the risk at the respective branches, under direction of the Bank’s GALM group.

The ALM Policy of the Bank contains the prudential limits on liquidity and interest rate risk, as prescribed by the

Board of Directors/Risk Committee/ALCO. Any amendments to the ALM Policy can be proposed by business

group(s), in consultation with the market risk and compliance teams and are subject to approval from ALCO/

Risk Committee/Board of Directors, as per the authority defined in the Policy. The amendments so approved

by ALCO are presented to the Board of Directors/Risk Committee for information/approval.

TMOG is an independent group responsible for preparing the various reports to monitor the adherence to

the prudential limits as per the ALM Policy. These limits are monitored on a regular basis at various levels

of periodicity. Breaches, if any, are duly reported to ALCO/Risk Committee/Board of Directors, as may be

required under the framework defined for approvals/ratification. Upon review of the indicators of IRRBB and

the impact thereof, ALCO may suggest necessary corrective actions in order to realign the exposure with the

current assessment of the markets.

BASEL II – PILLAR 3 DISCLOSURES (CONSOLIDATED)

at March 31, 2010