Vodafone 2014 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2014 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

Annual Report 2014 47Overview

Strategy

review Performance Governance Financials

Additional

information

Key risks Mitigating factors

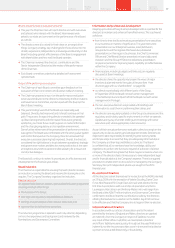

Network or IT systems failure

Major failure or malicious attack on our network or IT systems may result

in service interruption and consequential customer and revenue loss.

Specic back-up and resilience requirements are built into our networks

combined with regularly tested business continuity and disaster

recovery plans.

Failure to protect customer information

We host increasing quantities and types of customer data in both

enterprise and consumer segments and any failure to protect data

adequately could affect our reputation and lead to legalaction.

Hardware and software applications include security features which are

reviewed by our technology and corporate security functions to ensure

compliance with our policies and security standards.

Competition

We face intensifying competition where all operators are looking to

secure a share of the potential customer base, leading to lower future

revenues and protability.

We will continue to promote our differentiated propositions by focusing

on our points of strength such as network quality, products and

customer service. See page 21 for more details on our strategy.

Regulation

We need to comply with an extensive range of regulatory requirements

including the licensing, construction and operation of our networks and

services that can lead to adverse impacts on our business.

We monitor market developments closely, identifying risks in our

current and proposed commercial propositions, which are factored

into our business planning process, competitive commercial pricing

and product strategies. We also make interventions at a national

and international level in respect of legislative, scal and regulatory

proposals which we feel are not in the interest of the Group.

Converged and over-the-top “OTT” services

Some competitors offer converged services which we cannot either

replicate or provide at a similar price point. Furthermore, advances in

smartphone technology place more focus on applications, operating

systems and devices rather than the services provided by operators,

which could erode revenues.

In some markets we already provide xed line services whilst in others

we actively look to provide such services through acquisition or

partnerships. We have also accelerated the introduction of integrated

price plans to reduce customers’ out-of-bundle usage through

substitution. See pages 22 to 25 for more details.

Weak economic conditions

Economic conditions in many markets, especially in Europe, continue

to stagnate or show nominal levels of growth and remain impacted by

austerity measures which could affect disposable incomes. This may

result in customers moving to lower price plans or giving up theirphones.

We monitor the economic situation and have developed plans with

specic actions identied to mitigate the risk of a market entering a

period of severe nancial crisis.

Health risks

Concerns have been expressed that the electromagnetic signals

emitted by mobile handsets and base stations may pose health risks.

Authorities including the World Health Organization (‘WHO’) agree there

is no evidence that convinces experts that exposure to radiofrequency

elds from mobile devices and base stations operated within guideline

limits has any adverse health effects.

We have a global health and safety policy that includes standards for

radio frequency elds that are mandated in all our operating companies.

We monitor scientic developments and engage with relevant bodies

to support the delivery and transparent communication of the scientic

research agenda set by the WHO.

Integration of acquired businesses

The price paid for acquired businesses is based upon current and future

expected cash ows that are expected to be generated from benets

and synergies that being part of the Vodafone Group will generate.

We have experience of acquiring and integrating businesses into the

Group and for all signicant transactions we develop and implement

a structured integration plan to ensure that revenue benets and cost

synergies are delivered.

Key suppliers

We depend on a limited number of suppliers for strategically important

network and IT infrastructure and associated support services to

operate and upgrade our networks and provide key services to

ourcustomers.

We periodically review the performance of key suppliers across

individual markets and from a Group perspective, including identifying

and managing “suppliers at risk” and having business continuity plans in

place in case of supplier failure.

Tax disputes

We operate in many jurisdictions around the world and from time to

time have disputes on the amount of tax due, including an ongoing tax

case in India where the Indian Government has introduced retrospective

legislation that overturns a positive India Supreme Court decision.

We maintain constructive engagement with the tax authorities, relevant

government representatives and other businesses with similar issues.

We also engage advisors and legal counsel to obtain opinions on tax

legislation and principles.

Impairment assumptions

Revisions to the assumptions used in assessing the recoverability

of goodwill, including discount rates, estimated future cash ows or

anticipated changes in operations, could lead to the impairment of

certain Group assets.

We review for impairment at least annually and consider the

appropriateness of assumptions used including discount rates and long-

term growth rates, future technological developments and the timing

and amount of future capital expenditure.