Vodafone 2014 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2014 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

Market overview (continued)

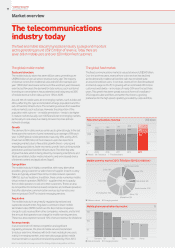

Growing importance of data and other new revenue areas

Mobile voice and texts, our traditional revenue sources, have reached

maturity in a number of markets. To deliver future growth opportunities,

we are investing in newer revenue areas such as data. It is estimated

that between 2013 and 2017 data revenue for the telecommunications

sector is set to grow by US$128 billion, compared to a US$38 billion

decline in voice revenue over the same period. The demand for data will

continue to be driven by rising smartphone and tablet penetration and

usage, and improvements in mobile network capability. As the demand

for data grows, mobile networks have to be recongured to data, while

still meeting the need for traditional texts and calls. Already 91% of the

world’s total trafc on mobile networks is data. The data services most

used are video streaming and internet browsing which require high

speed networks. Therefore, we are investing in ultrafast 4G with average

download speeds of over 75Mbps today, and the expectation of faster

speeds, of up to 300Mbps, by the end of calendar 2014.

New applications for mobile services are being developed by the

industry to extend the use of mobile beyond everyday communication

and deliver new revenue streams, such as mobile payments via

a handset or machine-to-machine services, including the location

monitoring of vehicles, through a SIM card embedded in the vehicle.

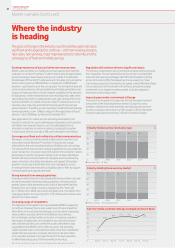

Convergence of xed and mobile into unied communications

We expect a continued trend towards unied communications such

as bundled mobile, xed and TV services. These provide a range

of benets for the user, including simplicity, exibility and cost savings.

The demand for these services is already established among enterprise

customers and it is now becoming more visible in the consumer market,

particularly in southern European markets, such as Spain. We believe

that this demand, combined with technological advances delivering

easier connection of multiple data devices, will support strong data

growth in future, and that this will need to be managed by access

to next-generation xed networks, principally cable or bre, to support

increased speed and capacity demands.

Strong demand from emerging markets

Emerging markets have the most potential for future mobile customer

and revenue growth driven by rising populations, strong economic

growth, lower mobile penetration and a lack of alternative xed line

infrastructure. According to industry analysts, by 2017 there will

be 1.7billion new mobile users across the globe, and most will be from

emerging markets. As a result by 2017, 77% of the world’s mobile users

will be from these markets.

Increasing range of competitors

The high level of competition among established MNOs is expected

to continue. However, there is also a wider pool of new competitors.

Alternative communication technologies, such as instant messaging

services which use data, rather than traditional voice and text,

are increasingly used by mobile consumers. In response, operators

have begun to replace per unit charges for voice and text services

with unlimited bundles, and combine this with a xed fee for data

usage. Meanwhile MVNOs which offer low prices, but have little

capital invested, have in recent periods taken share from established

capital intensive operators. However, the move to 4G and unied

communications presents an opportunity for the major operators

to differentiate the quality of their networks and services.

Regulation will continue to have a signicant impact

The industry is expected to see continued downward revenue pressure

from regulation. For example the Europe Commission is seeking the

removal of all roaming surcharges after 2016 (for Vodafone roaming

accounts for around 6% of European service revenue). In contrast,

Commission proposals to harmonise the speed at which Member States

roll out spectrum and the duration of contracts, should encourage

investment. In our largest emerging market, India, the regulatory

framework is becoming clearer.

Improving economic environment in Europe

The economic recession in Europe over the last two years has been

a key driver of the declining revenue trends in Europe for many

operators. However, we have started to see early signs of economic

recovery in Europe, with a return to GDP growth in 2013 in Northern

Europe and an expected recovery in 2014 in Southern Europe.

Where the industry

is heading

The pace of change in the industry over the last few years has been

signicant and is expected to continue – with new revenue streams,

new users, new services, major improvements to networks, and the

convergence of xed and mobile services.

Note: The industry data on this page is sourced from Strategy Analytics, Analysys Mason and Ovum.

Sep 12

24%

Dec 12 Mar 13 Jun 13 Sep 13 Dec 13 Feb 13

0

20

10

30

40

50

60

% of new mobile customers taking converged services in Spain

44%

49% 51% 51% 49% 57%

2013

72 69 66 64 61

28 31 34 36 39

2014e2015e2016e2017e

0

20

40

60

80

100

Industry mobile service revenue by type %

2013

26 25 24 23 23

74 75 76 77 77

2014e2015e2016e2017e

0

20

40

60

80

100

Industry mobile phone users by market %

n Voice and texts n Data

n Mature markets n Emerging markets

Vodafone Group Plc

Annual Report 2014

Vodafone Group Plc

Annual Report 20142020