Vodafone 2014 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2014 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

Our strategy (continued)

Consumer

Emerging Markets

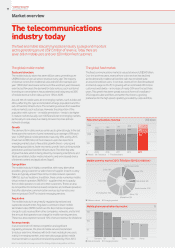

It’s easy to think of Vodafone as simply a European company, with its

headquarters in the UK, but the reality is that one third of our revenue

comes from countries outside Europe and most of this is in fast-growing

emerging markets where data demand is taking off.

Driving the mobile penetration opportunity

The number of customers in our emerging markets has grown steadily

and rapidly from 185 million, 57% of the Group total three years ago,

to around 302 million, representing 70% of the total today. This has been

driven by fast economic growth and rising populations. In our largest

emerging market, India, the proportion of the 1.2 billion population with

a mobile, commonly known as mobile penetration, is still only 78%,

so we expect to see a lot more growth going forward.

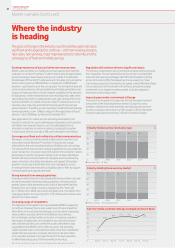

We have invested signicantly in our emerging markets to support and

drive this growth opportunity. We have expanded network coverage

by 8% to 161,500 base station sites, providing us with signicant scale

and broad coverage. We have increased the range of low cost Vodafone

branded devices, enabling more people on low incomes to access

mobile services. We have also lowered the cost of calls, with prices

as low as one US cent per minute in India, which, along with greater

network coverage, has helped drive growth in both the number users

and mobile usage.

The data opportunity

While mobile data usage to browse the internet or watch videos

is increasingly common in Europe, it is still at an early stage in emerging

markets. However, it is expanding quickly due to the growth

in customers and also the greater range and affordability of handsets.

In India, for example, the number of data users increased by 13 million

to 52 million over the course of last year. In Turkey, we now have

6.5 million smartphone users, up from 3.1 million only two years

ago. Outside South Africa, in our smaller southern African markets

of Tanzania, Lesotho, Mozambique and the DRC, the number of data

customers increased 86% to 7.7 million taking the total active data

customer base to 30% of total customers.

Enhancing distribution

Our distribution footprint in emerging markets consists of a range

of branded stores, franchised shops and small independent retail

recharging units. We have modernised over 250 stores in these markets

and we are targeting to reach over 2,300 by 2016. Our branded stores

are very attractive to customers wanting higher end smartphones

or monthly contract plans. In Egypt 95% of new contract customers

come to us through branded stores. In India we have the largest

footprint of 1.7 million point of sale sites for top-ups, signicantly more

than our nearest competitor, and to cater for our female customers

we are opening a number of new “Angel” stores, which are run and

managed exclusively by women.

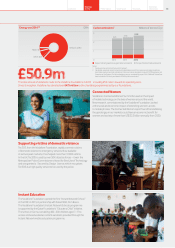

Increasing access to mobile nancial services

Our Vodafone money transfer service, or M-Pesa as it is more

commonly known, enables people who have a standard mobile

phone, but with limited or no access to a bank account, to send and

receive money person to person, top-up airtime, make bill payments,

and in conjunction with the Commercial Bank of Africa to save and also

receive short-term loans.

We now have over 17 million active M-Pesa customers, an increase

of 18% over last year. During the year we launched in several new

emerging markets – India, Egypt, Lesotho and Mozambique. In India

the service has now launched nationwide. Across the M-Pesa footprint,

we have over 200,000 active agents and M-Pesa processed 2.8 billion

transactions (up 27% year-on-year). The service is expected to deliver

a growing proportion of our emerging market revenue over the next few

years. Besides providing additional revenue streams, M-Pesa also keeps

customers on our networks, which reduces the proportion of customers

that leave, commonly known as churn.

We continue to innovate M-Pesa, with the introduction of services such

as Lipa Na M-Pesa, a retail payment proposition for consumers, and the

expansion of international money transfer propositions. In March 2014

we launched the service in our rst European market, Romania.

Context

a Our main emerging markets are India, South Africa, Turkey,

Egypt, Ghana, Kenya, Qatar, Tanzania and several other southern

African countries.

a They provide strong growth opportunities due to fast economic

growth, young and rising populations, and low and increasing

mobile penetration.

a The demand for mobile data in emerging markets is beginning

to take off, in part due to the lack of alternative xed

broadband infrastructure.

a There is signicant scope for newer revenue streams, such

as mobile money transfer as many people in these markets have

little or no access to banking services.

Where we are going

We are aiming to drive continued growth in emerging markets

through a differentiation-based strategy of being the “best”, by:

a increasing and enhancing our base stations sites to improve voice

and data quality and coverage;

a extending bre to enterprise customers to meet the expected

demand for unied communications services;

a expanding the branded store footprint to enhance customer

service; and

a expanding our leading money transfer service, M-Pesa. The goal

is for it to deliver a growing proportion of our emerging market

service revenue.

Vodafone Group Plc

Annual Report 2014

Vodafone Group Plc

Annual Report 20142626