Vodafone 2014 Annual Report Download - page 175

Download and view the complete annual report

Please find page 175 of the 2014 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

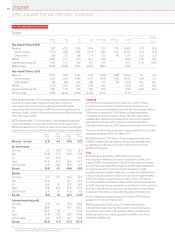

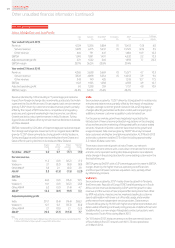

UK

Service revenue declined by 4.0%* driven by the impact of MTR

cuts effective from April 2012, intense price competition and

macroeconomic weakness, which led to lower out-of-bundle

usage. Data revenue grew by 4.2%* driven by higher penetration

of smartphones. Vodafone Red plans, launched in September 2012,

performed well, with over one million customers at 31 March 2013.

Following the purchase of additional spectrum in February 2013,

preparation for LTE roll-out is underway.

The network sharing joint arrangements between Telefónica UK and

Vodafone UK, announced in June 2012, is now operational and

the integration of the CWW enterprise businesses into Vodafone

UK is proceeding successfully.

EBITDA declined by 6.8%*, with a 0.5* percentage point reduction

in EBITDA margin, driven by higher retention activity.

Spain

Service revenue declined by 11.5%* driven by continued

macroeconomic weakness, high unemployment leading to customers

optimising their spend, and a lower customer base following our

decision to remove handset subsidies for a period earlier in the

year. Competition remains intense with the increased popularity

of converged consumer offers in the market. Data revenue grew

by 16.5%* driven by the higher penetration of smartphones and

an increase in those sold with a data bundle. Vodafone Red, which was

launched in Q3, continues to perform well. Fixed revenue declined

by 2.9%*, primarily due to intense competition, although new converged

xed/mobile tariffs had a positive impact on xed broadband customer

additions during Q4.

In March 2013 Vodafone Spain signed an agreement with Orange

to co-invest in a bre network in Spain, with the intention to reach six

million households and workplaces across 50 cities by September 2017.

The combined capital expenditure is expected to reach €1 billion.

EBITDA declined by 9.8%*, with a 0.9* percentage point increase

in EBITDA margin, as lower revenues were offset by commercial

and operating cost efciencies. The EBITDA margin stabilised in H2,

beneting from lower operating and commercial costs.

Other Europe

Service revenue decreased by 5.2%*, driven by declines in the

Netherlands, Greece and Portugal, which more than offset growth

in Albania and Malta. In the Netherlands service revenue declined

by 2.7%* due to more challenging macroeconomic conditions and

lower out-of-bundle usage. Macroeconomic weakness, intense price

competition and an MTR cut resulted in service revenue declines

of 13.4%* and 8.2%* in Greece and Portugal respectively.

EBITDA declined by 3.7%*, with a 0.1* percentage point increase

in EBITDA margin as the impact of service revenue declines was largely

offset by cost efciencies.

Annual Report 2014 173Overview

Strategy

review Performance Governance Financials Additional

information