Vodafone 2014 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2014 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

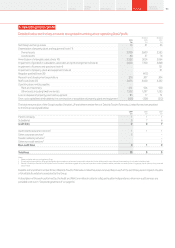

Business combinations and goodwill

When a business combination occurs, the fair values of the identiable assets and liabilities assumed, including intangible assets, are recognised.

The determination of the fair values of acquired assets and liabilities is based, to a considerable extent, on management’s judgement. If the purchase

consideration exceeds the fair value of the net assets acquired then the difference is recognised as goodwill. If the purchase price consideration

is lower than the fair value of the assets acquired then a gain is recognised in the income statement.

Allocation of the purchase price between nite lived assets (discussed below) and indenite lived assets such as goodwill affects the results of the

Group as nite lived intangible assets are amortised, whereas indenite lived intangible assets, including goodwill, are not amortised.

On transition to IFRS the Group elected not to apply IFRS 3, “Business combinations”, retrospectively as the difculty in applying these requirements

to business combinations completed by the Group from incorporation through to 1 April 2004 exceeded any potential benets. Goodwill arising

before the date of transition to IFRS amounted to £78,753 million.

If the Group had elected to apply the accounting for business combinations retrospectively it may have led to an increase or decrease in goodwill,

licences, customer bases, brands and related deferred tax liabilities recognised on acquisition.

Joint arrangements

The Group participates in a number of joint arrangements where control of the arrangement is shared with one or more other parties. A joint

arrangement is classied as a joint operation or as a joint venture, depending on management’s assessment of the legal form and substance

of the arrangement.

The classication can have a material impact on the consolidated nancial statements. The Group’s share of assets, liabilities, revenue, expenses and

cash ows of joint operations are included in the consolidated nancial statements on a line-by-line basis, whereas the Group’s investment and share

of results of joint ventures are shown within single line items in the consolidated statement of nancial position and consolidated income statement

respectively. See note 12 “Investments in associates and joint ventures” to the consolidated nancial statements.

Finite lived intangible assets

Other intangible assets include amounts spent by the Group acquiring licences and spectrum, customer bases and brands and the costs

of purchasing and developing computer software.

Where intangible assets are acquired through business combinations and no active market for the assets exists, the fair value of these assets

is determined by discounting estimated future net cash ows generated by the asset. Estimates relating to the future cash ows and discount rates

used may have a material effect on the reported amounts of nite lived intangible assets.

Estimation of useful life

The useful life over which intangible assets are amortised depends on management’s estimate of the period over which economic benet will

be derived from the asset. Reducing the useful life will increase the amortisation charge in the consolidated income statement. Useful lives are

periodically reviewed to ensure that they remain appropriate. The basis for determining the useful life for the most signicant categories of intangible

assets is discussed below.

Licences and spectrum fees

The estimated useful life is generally the term of the licence unless there is a presumption of renewal at negligible cost; this is adjusted if necessary,

for example taking into account the impact of any expected changes in technology.

Customer bases

The estimated useful life principally reects management’s view of the average economic life of the customer base and is assessed by reference

to customer churn rates. An increase in churn rates may lead to a reduction in the estimated useful life and an increase in the amortisation charge.

Capitalised software

For computer software, the useful life is based on management’s view, considering historical experience with similar products as well as anticipation

of future events which may impact their life such as changes in technology. The useful life will not exceed the duration of a licence.

Property, plant and equipment

Property, plant and equipment represents 18.8% (2013: 12.7%) of the Group’s total assets; estimates and assumptions made may have a material

impact on their carrying value and related depreciation charge. See note 11 “Property, plant and equipment” for further details.

Estimation of useful life

The depreciation charge for an asset is derived using estimates of its expected useful life and expected residual value, which are reviewed annually.

Increasing an asset’s expected life or residual value would result in a reduced depreciation charge in the consolidated income statement.

Management determines the useful lives and residual values for assets when they are acquired, based on experience with similar assets and taking

into account other relevant factors such as any expected changes in technology. The useful life of network infrastructure is assumed not to exceed

the duration of related operating licences unless there is a reasonable expectation of renewal or an alternative future use for the asset.

Post employment benets

Management judgement is exercised when determining the Group’s liabilities and expenses arising for dened benet pension schemes.

Management is required to make assumptions regarding future rates of ination, salary increases, discount rates and longevity of members, each

of which may have a material impact on the dened benet obligations that are recorded. Sensitivity analysis is provided for these assumptions

in note 26 “Post employment benets” to the consolidated nancial statements.

Annual Report 2014 105Overview

Strategy

review Performance Governance Financials Additional

information