United Airlines 2009 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2009 United Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

Table of Contents

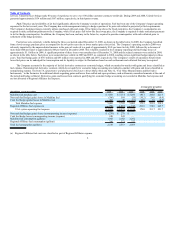

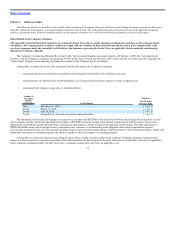

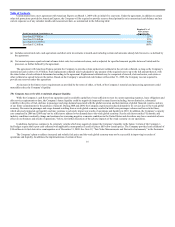

United’s actual and forecasted capacity increases (decreases) for 2009 and 2010, respectively, as compared to the year-ago periods, are summarized in the

following table:

Mainline Regional

Affiliates

Consolidated Domestic International

Fourth Quarter 2009 (3.4)% (4.8)% (7.7)% 17.2%

Full-year 2009 (7.4)% (10.4)% (8.7)% 11.2%

First Quarter 2010 (2.5)% to (1.5)% (5.75)% to (4.75)% (4.0)% to (3.0)% 15.9% to 16.9%

Full-year 2010 (0.5)% to 0.5% (5.3)% to (4.3)% 3.4% to 4.4% 6.3% to 7.3%

Carriers that operate as low cost carriers or that have lower cost structures achieved through reorganization may be more competitive with the rest of the

industry, resulting in lower fares for such carriers’ passengers with a potential negative impact on the Company’s revenues. In addition, future airline mergers or

acquisitions similar to Delta Airlines’ acquisition of Northwest Airlines in late 2008 may enable airlines to improve their revenue and cost performance relative

to peers and thus enhance their competitive position within the industry.

Domestic pricing decisions are largely affected by the need to be competitive with other U.S. airlines. Fare discounting by competitors has historically had

a negative effect on the Company’s financial results because United often finds it necessary to match competitors’ fares to maintain passenger traffic. Attempts

by United and other airlines to raise fares often fail due to a lack of competitive matching.

International Competition. In United’s international networks, the Company competes not only with U.S. airlines, but also with foreign carriers.

Competition on specified international routes is subject to varying degrees of governmental regulations. The United States and European Union (“EU”)

agreement in 2008 to reduce restrictions on flight operations between the two regions has increased competition for United’s transatlantic network from both

U.S. and European airlines. In our Pacific operations, competition is expected to increase as the governments of the United States and China recently approved

additional U.S. and Chinese airlines to fly new routes between the two countries, although the commencement of some new services to China has been postponed

due to the weak global economy. Competition in the Pacific may likely increase when the recently announced open skies agreement between the United States

and Japan becomes effective, which is currently expected to be in the fall of 2010, subject to certain conditions precedent being met. See Industry Regulation,

below. Competition in the Pacific may also increase if Japan Airlines, which filed for bankruptcy in January 2010, emerges from restructuring as a stronger

competitor in the region. Part of United’s ability to successfully compete with non-U.S. carriers on international routes is its ability to generate traffic from and to

the entire U.S. via its integrated domestic route network. Foreign carriers are currently prohibited by U.S. law from carrying local passengers between two points

in the U.S. and United experiences comparable restrictions in many foreign countries. In addition, U.S. carriers are often constrained from carrying passengers to

points beyond designated international gateway cities due to limitations in air service agreements and restrictions imposed unilaterally by foreign governments.

To compensate for these structural limitations, U.S. and foreign carriers have entered into alliances and marketing arrangements that allow these carriers to

exchange traffic between each other’s flights and route networks. See Alliances, above, for further information.

Insurance. United carries hull and liability insurance of a type customary in the air transportation industry, in amounts that the Company deems

appropriate, covering passenger liability, public liability and damage to United’s aircraft and other physical property. United also maintains other types of

insurance such as property, directors and officers, cargo, workers’ compensation, automobile and the like, with limits and deductibles that are standard within the

industry. Losses that materially exceed these limits could have a significant impact on the Company. After the September 11, 2001 terrorist attacks, the

Company’s insurance premiums increased significantly but have since been reduced reflecting the market’s changing perception of risk, as well as the

Company’s ongoing capacity reductions. Additionally, after September 11, 2001, commercial insurers canceled United’s liability insurance for losses resulting

from war and associated perils (terrorism, sabotage, hijacking and other similar events). The U.S. government subsequently agreed to provide commercial

war-risk insurance for

9