Rogers 2015 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2015 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS

FINANCIAL CONDITION

LIQUIDITY

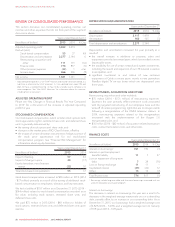

We had approximately $3.3 billion of available liquidity as at

December 31, 2015 (2014 – $2.8 billion), which includes:

• $0.01 billion in cash and cash equivalents (2014 – $0.2 billion);

• $3.0 billion available under our bank credit facility (2014 –

$2.5 billion); and

• $0.25 billion available under our accounts receivable

securitization program (2014 – $0.06 billion).

In addition to the sources of available liquidity noted above, we

held approximately $966 million (2014 – $1,130 million) of

marketable equity securities in publicly traded companies.

COVENANTS

The provisions of our $3.5 billion revolving and non-revolving bank

credit facilities described above impose certain restrictions on our

operations and activities, the most significant of which are leverage-

related maintenance tests. As at December 31, 2015 and 2014, we

were in compliance with all financial covenants, financial ratios, and

all of the terms and conditions of our debt agreements.

Throughout 2015, these covenants did not impose restrictions of

any material consequence on our operations.

CREDIT RATINGS

Credit ratings provide an independent measure of credit quality of

an issue of securities and can affect our ability to obtain short-term

and long-term financing and the terms of the financing. If rating

agencies lower the credit ratings on our debt, particularly a

downgrade below investment grade, it could adversely affect our

cost of financing and access to liquidity and capital.

We have engaged each of Standard & Poor’s Ratings Services

(Standard & Poor’s), Fitch Ratings (Fitch), and Moody’s Investors

Service (Moody’s) to rate our public debt issues. In December

2015, Standard & Poor’s affirmed RCI’s senior unsecured debt at

BBB+ with a stable outlook, Fitch affirmed its BBB+ rating with a

negative outlook, and Moody’s affirmed its comparably equivalent

rating of Baa1 with a stable outlook.

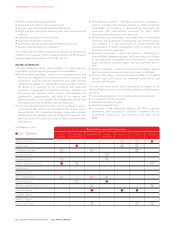

The table below shows the credit ratings on our borrowings received from the rating agencies as at December 31, 2015:

Issuance Standard & Poor’s Fitch Moody’s

Corporate credit issuer default rating BBB+ with a stable outlook BBB+ with a negative outlook Baa1, stable outlook

Senior unsecured debt BBB+ with a stable outlook BBB+ with a negative outlook Baa1, stable outlook

Ratings for debt instruments across the universe of composite rates

range from AAA (Standard & Poor’s and Fitch) or Aaa (Moody’s)

representing the highest quality of securities rated, to D

(Standard & Poor’s), Substantial Risk (Fitch), and C (Moody’s) for the

lowest quality of securities rated. Investment-grade credit ratings

are generally considered to range from BBB- (Standard & Poor’s

and Fitch) or Baa3 (Moody’s) to AAA (Standard & Poor’s and Fitch)

or Aaa (Moody’s).

Credit ratings are not recommendations for investors to purchase,

hold, or sell the rated securities, nor are they a comment on market

price or investor suitability. There is no assurance that a rating will

remain in effect for a given period, or that a rating will not be

revised or withdrawn entirely by a rating agency if it believes

circumstances warrant it. The ratings on our senior debt provided

by Standard & Poor’s, Fitch, and Moody’s are investment-grade

ratings.

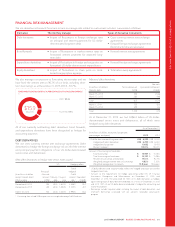

RATIO OF ADJUSTED OPERATING PROFIT / INTEREST ON BORROWINGS

2015

2014

2013

6.6x

6.4x

6.8x

PENSION OBLIGATIONS

Our retiree pension plans had a funding deficit of approximately

$281 million as at December 31, 2015 (2014 – $307 million).

During 2015, our funding deficit decreased by $26 million primarily

as a result of an increase in the discount rate we used to measure

these obligations.

We made a total of $118 million (2014 – $106 million) of

contributions to our pension plans. We expect our total estimated

funding requirements to be $119 million in 2016 and to be

adjusted annually thereafter, based on various market factors such

as interest rates, expected returns, and staffing assumptions.

Changes in factors such as the discount rate, participation rates,

increases in compensation, and the expected return on plan assets

can affect the accrued benefit obligation, pension expense, and

the deficiency of plan assets over accrued obligations in the future.

See “Critical Accounting Estimates and Judgments” for more

information. In order to manage the rising cost of our pension

plans, effective June 30, 2016, the Rogers Defined Benefit pension

plan will be closed to new enrolment. Beginning July 1, 2016,

employees that do not participate in defined benefit pension plans

will be eligible to enrol in a new defined contribution pension plan.

Purchase of annuities

From time to time, we have made additional lump-sum

contributions to our pension plans, and the pension plans have

purchased annuities from insurance companies to fund the

pension benefit obligations for certain groups of retired employees

in the plans. Purchasing the annuities relieves us of our primary

responsibility for that portion of the accrued benefit obligations for

the retired employees and eliminates the significant risk associated

with the obligations.

We did not make any additional lump-sum contributions to our

pension plans in 2015 or 2014, and the pension plans did not

purchase additional annuities.

60 ROGERS COMMUNICATIONS INC. 2015 ANNUAL REPORT