Reebok 2015 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2015 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

|

|

GROUP MANAGEMENT REPORT – FINANCIAL REVIEW

Internal Group Management System

102

3

INTERNALGROUP

MANAGEMENTSYSTEM

The adidas Group’s principal financial goal for increasing shareholder value is maximising operating

cash flow. We strive to achieve this goal by continually improving our top- and bottom-line performance

while at the same time optimising the use of invested capital. Our Group’s planning and controlling

system is therefore designed to provide a variety of tools to assess our current performance and

to align future strategic and investment decisions to best utilise commercial and organisational

opportunities.

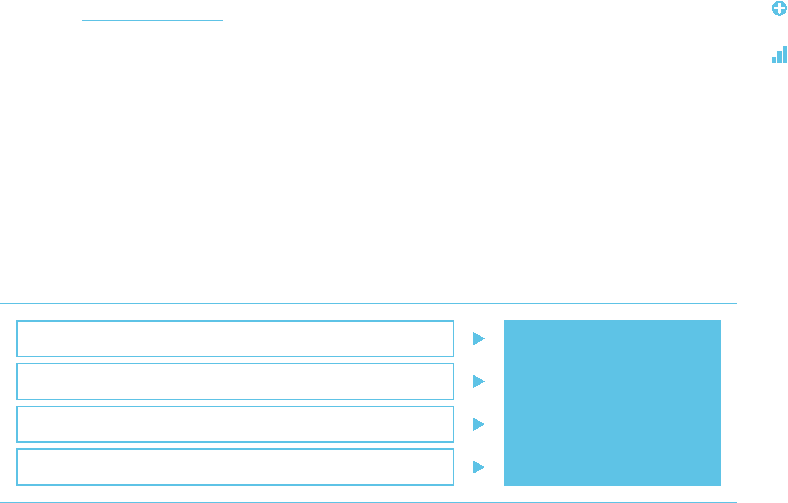

OPERATING CASH FLOW AS INTERNALGROUP MANAGEMENT FOCUS

We believe operating cash flow is the most important driver to increase shareholder value. To support

this, Group Management focuses on four major financial Key Performance Indicators (KPIs). Increasing

net sales and operating profit are the main contributors to improve operating cash flow. In addition, strict

management of operating working capital and value-enhancing capital expenditure are beneficial for

operating cash flow development. As a result, in order to maximise operating cash flow generation across

our organisation, management of our operating segments have responsibility for improving net sales and

operating profit as well as optimising operating working capital and capital expenditure. In addition, in

order to keep senior management focused on long-term performance improvements, we have KPIs in

place, which measure the development of the business units over a multi-year period.

see Glossary, p. 260

see Diagram 01

01FINANCIAL KPIS OF THE ADIDAS GROUP

Net sales

Operating

cash flow

Operating profit

Change in operating working capital

Capital expenditure 1

1 Less depreciation and amortisation.