MoneyGram 2011 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2011 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

|

|

Table of Contents

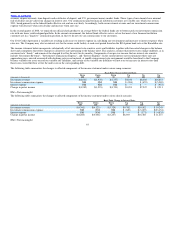

Foreign Currency Risk

We are exposed to foreign currency risk in the ordinary course of business as we offer our products and services through a network of agents and financial

institutions with locations in 192 countries and operate subsidiaries in 12 countries. Translation risk, generated from translating foreign

currency−denominated earnings into U.S. dollars for reporting purposes, is not hedged as this is not considered an economic exposure. In 2011, the decline

of the euro exchange rate (net of hedging activities) resulted in a net decrease to our operating results of $3.0 million over 2010. By policy, we do not

speculate in foreign currencies; all currency trades relate to underlying transactional exposures.

Substantial increases in the credit risk of countries within the European Union, coupled with recessionary forces, have caused high levels of volatility, and a

trend of declining value of the euro against the U.S. dollar. High inter−day volatility will result in higher risk of currency revaluation due to the timing

differences between when our customers pay our agents for their money transfers, and when those proceeds are collected. In addition, currency volatility

can also impact the value of cash balances that are maintained to support the level of our customer activity. Other countries that had extremely high

volatility versus the U.S. dollar in 2011 were India and Mexico, both of which are significant corridors for our money transfer business.

Resolution of the financial crisis affecting Europe relative to the risk of default on the sovereign debt of Greece, Italy, Spain, and Portugal, will be necessary

to reduce our foreign currency risk. The impact of austerity measures being taken by all of the highly leveraged countries that participate in the euro will

also continue to exert recessionary forces on much of the European Union, which in turn can continue to exert a weakening force on the euro. Economic

uncertainty in the United States and its major trading partners will also cause higher levels of volatility for all major currencies versus the U.S. dollar which

could increase foreign currency risk on an ongoing basis.

Our primary source of transactional currency risk is the money transfer business in which funds are frequently transferred cross−border and we settle with

agents in multiple currencies. Although this risk is somewhat limited due to the fact that these transactions are short−term in nature, we currently manage

some of this risk with forward contracts to protect against potential short−term market volatility. The primary currency pairs, based on volume, that are

traded against the dollar in the spot and forward markets include the European euro, Mexican peso, British pound and Indian rupee. The duration of forward

contracts is typically less than one month.

Realized and unrealized gains or losses on transactional currency and any associated revaluation of balance sheet exposures are recorded in “Transaction

and operations support” in the Consolidated Statement of Income (Loss). The fair market value of any open forward contracts at period end are recorded in

“Other assets” in the Consolidated Balance Sheets. The net effect of changes in foreign exchange rates and the related forward contracts for the year ended

December 31, 2011 was a loss of $8.7 million.

Had the euro appreciated/depreciated relative to the U.S. dollar by 20 percent from actual exchange rates for 2011, pre−tax operating income would have

increased/decreased $14.7 million for the year. There are inherent limitations in this sensitivity analysis, primarily due to the assumption that foreign

exchange rate movements are linear and instantaneous, that the unhedged exposure is static, and that we would not hedge any additional exposure. As a

result, the analysis is unable to reflect the potential effects of more complex market changes that could arise, which may positively or negatively affect

income.

62