MoneyGram 2011 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2011 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

|

|

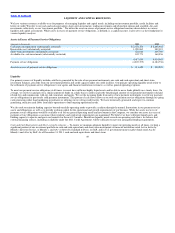

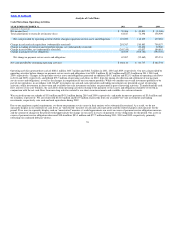

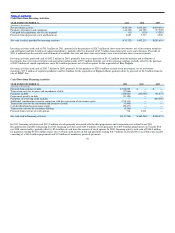

Table of Contents

minimum debt ratings of A3 (Moody’s) and A− (S&P), commercial paper with minimum ratings of A−1 (Moody’s) and P−1 (S&P) and U.S. dollar

denominated SEC registered senior notes of corporations with minimum ratings of A3 and A−. No maturity in the portfolio can exceed 24 months from the

date of purchase.

The financial institutions holding significant portions of our investment portfolio act as custodians for our asset accounts, serve as counterparties to our

foreign currency transactions and conduct cash transfers on our behalf for the purpose of clearing our payment instruments and related agent receivables and

agent payables. Through certain check clearing agreements and other contracts, we are required to utilize several of these financial institutions. As a result

of the credit market crisis, several financial institutions have faced capital and liquidity issues that led them to restrict credit exposure. This has led certain

financial institutions to require that we maintain pre−defined levels of cash, cash equivalents and investments at these financial institutions overnight, with

no restrictions to our usage of the assets during the day. While the credit market crisis and recession affected all financial institutions, those institutions

holding our assets are well capitalized, and there have been no significant concerns as to their ability to honor all obligations related to our holdings.

With respect to our credit union customers, our credit exposure is partially mitigated by National Credit Union Administration insurance. However, as our

credit union customers were not insured by a Temporary Liquidity Guarantee Program (“TLGP”) − equivalent program, we have required certain credit

union customers to provide us with larger balances on deposit and/or to issue cashier’s checks only. While the value of these assets are not at risk in a

disruption or collapse of a counterparty financial institution, the delay in accessing our assets could adversely affect our liquidity and potentially our

earnings depending upon the severity of the delay and corrective actions we may need to take. Corrective actions could include draws upon our 2011 Credit

Agreement to provide short−term liquidity until our assets are released, reimbursements of costs or payment of penalties to our agents and higher banking

fees to transition banking relationships in a short timeframe.

The concentration in U.S. government agencies includes agencies placed under conservatorship by the U.S. government in 2008 and extended unlimited

lines of credit from the U.S. Treasury. The implicit guarantee of the U.S. government and its actions to date support our belief that the U.S. government will

honor the obligations of its agencies if the agencies are unable to do so themselves.

58