MoneyGram 2011 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2011 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

|

|

Table of Contents

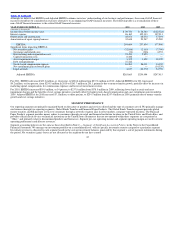

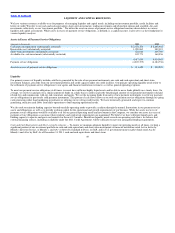

facility and/or causing acceleration of amounts due under the credit facilities. The financial covenants in our 2011 Credit Agreement measure leverage,

interest coverage and liquidity. Leverage is measured through a senior secured debt ratio calculated as consolidated indebtedness to consolidated EBITDA,

adjusted for certain items such as net securities (gains) losses, stock−based compensation expense, certain legal settlements and asset impairments, among

other items, also referred to as adjusted EBITDA. This measure is similar, but not identical, to the measure discussed under EBITDA and Adjusted EBITDA.

Interest coverage is calculated as adjusted EBITDA to net cash interest expense. Liquidity is measured as assets in excess of payment service obligations

adjusted for various exclusions. We are in compliance with all financial covenants as of December 31, 2011 by a substantial margin.

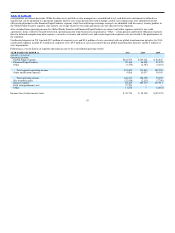

The terms of our 2011 Credit Agreement also place restrictions on certain types of payments we may make, including dividends on our common stock,

acquisitions and the funding of foreign subsidiaries, among others. We do not anticipate that these restrictions will limit our ability to grow the business

either domestically or internationally. In addition, we may only make dividend payments to common stockholders subject to an incremental build−up based

on our consolidated net income in future periods. No dividends were paid on our common stock in 2011, and we do not anticipate declaring any dividends

on our common stock during 2012.

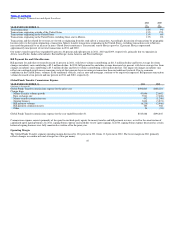

Equity Registration Rights Agreement — The Company and the Investors also entered into a Registration Rights Agreement, or the Equity Registration

Rights Agreement, on March 25, 2008, with respect to the Series B Stock and D Stock, and the common stock owned by the Investors and their affiliates,

also referred to collectively as the Registrable Securities. Under the terms of the Equity Registration Rights Agreement, we are required to file with the SEC

a shelf registration statement relating to the offer and sale of the Registrable Securities and keep such shelf registration statement continuously effective

under the Securities Act of 1933, as amended, or the Securities Act, until the earlier of (1) the date as of which all of the Registrable Securities have been

sold, (2) the date as of which each of the holders of the Registrable Securities is permitted to sell its Registrable Securities without registration pursuant to

Rule 144 under the Securities Act and (3) fifteen years. The holders of the Registrable Securities are also entitled to six demand registrations and unlimited

piggyback registrations during the term of the Equity Registration Rights Agreement. On July 17, 2011, the SEC declared effective a shelf registration

statement on Form S−3 that permits the offer and sale of the Registrable Securities, as required by the terms of the Equity Registration Rights Agreement.

The registration statement also permits the Company to offer and sell up to $500 million of its common stock, preferred stock, debt securities or any

combination of these, from time to time, subject to market conditions and the Company’s capital needs. In December 2011, the Company completed the

secondary offering pursuant to which the Investors sold an aggregate of 10,237,524 shares of Company common stock at a price of $16.25 per share in an

underwritten offering.

Credit Ratings — As of December 31, 2011 our credit ratings from Moody’s and S&P were B1 and BB−, respectively. Our credit facilities, regulatory

capital requirements and other obligations are not impacted by the level of our credit ratings. However, higher credit ratings could increase our ability to

attract capital, reduce our weighted average cost of capital and obtain more favorable terms with our lenders, agents and clearing and cash management

banks.

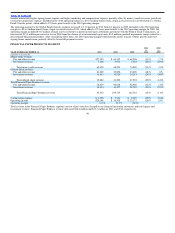

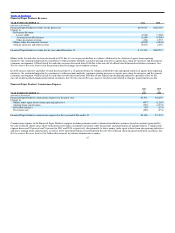

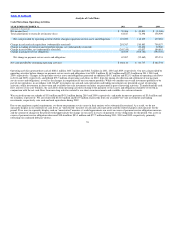

Contractual and Regulatory Capital

Regulatory Capital Requirements — We have capital requirements relating to government regulations in the United States and other countries where we

operate. Such regulations typically require us to maintain certain assets in a defined ratio to our payment service obligations. Through our wholly owned

subsidiary and licensed entity, MPSI, we are regulated in the United States by various state agencies that generally require us to maintain a pool of liquid

assets and investments in an amount generally equal to the regulatory payment service obligation measure, as defined by each state, for our regulated

payment instruments, namely teller checks, agent checks, money orders and money transfers. The regulatory requirements do not require us to specify

individual assets held to meet our payment service obligations, nor are we required to deposit specific assets into a trust, escrow or other special account.

Rather, we must maintain a pool of liquid assets. Provided we maintain a total pool of liquid assets sufficient to meet the regulatory and contractual

requirements, we are able to withdraw, deposit or sell our individual liquid assets at will, without prior notice, penalty or limitations.

52