Experian 2011 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2011 Experian annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

Financial statements 107

8. Financial risk management (continued)

The Group has investments in undertakings with other functional currencies, whose net assets are exposed to foreign exchange translation risk.

In order to reduce the impact of currency uctuations on the value of such entities, the Group has a policy of borrowing in sterling and euros,

as well as in US dollars, and of entering into forward foreign exchange contracts in the relevant currencies. The sensitivity reported in respect

of sterling against the US dollar is wholly attributable to such net exposures. Otherwise the above analysis excludes the impact of foreign

exchange risk on the translation of the net assets of such undertakings.

There has been a change in the Group’s sterling exposures in 2011 as a signicant exposure matured during the course of the year.

Interest rate risk

The Group’s interest rate risk arises principally from its net debt and the portions thereof at variable rates which expose the Group to such risk.

The Group has a policy of normally maintaining between 30% and 70% of net debt at rates that are xed for more than six months. The Group’s

interest rate exposure is managed by the use of xed and oating rate borrowings and by the use of interest rate swaps and cross currency

interest rate swaps to adjust the balance of xed and oating rate liabilities. The Group also mixes the duration of its borrowings to smooth the

impact of interest rate uctuations.

On the basis of the prole of net debt at each balance sheet date and an assessment of reasonably possible changes in the principal interest

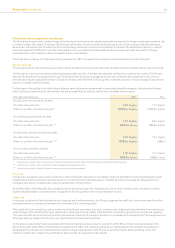

rates, the Group’s sensitivity to interest rate risk can be quantied as follows, with all other variables held constant:

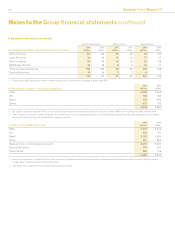

Interest rate exposure 2011 2010

On US dollar denominated net debt:

Interest rate movement 1.6% higher 1.7% higher

Effect on prot for the nancial year * US$16m higher US$15m higher

On sterling denominated net debt:

Interest rate movement 1.7% higher 2.0% higher

Effect on prot for the nancial year ** US$9m lower US$3m higher

On Brazilian real denominated net debt:

Interest rate movement 2.3% higher 1.4% higher

Effect on prot for the nancial year *** US$2m higher US$nil

On euro denominated net debt:

Interest rate movement 1.5% higher 1.7% higher

Effect on prot for the nancial year ** US$8m lower US$3m lower

* primarily as a result of fair value gains on interest rate swaps offset by higher interest expense on oating rate borrowings.

** primarily as a result of the revaluation of borrowings and related derivatives.

*** primarily as a result of higher interest income on cash and cash equivalents.

Price risk

The Group is exposed to price risk in connection with investments classied on the balance sheet as available for sale nancial assets. Such

investments are primarily held to provide security in connection with unfunded pension obligations and are managed by independent fund

managers who seek to mitigate such risk by diversication of the portfolio.

At 31 March 2011, if the relevant stock market and other indices had been 10% higher/lower with all other variables held constant, no further

signicant gains/losses would have been recognised in the Group statement of comprehensive income.

Credit risk

In the case of derivative nancial instruments, deposits and trade receivables, the Group is exposed to credit risk, which would result from the

non-performance of contractual agreements on the part of the contracted party.

This credit risk is minimised by a policy under which the Group only enters into such contracts with banks and nancial institutions with strong

credit ratings, within limits set for each organisation. Dealing activity is closely controlled and counterparty positions are monitored regularly.

The general credit risk on derivative nancial instruments utilised by the Group is therefore not considered to be signicant. The Group does not

anticipate that any losses will arise from non-performance by these counterparties.

At the balance sheet date trade receivables with nancial institutions accounted for some 47% (2010: 45%) of total trade receivables in the

UK and some 22% (2010: 20%) of total trade receivables in the USA. The remaining balances are distributed across multiple industries and

geographies. The Group has implemented policies that require appropriate credit checks on potential clients before granting credit. The

maximum credit risk in respect of such nancial assets is the carrying value of the assets.