Volvo 2005 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2005 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

|

|

Volvo Group 2005 89

operating income and expenses. A provision for decided restructur-

ing measures is reported when a detailed plan for the implementa-

tion of the measures is complete and when this plan is communi-

cated to those who are affected.

Deferred taxes, allocations and untaxed reserves

Tax legislation in Sweden and other countries sometimes contains

rules other than those identifi ed with generally accepted accounting

principles, and which pertain to the timing of taxation and measure-

ment of certain commercial transactions. Deferred taxes are pro-

vided for on differences that arise between the taxable value and

reported value of assets and liabilities (temporary differences) as

well as on tax-loss carryforwards. However, with regards to the valu-

ation of deferred tax assets, that is, the value of future tax reduc-

tions, these items are recognized provided that it is probable that the

amounts can be utilized against future taxable income.

Deferred taxes on temporary differences on participations in sub-

sidiaries and associated companies are only reported when it is

probable that the difference will be recovered in the near future.

Tax laws in Sweden and certain other countries allow companies

to defer payment of taxes through allocations to untaxed reserves.

These items are treated as temporary differences in the consolidat ed

balance sheet, that is, a split is made between deferred tax liability

and equity capital (restricted reserves). In the consolidated income

statement an allocation to, or withdrawal from, untaxed reserves is

divided between deferred taxes and net income for the year.

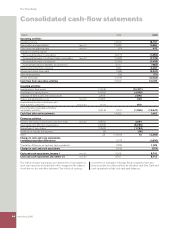

Cash-fl ow statement

The cash-fl ow statement is prepared in accordance with IAS 7, Cash

Flow Statement, indirect method. The cash-fl ow statements of for-

eign Group companies are translated at the average rate. Changes

in Group structure, acquisitions and divestments, are reported net,

excluding cash and cash equivalents, in the item Acquisition and

divestment of subsidiaries and other business units and are included

in Cash Flow from Investing Activities. The reported operating cash

fl ow for 2005 was affected by the adoption of IAS 39. The adjusted

opening value at January 1, 2005 was used in calculating cash fl ow.

Cash and cash equivalents include cash, bank balances and parts

of Marketable Securities. Marketable Securities comprise interest-

bearing securities, the majority of which with terms exceeding three

years. However, these securities have high liquidity and can easily be

converted to cash. In accordance with IAS 7, certain investment in

marketable securities are excluded from the defi nition of cash and

cash equivalents in the cash-fl ow statement if the date of maturity of

such instruments is later than three months after the investment was

made.

Earnings per share

Earnings per share is calculated as the period’s net income attributed

to the shareholders of the parent company, divided with the average

number of outstanding shares per reporting period. To calculate the

result after dilution per share, the average number of shares is

adjusted with the value of the share based incentive program and

employee stock option program recalculated to number of shares.

Note 2 Key sources of estimation uncertainty

Key sources of estimation uncertainty

Volvo’s signifi cant accounting principles are set out in note 1,

Accounting Principles and conform to IFRS as adopted by the EU.

The preparation of Volvo’s Consolidated Financial Statements

requires the use of estimates, judgements and assumptions that

affect the reported amounts of assets, liabilities and provisions at

the date of the fi nancial statements and the reported amounts of

sales and expenses during the periods presented. In preparing these

fi nancial statements, Volvo’s management has made its best esti-

mates and judgements of certain amounts included in the fi nancial

statements, giving due consideration to materiality. The application

of these accounting principles involves the exercise of judgement

and use of assumptions as future uncertainties and, as a result,

actual results could differ from these estimates. In accordance with

IAS 1, preparers are required to provide additional disclosure of

accounting principles in which estimates, judgments and assump-

tions are particularly sensitive and which, if actual results are differ-

ent, may have a material impact on the fi nancial statements. The

accounting principles applied by Volvo that are deemed to meet

these criteria are discussed below:

Impairment of goodwill, other intangible assets

and other non-current assets

Property, plant and equipment, intangible assets, other than good-

will, and certain other non-current assets are amortized and depreci-

ated over their useful lives. Useful lives are based on management’s

estimates of the period that the assets will generate revenue. If, at

the date of the fi nancial statements, there is any indication that a

tangible or intangible non-current asset has been impaired, the

recoverable amount of the asset should be estimated. The recovera-

ble amount is the higher of the asset’s net selling price and its value

in use, estimated with reference to management’s projections of

future cash fl ows. If the recoverable amount of the asset is less than

the carrying amount, an impairment loss is recognized and the carry-

ing amount of the asset is reduced to the recoverable amount.

Determination of the recoverable amount is based upon manage-

ment’s projections of future cash fl ows, which are generally made by

use of internal business plans or forecasts. While management

believes that estimates of future cash fl ows are reasonable, different

assumptions regarding such cash fl ows could materially affect our

valuations. Intangible and tangible non-current assets amounted to

55,840 whereof 11,072 represents goodwill. For Goodwill and cer-

tain other intangible assets with indefi nite life-time an annual impair-

ment review is performed at the year-end closing. Such an impair-

ment review will require management to determine the fair value of

Volvo’s cash generating units, reporting units for US GAAP pur-

poses, on the basis of projected cash fl ows and internal business

plans and forecasts. Volvo has since 2002 performed a simliar

impairment review in accordance with US GAAP. No impairment

charges were required for the period 2002–2005.

Residual value risks

In the course of its operations, Volvo is exposed to residual value

risks through operating lease agreements and sales combined with

repurchase agreements. The products, primarily trucks, for which

Volvo has a residual value commitment, are generally recognized in

the balance sheet as assets under operating leases. Depreciation

expenses for these products are charged on a straight-line basis

over the term of the commitment in amounts required to reduce the

value of the product to its estimated net realizable value at the end