Volvo 2005 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2005 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

|

|

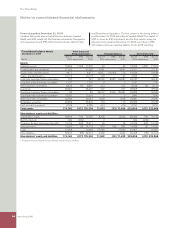

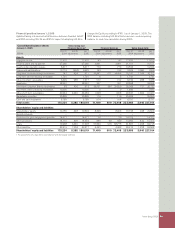

Volvo Group 2005 85

Amounts in SEK M unless otherwise specifi ed. The amounts within parentheses refer to the preceding year, 2004.

The consolidated fi nancial statements for AB Volvo and its subsidiar-

ies have been prepared in accordance with International Financial

Reporting Standards (IFRS) issued by the International Accounting

Standards Board (IASB), as adopted by the EU. Those portions of

IFRS not adopted by the EU have no material effect on this report.

This annual report is prepared in accordance with IAS 1 Presenta-

tion of Financial Statements and in accordance with the Swedish

Companies Act. In addition, RR30 Supplementary Rules for Groups,

was applied, issued by the Swedish Financial Accounting Standards

Council. IFRS differs in some respects from US GAAP, see further in

Note 37.

In the preparation of these fi nancial statements, the company

management has made certain estimates and assumptions that

affect the value of assets and liabilities as well as contingent liabil-

ities at the balance sheet date. Reported amounts for income and

expenses in the reporting period are also affected. The actual future

outcome of certain transactions may differ from the estimated out-

come when these fi nancial statements were issued. Any such differ-

ences will affect the fi nancial statements for future fi scal periods.

Changes of accounting principles

Effective in 2005 Volvo has applied International Financial Reporting

Standards (IFRS) in its fi nancial reporting. In accordance with the

IFRS transition rules in IFRS 1, Volvo applies retroactive application

from the IFRS transition date at January 1, 2004. The general rule is

that restatement of fi nancial reporting for periods after the transition

date should be made as if IFRS has been applied historically. All

comparison fi gures from 2004, in tables and the notes, have been

restated. There are certain exceptions from the general rule of which

the most signifi cant for Volvo are:

– IAS 39 Financial instruments: Recognition and measurement

which is applicable from January 1, 2005.

– Non-amortization of intangible assets with indefi nite useful lives

(e.g. goodwill) in accordance with IFRS 1 should be applied retro-

actively only from the transition date January 1, 2004.

The transition from Swedish GAAP to IFRS is being made accord-

ing to a regulation applicable to all listed companies within the Euro-

pean Union as of 2005. Refer to Note 3, Effect of transition to IFRS

for a more detailed overview of the transition.

Refer to the 2004 Annual Report for a description of the previous

Swedish accounting principles applied by Volvo.

New accounting principles in 2005

The following IFRS standards are applied as of 2005, in accordance

with the respective standards transition rules or in accordance with

IFRS 1, IAS 39: Financial Instruments: Recognition and Measure-

ment, and IFRS 5, Non-Current Assets Held for Sale and Discon-

tinued Operations. Neither of these standards requires retroactive

reporting. Accordingly, the comparison year 2004 is not restated

with regard to these standards. Volvo has decided to apply the

amended IAS 39 regarding hedging of commercial cash fl ows with

earlier adoption from January 1, 2005.

New accounting principles in 2006

As of 2006, Volvo applies IFRIC 4, Determining Whether an

Arrangement Contains a Lease. The International Financial Report-

ing Interpretation Committee (IFRIC) issue its interpretations of

IASB’s accounting standards. The effect of applying IFRIC 4 for

Volvo mainly comprises certain type-bound supplier tools and is

expected to be limited, see also note 37, US GAAP. IFRS 6, Explor-

ation for and Evaluation of Mineral Assets, is not applicable to Volvo,

while IFRS 7, Financial Instruments: Disclosure, shall be applied for

the fi nancial year beginning after January 1, 2007. IFRS 7 involves

disclosure requirements and does not affect Volvo’s fi nancial position.

IFRIC 5, Rights to interests arising from Decommissioning Resto-

ration and Environmental Rehabilitation Funds, IFRIC 6, Liabilities

arising from participating in a Specifi c Market - Waste Electrical and

Electronic Equipment, IFRIC 7, Applying the Restatement Approach

under IAS 29 Financial reporting in Hyperinfl ationary Economies

and IFRIC 8, Scope of IFRS 2, which should be adopted as from

2006 or later are not expected to have any signifi cant effects on

Volvo’s fi nancial position.

Consolidated fi nancial statements

The consolidated fi nancial statements comprise the Parent Com-

pany, subsidiaries, joint ventures and associated companies. Subsid-

iaries are defi ned as companies in which Volvo holds more than 50%

of the voting rights or in which Volvo otherwise has a controlling

infl uence. Joint ventures are companies over which Volvo has joint

control together with one or more external parties. Associated com-

panies are companies in which Volvo has a signifi cant infl uence,

which is normally when Volvo’s holding equals to at least 20% but

less than 50% of the voting rights.

The consolidated fi nancial statement have been prepared in

accordance with the principles set forth in IAS 27, Consolidated and

Separate Financial Statements. Accordingly, intra-Group transactions

and gains on transactions with associated companies are eliminated.

All business combinations are accounted for in accordance with

the purchase method. Volvo applies IFRS 3, Business Combinations

for acquisitions after January 1, 2004, in accordance with the IFRS

1 transition rules. Volvo has decided not to restate prior acquisitions.

Volvo values acquired identifi able assets, tangible and intangible,

and liabilities at fair value. Surplus amounts compared with the pur-

chase consideration are reported as goodwill. Any lesser amount,

so-called negative goodwill, is reported in the income statement.

Companies that have been divested are included in the consoli-

dated fi nancial statements up to and including the date of divest-

ment. Companies acquired during the year are consolidated as of

the date of acquisition.

Joint ventures are reported by use of the proportionate method of

consolidation.

Holdings in associated companies are reported in accordance

with the equity method. The Group’s share of reported income in

such companies is included in the consolidated income statement in

Income from investments in associated com panies, reduced in appro-

priate cases by depreciation of surplus values and the effect of apply-

ing different accounting principles. Income from associated compa-

nies are included in operating income due to that the investments

are of operating nature.

For practical reasons, most of the associated companies are

included in the consolidated accounts with a certain time lag, nor-

mally one quarter. Dividends from associated companies are not

included in consolidated income. In the consolidated balance sheet,

Notes to consolidated

fi nancial statements

Note 1 Accounting principles