Volvo 2005 Annual Report Download - page 133

Download and view the complete annual report

Please find page 133 of the 2005 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

|

|

Volvo Group 2005 129

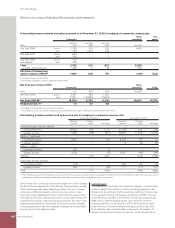

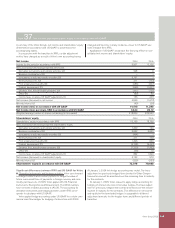

Cash fl ow: In accordance with IFRS, receivables within Volvo’s

customer fi nancing operations are classifi ed as cash fl ow from oper-

ating activities. Under US GAAP the classifi cation depends on how

the actual cash fl ow occurs. In cases when customer fi nancing is to

an external customer and thereby results in an actual cash fl ow,

according to US GAAP this should be classifi ed as cash fl ow from

fi nancing activities. Approximately 15% of Volvo’s customer fi nance

receivables relates to this kind of contracts and should hence be

classifi ed as cash fl ow from investing activities under US GAAP.

Payroll Tax: An adjustment of positive 104 has been booked for

social expenses on employee benefi ts.

I. Income taxes on US GAAP adjustments. Deferred taxes are

reported for temporary differences arising from differences between

US GAAP and IFRS.

J. Minority interest: In accordance with IFRS, minority interest is

recognized a part of shareholders’ equity and are included in net

income for the year in the income statement. Under US GAAP,

minority interest is reported as a separate item in both the income

statement and balance sheet.

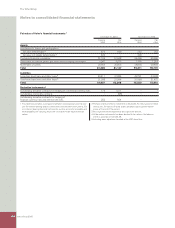

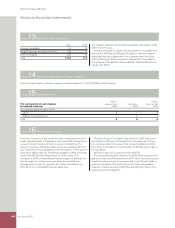

Comprehensive income (loss) 2004 2005

Net income (loss) in accordance with US GAAP 14,416 11,396

Other comprehensive income (loss), net of income taxes

Translation differences (172) 3,458

Unrealized gains and (losses) on securities (SFAS 115):

Unrealized gains (losses) arising during the year (14) 83

Less: Reclassifi cation adjustment for (gains) and losses included in net income (3,285) –

Additional minimum liability for pension obligations (SFAS 87) (471) (284)

Fair value of cash-fl ow hedges (SFAS 133) 13 (1,442)

Other (1) 98

Other comprehensive income (loss), subtotal (3,930) 1,913

Comprehensive income (loss) in accordance with US GAAP 10,486 13,309