PNC Bank 2005 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2005 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

99

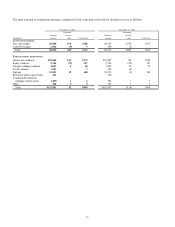

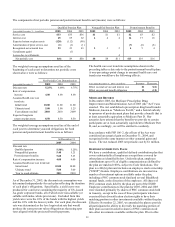

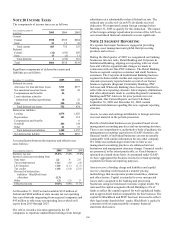

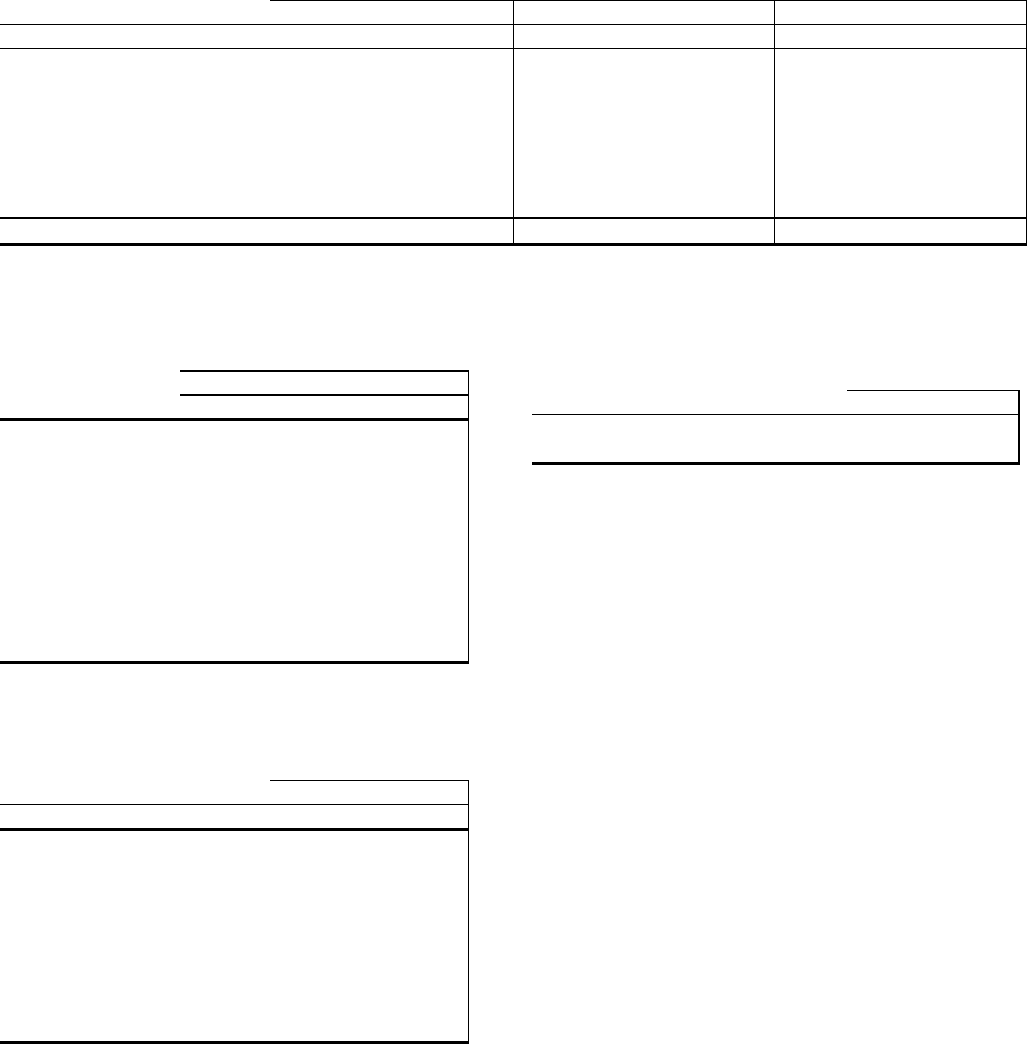

The components of net periodic pension and postretirement benefit cost/(income) were as follows:

Qualified Pension Plan

Nonqualified Pension Plan

Postretirement Benefits

Year ended December 31 – in millions 2005 2004 2003 2005 2004 2003 2005 2004 2003

Service cost $33 $35 $36 $1 $1 $1 $2 $3 $2

Interest cost 65 65 62 4 4 4 14 17 16

Expected return on plan assets (128) (112) (90)

Amortization of prior service cost (1) (1) (1) (7) (6) (6)

Recognized net actuarial loss 23 23 43 3 3 2 4 5 4

Curtailment (gain) (1)

Losses due to settlements 4

Net periodic cost $(8) $9 $50 $8 $8 $11 $13 $19 $16

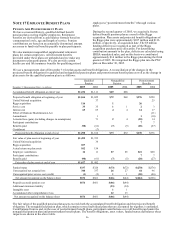

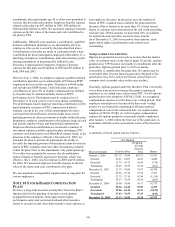

The weighted-average assumptions used (as of the

beginning of each year) to determine net periodic costs

shown above were as follows:

Net Periodic Cost Determination

Year ended December 31

2005

2004

2003

Discount rate 5.25% 6.00% 6.75%

Rate of compensation

increase 4.00 4.00 4.00

Assumed health care cost

trend rate

Initial trend 10.00 11.00 11.00

Ultimate trend 5.00 5.00 5.25

Year ultimate reached 2010 2010 2009

Expected long-term

return on plan assets 8.50 8.50 8.50

The weighted-average assumptions used (as of the end of

each year) to determine year-end obligations for both

pension and postretirement benefits were as follows:

At December 31

2005

2004

Discount rate

Qualified pension 5.50% 5.25%

Nonqualified pension 5.40 5.25

Postretirement benefits 5.60 5.25

Rate of compensation increase 4.00 4.00

Assumed health care cost trend rate

Initial trend 10.00 10.00

Ultimate trend 5.00 5.00

Year to reach ultimate

2011

2010

As of December 31, 2005, the discount rate assumption was

determined independently for each plan reflecting the duration

of each plan’ s obligations. Specifically, a yield curve was

produced for a universe containing the majority of US-issued

Aa grade corporate bonds, all of which were non-callable (or

callable with make-whole provisions). Excluded from this

yield curve were the 10% of the bonds with the highest yields

and the 10% with the lowest yields. For each plan, the discount

rate was determined as the level equivalent rate that would

produce the same present value obligation as that using spot

rates aligned with the projected benefit payments.

The health care cost trend rate assumptions shown in the

preceding tables relate only to the postretirement benefit plans.

A one-percentage-point change in assumed health care cost

trend rates would have the following effects:

Year ended December 31, 2005

–

in millions

Increase

Decrease

Effect on total service and interest cost $1

$(1)

Effect on year-end benefit obligation 13

(12)

MEDICARE REFORM

In December 2003, the Medicare Prescription Drug,

Improvement and Modernization Act of 2003 (the “Act”) was

enacted. The Act established a prescription drug benefit under

Medicare, known as “Medicare Part D,” and a federal subsidy

to sponsors of postretirement plans that provide a benefit that is

at least actuarially equivalent to Medicare Part D. Our

actuaries have attested that the benefits we provide to certain

participants are at least actuarially equivalent to Medicare Part

D, and, accordingly, we will be entitled to a subsidy.

In accordance with FSP 106-2, the effects of the Act were

considered an actuarial gain on December 31, 2004, and

recognized in the same manner as other actuarial gains and

losses. The Act reduced 2005 net periodic cost by $1 million.

DEFINED CONTRIBUTION PLANS

We have a contributory, qualified defined contribution plan that

covers substantially all employees except those covered by

other plans as identified below. Under this plan, employee

contributions up to 6% of eligible compensation as defined by

the plan are matched 100%, subject to Code limitations. The

plan is a 401(k) plan and includes an employee stock ownership

(“ESOP”) feature. Employee contributions are invested in a

number of investment options available under the plan,

including a PNC common stock fund and several BlackRock

mutual funds, at the direction of the employee. All shares of

PNC common stock held by the plan are part of the ESOP.

Employee contributions to the plan for 2005, 2004 and 2003

were matched primarily by shares of PNC common stock held

in treasury, except in the case of those participants who have

exercised their diversification election rights to have their

matching portion in other investments available within the plan.

Effective November 22, 2005, we amended the plan to provide

all participants the ability to diversify the matching portion of

their plan account invested in shares of PNC common stock

into other investments available within the plan. Prior to this