PNC Bank 2005 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2005 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

30

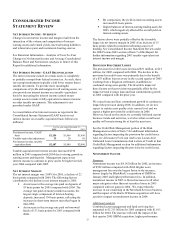

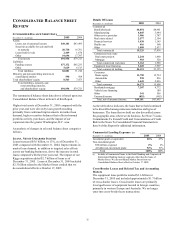

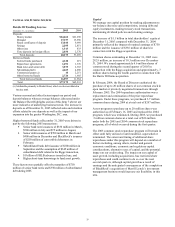

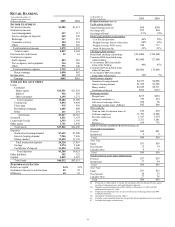

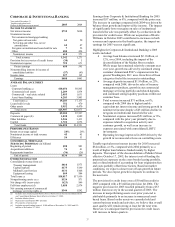

Risk-Based Capital

December 31 - dollars in millions 2005 2004

Capital components

Shareholders’ equity

Common $8,555 $7,465

Preferred 8 8

Trust preferred capital securities 1,417 1,194

Minority interest 291 226

Goodwill and other intangibles (4,122) (3,112)

Net unrealized securities losses 240 66

Net unrealized losses (gains) on

cash flow hedge derivatives 26 (6)

Equity investments in nonfinancial

companies (40)

(32)

Other, net (11)

(15)

Tier 1 risk-based capital 6,364 5,794

Subordinated debt 2,216 1,924

Eligible allowance for credit losses 697 683

Total risk-based capital $9,277 $8,401

Assets

Risk-weighted assets, including off-

balance-sheet instruments and

market risk equivalent assets $76,673 $64,539

Adjusted average total assets 88,329 75,757

Capital ratios

Tier 1 risk-based 8.3% 9.0%

Total risk-based 12.1 13.0

Leverage 7.2 7.6

Tangible common 5.0 5.7

The access to, and cost of, funding new business initiatives

including acquisitions, the ability to engage in expanded

business activities, the ability to pay dividends, the level of

deposit insurance costs, and the level and nature of

regulatory oversight depend, in part, on a financial

institution's capital strength. The declines in the capital

ratios at December 31, 2005 compared with the ratios at

December 31, 2004 were primarily caused by asset growth

and the addition of goodwill and other intangible assets

associated with the Riggs, SSRM and Harris Williams

transactions.

At December 31, 2005, each of our banking subsidiaries

was considered “well capitalized” based on regulatory

capital ratio requirements. See the Supervision And

Regulation section of Item 1 of this Report and Note 4

Regulatory Matters in the Notes To Consolidated Financial

Statements in Item 8 of this Report for additional

information. We believe our bank subsidiaries will continue

to meet these requirements in 2006.