PNC Bank 2005 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2005 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

47

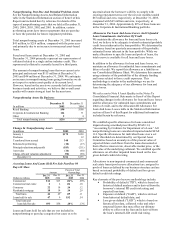

Our pool reserve methodology is sensitive to changes in key

risk parameters such as PDs, LGDs and EADs. In general, a

given change in any of the major risk parameters will have a

corresponding change in the pool reserve allocations for

non-impaired commercial loans. Our commercial loans are

the largest category of credits and are most sensitive to

changes in the key risk parameters and pool reserve loss

rates. To illustrate, if we increase the pool reserve loss rates

by 5% for all categories of non-impaired commercial loans,

then the aggregate of the allowance for loan and lease losses

and allowance for unfunded loan commitments and letters

of credit would increase by $29 million. Additionally, other

factors such as the rate of migration in the severity of

problem loans or changes in the maturity distribution of the

loans will contribute to the final pool reserve allocations.

We make consumer (including residential mortgage) loan

allocations at a total portfolio level by consumer product

line based on historical loss experience. We compute a four-

quarter average loss rate from net charge-offs for the prior

four quarters as a percentage of the average loans

outstanding in those quarters. We apply this loss rate to

loans outstanding at the end of the current period to

determine the consumer loan allocation.

We establish reserves to provide coverage for probable

losses not considered in the specific, pool and consumer

reserve methodologies, such as, but not limited to, industry

concentrations and conditions, credit quality trends, recent

loss experience in particular sectors of the portfolio,

experience, ability and depth of lending management,

changes in risk selection and underwriting standards and the

timing of available information. The amount of reserves for

these qualitative factors is assigned to loan categories and to

business segments based on the relative specific and pool

allocation amounts. Enhancements to the reserve

methodology in the third quarter of 2005 resulted in more

precise modeling of pool allocations and reduced the

amount of reserve allocated for qualitative factors. This

portion represented 9.9% of the total allowance and .12% of

total loans at December 31, 2005.

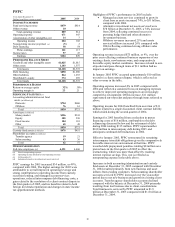

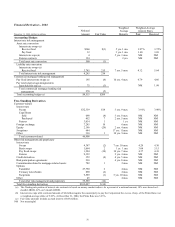

Charge-Offs And Recoveries

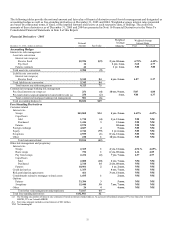

Net Percent of

Year ended December 31

Dollars in millions Charge-offs Recoveries

Charge-offs

(Recoveries)

Average

Loans

2005

Commercial (a) $52 $82

$(30) (.16)%

Commercial real estate 1 1

Consumer 45 15

30 .19

Residential mortgage 2

2 .03

Lease financing 29 1

28 .95

Total $129 $99

$30 .06

2004

Commercial (b) $113 $31

$82

.49%

Commercial real estate 2 1

1

.05

Consumer 43 12

31

.22

Residential mortgage 3 1

2

.05

Lease financing 5 6

(1)

(.03)

Total $166 $51

$115

.28

(a) Includes a $53 million loan recovery.

(b) During the first quarter of 2004, we changed our policy for

recognizing charge-offs on smaller nonperforming commercial loans.

This change resulted in the recognition of an additional $24 million of

gross charge-offs for the first quarter of 2004.

Apart from the impact of the items described in footnotes

(a) and (b) above, commercial net charge-offs declined $35

million in 2005 compared with the prior year primarily due

to an improvement in the overall credit quality of the

commercial loan portfolio. The increase in equipment lease

financing net charge-offs in 2005 compared with the prior

year reflected an additional charge-off in the fourth quarter

of 2005 related to a single leasing customer.

Aside from the impact of the $53 million loan recovery in

2005, increases in the provision for credit losses compared

with 2004 and the allowances for loan and lease losses and

unfunded loan commitments and letters of credit as of

December 31, 2005 reflected growth in loans and loan

commitments and additional provisions related to a leasing

customer. The provision includes amounts for probable

losses on loans and credit exposure related to unfunded loan

commitments and letters of credit.

We do not expect to sustain asset quality at its current level.

However, based on the assets we currently hold and current

business trends and activities, we believe that overall asset

quality will remain strong at least for the near term. This

outlook, combined with expected loan growth, may result in

an increase in the allowance for loan and lease losses in

future periods.

CREDIT-RELATED INSTRUMENTS

Credit Default Swaps

Credit default swaps provide, for a fee, an assumption by a

third party of a portion of the credit risk related to the

underlying financial instruments. We use the contracts to

mitigate credit risk associated with commercial lending

activities as well as proprietary derivative and convertible

bond trading. Credit default swaps are included in the Free-

Standing Derivatives table in the Financial Derivatives

section of this Risk Management discussion. We realized

minimal net gains in connection with credit default swaps

during 2005 and a net loss of $4.4 million in 2004.

Interest Rate Derivative Risk Participation Agreements

We enter into risk participation agreements to share credit

exposure with other financial counterparties related to

interest rate derivative contracts or take on credit exposure

to generate revenue. Risk participation agreements are

included in the Free-Standing Derivatives table in the

Financial Derivatives section of this Risk Management

discussion.

Agreements entered into prior to July 1, 2003 are considered

to be financial guarantees and, therefore, are not included in

the Financial Derivatives section of this Risk Management

discussion. Risk participation agreements entered into prior

to July 1, 2003 used by us to mitigate credit risk had a

notional amount of $3 million at December 31, 2005

compared with $36 million at December 31, 2004. Risk

participation agreements entered into in which we assumed

credit risk exposure had a total notional amount of $18

million at December 31, 2005 compared with $24 million at

December 31, 2004.