PNC Bank 2005 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2005 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

60

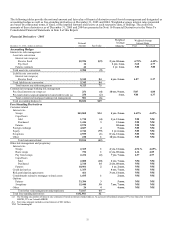

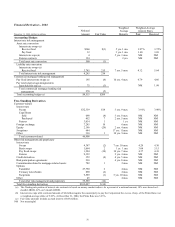

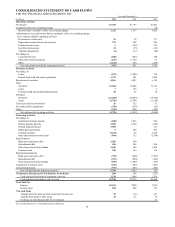

Regulatory capital ratios at December 31, 2004 were 7.6% for

leverage, 9.0% for tier 1 risk-based and 13.0% for total risk-

based capital. The regulatory capital ratios were 8.2% for

leverage, 9.5% for tier 1 risk-based and 13.8% for total risk-

based capital at December 31, 2003.

Glossary of Terms

Accounting/administration net fund assets - Net domestic and

foreign fund investment assets for which we provide

accounting and administration services. We do not include

these assets on our Consolidated Balance Sheet.

Adjusted average total assets - Primarily comprised of total

average quarterly (or annual) assets plus (less) unrealized

losses (gains) on available-for-sale debt securities, less

goodwill and certain other intangible assets.

Annualized - Adjusted to reflect a full year of activity.

Assets under management - Assets over which we have sole or

shared investment authority for our customers/clients. We do

not include these assets on our Consolidated Balance Sheet.

Basis point - One hundredth of a percentage point.

Charge-off - Process of removing a loan or portion of a loan

from a bank's balance sheet because the loan is considered

uncollectible. A charge-off is also recorded when a loan is

transferred to held for sale and the loan’ s market value is less

than its carrying amount.

Common shareholders’ equity to total assets - Common

shareholders' equity divided by total assets. Common

shareholders' equity equals total shareholders' equity less the

liquidation value of preferred stock.

Credit derivatives - Contractual agreements that provide

protection against a credit event of one or more referenced

credits. The nature of a credit event is established by the

protection buyer and protection seller at the inception of a

transaction, and such events include bankruptcy, insolvency

and failure to meet payment obligations when due. The buyer

of the credit derivative pays a periodic fee in return for a

payment by the protection seller upon the occurrence, if any, of

a credit event.

Custody assets - All investment assets held on behalf of clients

under safekeeping arrangements. We do not include these

assets on our Consolidated Balance Sheet. Investment assets

held in custody at other institutions on our behalf are included

in the appropriate asset categories on the Consolidated Balance

Sheet as if physically held by us.

Derivatives - Financial contracts whose value is derived from

publicly traded securities, interest rates, currency exchange

rates or market indices. Derivatives cover a wide assortment of

financial contracts, including forward contracts, futures,

options and swaps.

Duration of equity - An estimate of the rate sensitivity of a

firm’ s economic value of equity. A negative duration of equity

is associated with asset sensitivity (i.e., positioned for rising

interest rates), while a positive value implies liability

sensitivity (i.e., vulnerable to rising rates). For example, if the

duration is +1.5 years, the economic value of equity declines by

1.5% for each 100 basis point increase in interest rates.

Earning assets - Assets that generate income, which include:

federal funds sold; resale agreements; other short-term

investments, including trading securities; loans held for sale;

loans, net of unearned income; securities; and certain other

assets.

Economic capital - Represents the amount of resources that a

business segment should hold to guard against potentially large

losses that could cause insolvency. It is based on a

measurement of economic risk, as opposed to risk as defined

by regulatory bodies. The economic capital measurement

process involves converting a risk distribution to the capital

that is required to support the risk, consistent with an

institution’ s target credit rating. As such, economic risk serves

as a “common currency” of risk that allows an institution to

compare different risks on a similar basis.

Economic value of equity (“EVE”) - The present value of the

expected cash flows of our existing assets less the present value

of the expected cash flows of our existing liabilities, plus the

present value of the net cash flows of our existing off-balance

sheet positions.

Effective duration - A measurement, expressed in years, that,

when multiplied by a change in interest rates, would

approximate the percentage change in value of on- and off-

balance sheet positions.

Efficiency - Noninterest expense divided by the sum of net

interest income and noninterest income.

Foreign exchange contracts - Contracts that provide for the

future receipt and delivery of foreign currency at previously

agreed-upon terms.

Funds transfer pricing - A management accounting

methodology designed to recognize the net interest income

effects of sources and uses of funds provided by the assets and

liabilities of business segments. These balances are assigned

funding rates that represent the interest cost for us to

raise/invest funds with similar maturity and repricing

structures, using the least-cost funding sources available.