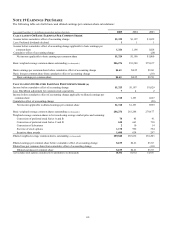

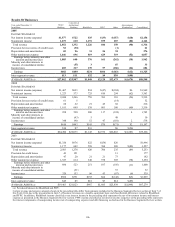

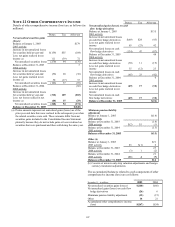

PNC Bank 2005 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2005 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

97

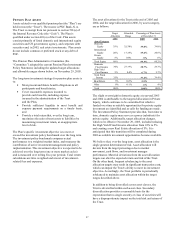

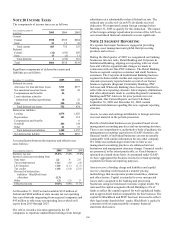

PENSION PLAN ASSETS

Assets related to our qualified pension plan (the “Plan”) are

held in trust (the “Trust”). The trustee is PNC Bank, N.A.

The Trust is exempt from tax pursuant to section 501(a) of

the Internal Revenue Code (the “Code”). The Plan is

qualified under section 401(a) of the Code. Plan assets

consist primarily of listed domestic and international equity

securities and US government, agency, and corporate debt

securities and, in 2005, real estate investments. Plan assets

do not include common or preferred stock or any debt of

PNC.

The Pension Plan Administrative Committee (the

“Committee”) adopted the current Pension Plan Investment

Policy Statement, including the updated target allocations

and allowable ranges shown below, on November 29, 2005.

The long-term investment strategy for pension plan assets is

to:

• Meet present and future benefit obligations to all

participants and beneficiaries,

• Cover reasonable expenses incurred to

provide such benefits, including expense

incurred in the administration of the Trust

and the Plan,

• Provide sufficient liquidity to meet benefit and

expense payment requirements on a timely basis,

and

• Provide a total return that, over the long term,

ma ximizes the ratio of trust assets to liabilities by

maximizing investment return, at an appropriate

level of risk.

The Plan’ s specific investment objective is to meet or

exceed the investment policy benchmark over the long term.

The investment policy benchmark compares actual

performance to a weighted market index, and measures the

contribution of active investment management and policy

implementation. This investment objective is expected to be

achieved over the long term (one or more market cycles)

and is measured over rolling five-year periods. Total return

calculations are time -weighted and are net of investment-

related fees and expenses.

The asset allocations for the Trust at the end of 2005 and

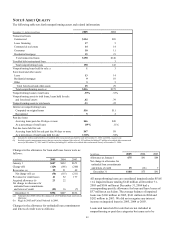

2004, and the target allocation for 2006, by asset category,

are as follows:

Target

Allocation

Allowable

Range

Percentage of Plan Assets

at December 31

2006 2005 2004

Asset Category

Domestic

Equity

35%

32-38% 39.0% 39.0%

International

Equity

20%

17-23% 19.6% 20.6%

Private

Equity 5% 0-8% .9% .6%

Total Equity 60% 59.5% 60.2%

Domestic

Fixed Income 30% 27-33% 30.7% 29.7%

High Yield

Fixed Income 5% 0-8% 6.7% 9.7%

Total Fixed

Income 35% 37.4% 39.4%

Real Estate 5% 0-8% 2.5%

Other 0% 0-1 % .6% .4%

Total 100% 100% 100%

The slight overweight in domestic equity at year-end 2005

and 2004 is attributable to the targeted allocation in Private

Equity, which continues to be committed but which is

funded over time as suitable opportunities for private equity

investment are identified and as calls for funding are made.

The Investment Policy Statement provides that, from time to

time, domestic equity may serve as a proxy (substitute) for

private equity. Additionally, target allocation changes,

which were effective November 29, 2005, included reducing

the High Yield Fixed Income allocation from 10% to 5%

and creating a new Real Estate allocation of 5%. It is

anticipated that this transition will be completed during

2006 as suitable investment opportunities become available.

We believe that, over the long term, asset allocation is the

single greatest determinant of risk. Asset allocation will

deviate from the target percentages due to market

movement, cash flows, and investment manager

performance. Material deviations from the asset allocation

targets can alter the expected return and risk of the Trust.

On the other hand, frequent rebalancing to the asset

allocation targets may result in significant transaction costs,

which can impair the Trust’ s ability to meet its investment

objective. Accordingly, the Trust portfolio is periodically

rebalanced to maintain asset allocation within the target

ranges described above.

In addition to being diversified across asset classes, the

Trust is diversified within each asset class. Secondary

diversification provides a reasonable basis for the

expectation that no single security or class of securities will

have a disproportionate impact on the total risk and return of

the Trust.