PNC Bank 2005 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2005 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

117

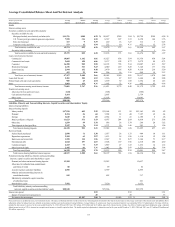

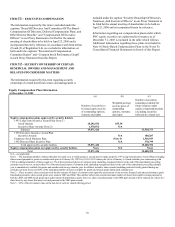

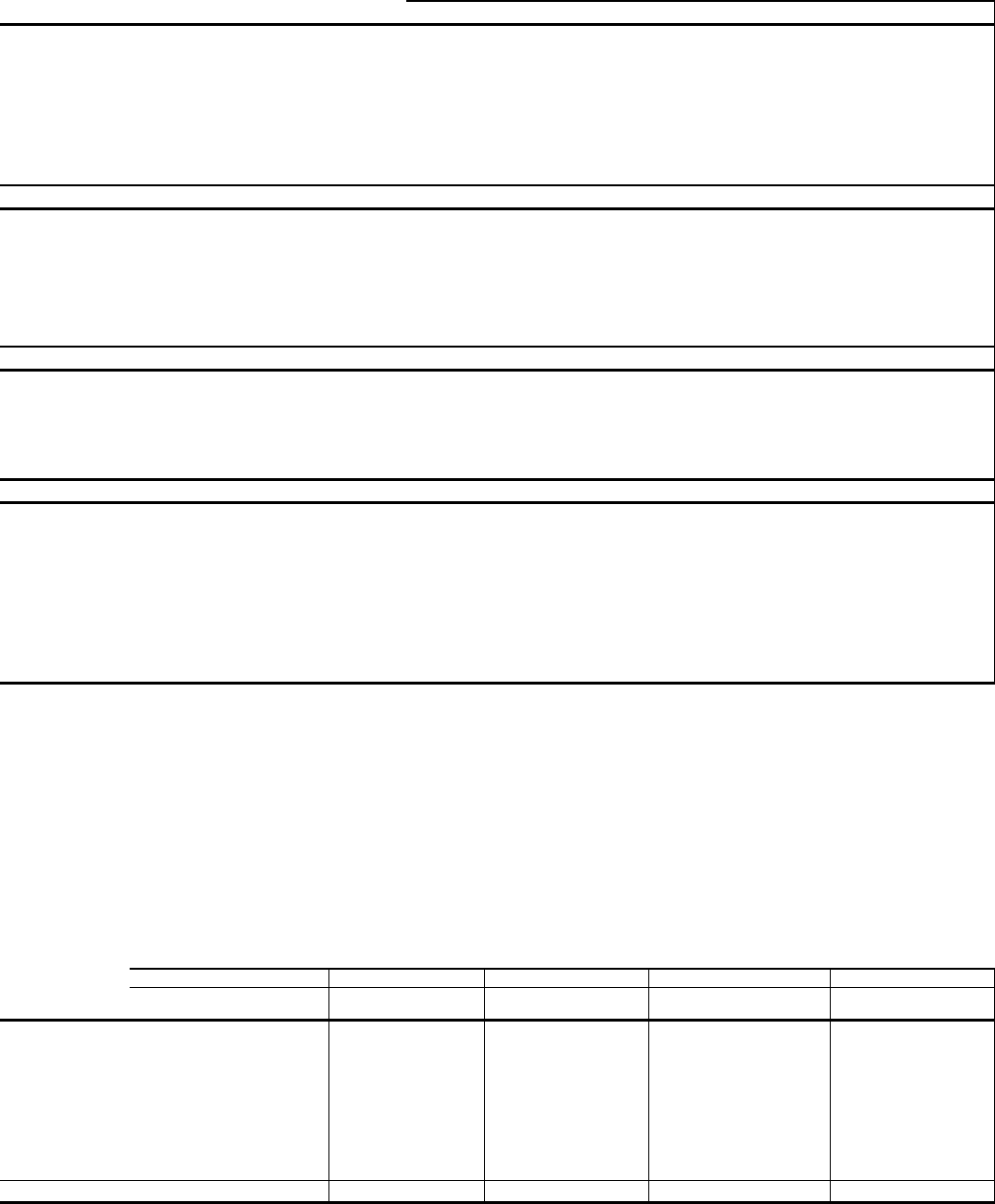

SUMMARY OF LOAN LOSS EXPERIENCE

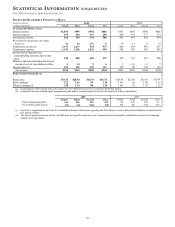

Year ended December 31 - dollars in millions 2005 2004 2003 2002 2001

Allowance for loan and lease losses at beginning of year $607 $632 $673 $560 $598

Charge-offs

Commercial (52) (113) (168) (194) (876)

Commercial real estate (1) (2) (3) (3) (37)

Consumer (45) (43) (39) (40) (42)

Residential mortgage (2) (3) (4) (5) (2)

Lease financing (29) (5) (46) (25) (28)

Total charge-offs (129) (166) (260) (267) (985)

Recoveries

Commercial (a) 82 31 32 26 17

Commercial real estate 1 1 1 1 1

Consumer 15 12 12 14 16

Residential mortgage 1 1 1 1

Lease financing 1 6 3 2 2

Total recoveries 99 51 49 44 37

Net charge-offs (a) (30) (115) (211) (223) (948)

Provision for credit losses 21 52 177 309 903

Acquisitions 23 22 41

Net change in allowance for unfunded loan

commitments and letters of credit (25) 16 (7) (14) 7

Allowance for loan and lease losses at end of year $596 $607 $632 $673 $560

Allowance as a percent of period-end

Loans 1.21%

1.40%

1.74% 1.90% 1.47%

Nonperforming loans 314 424 238 218 265

As a percent of average loans

Net charge-offs (a) (b) .06 .28 .59 .60 2.12

Provision for credit losses (c) .04 .13 .49 .83 2.01

Allowance for loan and lease losses 1.26 1.48 1.76 1.81 1.25

Allowance as a multiple of net charge-offs (a) (b) 19.87x 5.28x 3.00x 3.02x .59x

(a) Amounts for 2005 reflect the impact of a $53 million loan recovery in that year. Excluding this recovery, net charge-offs would have been .18% of average loans and the allowance

as a multiple of net charge-offs would have been 7.18x.

(b) Excluding $804 million of net charge-offs in 2001 related to the institutional lending repositioning initiative, net charge-offs would have been .32% of average loans and the

allowance as a multiple of net charge-offs would have been 3.89x.

(c) Excluding $714 million of provision in 2001 related to the institutional lending repositioning initiative, provision for credit losses would have been .42% of average loans.

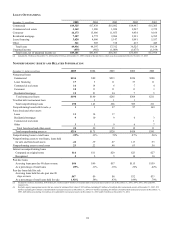

The following table presents the assignment of the allowance for loan and lease losses and the categories of loans as a percentage

of total loans. Changes in the allocation over time reflect the changes in loan portfolio composition, risk profile and refinements to

reserve methodologies. For purposes of this presentation, a portion of the allowance for loan and lease losses has been assigned to

loan categories based on the relative specific and pool allocation amounts to provide coverage for probable losses not covered in

specific, pool and consumer reserve methodologies related to qualitative and measurement factors. At December 31, 2005, the

portion of the reserves for these factors was $59 million.

ALLOCATION OF ALLOWANCE FOR LOAN AND LEASE LOSSES

2005

2004

2003

2002

2001

December 31

Dollars in millions

Allowance

Loans to

Total Loans

Allowance

Loans to

Total Loans Allowance

Loans to

Total Loans

Allowance

Loans to

Total Loans Allowance

Loans to

Total Loans

Commercial $489 39.2% $503 40.1% $514 41.5% $504 42.3% $392 40.0%

Commercial real

estate 32 6.4 26 4.5 34 5.1 52 6.4 63 6.3

Consumer

24

33.1

35

35.9

28

32.6

28

27.8

39

24.1

Residential

mortgage 7 14.9 6 11.0 7 8.0 10 11.0 8 16.8

Lease financing 41 5.7 33 7.3 44 11.4 75 11.3 53 11.6

Other 3 .7 4 1.2 5 1.4 4 1.2 5 1.2

Total $596 100.0% $607 100.0% $632 100.0% $673 100.0% $560 100.0%