PNC Bank 2005 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2005 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

36

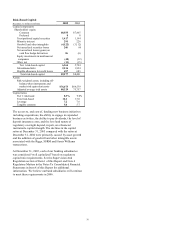

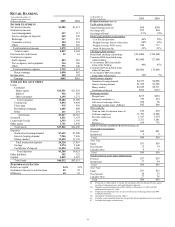

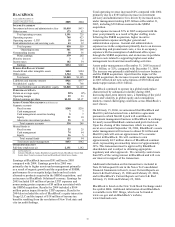

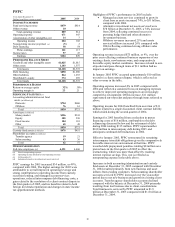

• Average residential mortgage loans increased $517

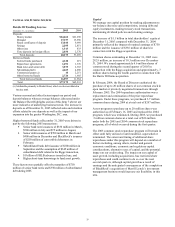

million, or 58%, primarily due to the addition of

loans from the greater Washington, D.C. area

acquisition. Payoffs in our existing portfolio, which

will continue throughout 2006, reduced the impact of

the additional loans acquired.

Growing core checking deposits as a lower cost-funding

source and as the cornerstone product to build customer

relationships are primary objectives of our deposit strategy.

Average total deposits increased $3.9 billion, or 10% ,

compared with 2004. The deposit growth was driven by

increases in the number of checking relationships (new

customer acquisition and the expansion into the greater

Washington, D.C. area) and the recapture of consumer

certificate of deposit balances as interest rates have risen.

During this rising rate environment, we expect the rate of

growth in demand deposit balances to be less than the rate of

growth for customer checking relationships. Additionally, we

expect to see customers shift their funds from lower interest-

bearing deposits to higher yielding deposits or investment

products. The shift was evident during the second half of 2005

and impacted the level of average demand deposits in that

period. Higher energy costs to consumers could also have a

negative impact on demand deposit balance growth.

• Average demand deposit growth of $909 million, or 6%,

was driven by a $229 million increase in the core business

due to continued growth in total checking relationships

and $680 million attributable to the expansion into the

greater Washington, D.C. area.

• Small business checking relationship retention has

improved. Consumer checking relationship retention

remains steady and strong due to increased penetration

rates of debit card, online banking and online bill

payment.

• Customer balances in other deposit products remained

consistent while certificates of deposits increased $2.5

billion. This increase was attributable to the rising

interest rate environment attracting customers back into

this product.

Assets under management of $49 billion at December 31,

2005 declined $1 billion compared with the balance at

December 31, 2004. The effects of comparatively higher

equity markets and the expansion into the greater Washington,

D.C. area were more than offset by net client asset outflows.

Net client asset outflows are the result of ordinary course

distributions from trust and investment management accounts

and account closures exceeding investment additions from

new and existing clients. The net outflows were primarily

related to a few significant low-margin clients.

Nondiscretionary assets under administration of $84 billion at

December 31, 2005 declined $9 billion compared with the

balance at December 31, 2004. The decline primarily reflects

the loss of two sizeable master custody accounts with minimal

earnings impact.

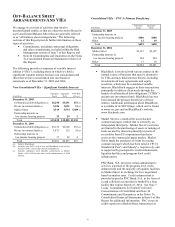

Retail Banking provides deposit, lending, cash management,

brokerage, investment management and trust, and private

banking products and services to 2.5 million customers within

our primary geographic area. Products and services offered to

our customers include:

• Checking accounts

• Savings, money market and certificates of deposit

• Personal and business loans

• Cash management, collection and payment services

• Brokerage and insurance services

• Personal and charitable trusts

• Executorships

• Employee benefit plans

• Investment management