PNC Bank 2005 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2005 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

|

|

44

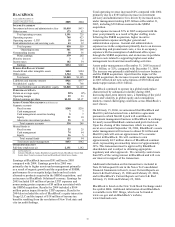

STATUS OF DEFINED BENEFIT

PENSION PLAN

We have a noncontributory, qualified defined benefit

pension plan ("plan" or "pension plan") covering eligible

employees. Retirement benefits are derived from a cash

balance formula based on compensation levels, age and

length of service. Pension contributions are based on an

actuarially determined amount necessary to fund total

benefits payable to plan participants. Plan assets are

currently approximately 60% invested in equity investments

with most of the remainder invested in fixed income

instruments. Plan fiduciaries determine and review the

plan’ s investment policy.

We calculate the expense associated with the pension plan

in accordance with SFAS 87, "Employers' Accounting for

Pensions," and we use assumptions and methods that are

compatible with the requirements of SFAS 87, including a

policy of reflecting trust assets at their fair market value. On

an annual basis, we review the actuarial assumptions related

to the pension plan, including the discount rate, rate of

compensation increase and the expected return on plan

assets. Neither the discount rate nor the compensation

increase assumptions significantly affect pension expense.

The expected long-term return on assets assumption does

significantly affect pension expense. We intend to decrease

the expected long-term return on plan assets assumption

from the 8.5% used for 2005 to 8.25% for determining net

periodic cost for 2006. Also, under current accounting rules,

the difference between expected long-term returns and

actual returns are accumulated and amortized to pension

expense over future periods. Each one percentage point

difference in actual return compared with our expected

return causes expense in the following year to change by up

to $3 million.

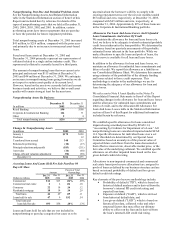

The table below reflects the estimated effects on pension

expense of certain changes in assumptions, using 2006

estimated expense as a baseline.

Change in Assumption

Estimated

Increase to 2006

Pension

Expense

(In millions)

.5% decrease in discount rate $2

.5% decrease in expected long-term return

on assets

8

.5% increase in compensation rate 1

We currently estimate a pretax pension benefit of $1 million

in 2006 compared with a pretax benefit of $8 million in

2005.

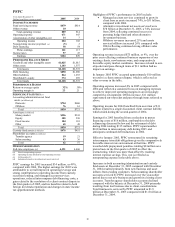

In accordance with SFAS 87 and SFAS 132 (Revised 2003),

"Employers' Disclosures about Pensions and Other

Postretirement Benefits," we may have to eliminate any

prepaid pension asset and recognize a minimum pension

liability if the accumulated benefit obligation exceeds the

fair value of plan assets at year-end. We would recognize

the corresponding charge as a component of other

comprehensive income and it would reduce total

shareholders' equity, but it would not affect net income. At

December 31, 2005, the fair value of plan assets was $1.627

billion, which exceeded the accumulated benefit obligation

of $1.232 billion. The status at year-end 2006 will depend

primarily upon 2006 investment returns and the level of

contributions, if any, we make to the plan during 2006.

Plan asset investment performance has the most impact on

contribution requirements. However, contribution

requirements are not particularly sensitive to actuarial

assumptions. Investment performance will drive the amount

of permitted contributions in future years. Also, current law

sets limits as to both minimum and maximum contributions

to the plan. In any event, any large near-term contributions

to the plan will be at our discretion, as we expect that the

minimum required contributions under the law will be

minimal or zero for several years.

During the second quarter of 2005, we acquired a frozen

defined benefit pension plan as a result of the Riggs

acquisition. Plan assets and projected benefit obligations of

the Riggs plan were approximately $107 million and $116

million, respectively, at acquisition date. The $9 million

funding deficit was recognized as part of the Riggs

acquisition purchase price allocation. For determining

contribution amounts to the plan, deficits are calculated

using ERISA-mandated rules, and on this basis we

contributed approximately $16 million to the Riggs plan

during the third quarter of 2005. We integrated the Riggs

plan into the PNC plan on December 30, 2005.

We maintain other defined benefit plans that have a less

significant effect on financial results, including various

nonqualified supplemental retirement plans for certain

employees. See Note 17 Employee Benefit Plans in the

Notes To Consolidated Financial Statements in Item 8 of

this Report for additional information.

RISK MANAGEMENT

We encounter risk as part of the normal course of our

business and we design risk management processes to help

manage these risks. This Risk Management section first

provides an overview of the risk measurement, control

strategies, and monitoring aspects of our corporate-level risk

management processes. Following that discussion is an

analysis of the risk management process for what we view

as our primary areas of risk: credit, operational, liquidity,

and market. The discussion of market risk is further

subdivided into interest rate, trading, and equity and other

investment risk areas. Our use of financial derivatives as

part of our overall asset and liability risk management

process is also addressed within the Risk Management

section of this Item 7. In appropriate places within this

section, historical performance is also addressed.

OVERVIEW

As a financial services organization, we take a certain

amount of risk in every business decision. For example,

every time we open an account or approve a loan for a

customer, process a payment, hire a new employee, or

implement a new computer system, we incur a certain

amount of risk. As an organization, we must balance

revenue generation and profitability with the risks

associated with our business activities. Risk management is

not about eliminating risks, but about identifying and

accepting risks and then effectively managing them so to

optimize shareholder value.