IBM 2008 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2008 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

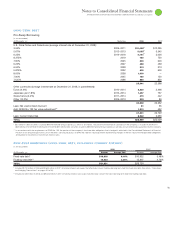

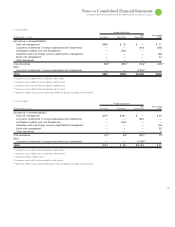

Notes to Consolidated Financial Statements

INTERNATIONAL BUSINESS MACHINES CORPORATION and Subsidiary Companies

counterparties. These arrangements permit the company to net

amounts due from the company to a counterparty with amounts due

to the company from a counterparty reducing the maximum loss

from credit risk in the event of counterparty default.

The company employs derivative instruments to hedge the vola-

tility in stockholders’ equity resulting from changes in currency

exchange rates of significant foreign subsidiaries of the company with

respect to the U.S. dollar. These instruments, designated as net

investment hedges in accordance with SFAS No. , expose the

company to liquidity risk as the derivatives have an immediate cash

flow impact upon maturity which is not offset by the translation of

the underlying hedged equity. The company monitors the cash loss

potential on an ongoing basis and may discontinue some of these

hedging relationships by de-designating the derivative instrument to

manage this liquidity risk. Although not designated as accounting

hedges, the company may utilize derivatives to offset the changes in

fair value of the de-designated instruments from the date of de-des-

ignation until maturity. The company expended $ million and $

million related to maturities of derivative instruments that existed in

qualifying net investment hedge relationships in and ,

respectively. At December , , the company had net liabilities of

$ million, representing the fair value of derivative instruments in

qualifying net investment hedge relationships. Of this amount, $

million is expected to mature in fiscal . In addition, at December

, , the company had net liabilities of $ million, represent-

ing the fair value of derivative instruments that were designated in

qualifying net investment hedging relationships as of December ,

, but were subsequently de-designated in fiscal . This

amount will fully mature in fiscal . At December , the

weighted-average remaining maturity of all derivative instruments

designated as net

investment hedges was approximately . years as

compared to . years

at December , .

In its hedging programs, the company uses forward contracts,

futures contracts, interest-rate swaps and currency swaps, depend-

ing upon the underlying exposure.

A brief description of the major hedging programs follows.

The company issues debt in the global capital markets, principally to

fund its financing lease and loan portfolio. Access to cost-effective

financing can result in interest rate and/or currency mismatches with

the underlying assets. To manage these mismatches and to reduce

overall interest cost, the company uses interest-rate swaps to convert

specific fixed-rate debt into variable-rate (or “floating-rate”) debt

(i.e., fair value hedges) and to convert specific variable-rate debt into

fixed-rate debt (i.e., cash flow hedges).

The company is exposed to exchange rate volatility on foreign

currency denominated debt. To manage this risk, the company

employs cross-currency swaps to convert fixed-rate foreign currency

denominated debt to fixed-rate debt denominated in the functional

currency of the borrowing entity. These swaps are accounted for as

cash flow hedges.

The company is exposed to interest rate volatility on forecasted

debt issuances. To manage this risk, the company may use forward

starting interest-rate swaps to lock in a portion of the rate on the

interest payments related to the forecasted debt issuance. These

swaps are accounted for as cash flow hedges.

At December , and , the weighted-average remaining

maturity of all swaps in the debt risk management program was

approximately five years.

-

( )

A significant portion of the company’s foreign currency denominated

debt portfolio is designated as a hedge of net investment which

reduces the volatility in stockholders’ equity caused by changes in

foreign currency exchange rates in the functional currency of major

foreign subsidiaries with respect to the U.S. dollar. The company also

uses cross-currency interest rate swaps and foreign exchange forward

contracts for this risk management purpose. The currency effects of

these hedges (approximately $ million losses in , $ mil-

lion losses in and $ million losses in , net of tax) were

reflected in accumulated gains and

(l

osses) not affecting retained

earnings within the Consolidated Statement of Stockholders’ Equity,

thereby offsetting a portion of the translation adjustment of the

applicable foreign subsidiaries’ net assets.

The company’s operations generate significant nonfunctional cur-

rency, third-party vendor payments and intercompany payments

for royalties and goods and services among the company’s non-U.S.

subsidiaries and with the parent company. In anticipation of these

foreign currency cash flows and in view of the volatility of the cur-

rency markets, the company selectively employs foreign exchange

forward contracts to manage its currency risk. These forwards are

accounted for as cash flow hedges. The maximum length of time

over which the company is hedging its exposure to the variability

in future cash flows is approximately four years. At December ,

, the weighted-average remaining maturity of these derivative

instruments was approximately days as compared to days at

December , .