Vodafone 2015 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2015 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

Overview Strategy review Performance Governance Financials Additional information Vodafone Group Plc

Annual Report 2015

39

Acquisition integration

We commenced integration of KDG in April

2014 and of Ono in August 2014. In total

we expect to generate combined annual

cost and capex synergies of approximately

€540 million in the 2018 nancial year, mainly

from migrating xed and mobile customers

onto our own infrastructure and combining

backhaul and core networks.

In terms of standalone business performance,

KDG has continued to grow strongly and

even showed some acceleration through the

year, supported by rm pricing and improved

subscriber growth. Ono’s performance has

been a little below expectations, with ARPU

coming under more pressure than anticipated

as a result of aggressive pricing at the premium

end of the market.

The teams have made solid progress on all

aspects of integration. In Germany, we have

started to connect Vodafone base station sites

to KDG bre backhaul, and have migrated

77,000 customers to date off our DSL platform

(on which we pay high monthly fees) onto

KDG’s cable infrastructure. 70% of IP trafc has

now been combined, and we have launched

our combined xed/mobile proposition, “All

in One”.

In Spain, we have so far connected over

500 mobile base station sites to Ono’s bre

to save on backhaul costs. We also signed

an agreement with Telefónica, the host

of Ono’s MVNO, to accelerate the migration

of trafc to our own network. We are launching

a truly integrated, single-billed, xed/mobile

proposition this summer.

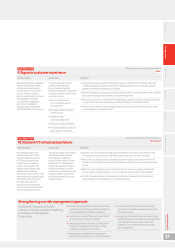

EBITDA £ billion

11.5

2013 2014 2015

11.1 11.9

0

5

10

15

Free cash ow and £ billion

ordinary dividends paid

4.8

5.7

2013 2014 2015

4.4

5.1

1.1

2.9

0

4

2

6

Free cash ow Dividend

Cost efciency

Progress on costs was good this year, with

operating costs in Europe at in organic terms,

despite the cost growth driven by the Project

Spring network roll-out. Savings came from

further development of our shared services

platform, increased centralised procurement,

headcount reductions and other efciencies.

Looking ahead, for a relatively lean

organisation such as Vodafone, a pure focus

on “cost cutting” can be an over-simplistic

approach that could compromise the quality

of service we provide to customers, which

would clearly be self-defeating.

Instead, we are looking at cost in two ways

which can make a signicant long term

difference to our overall efciency. First, we are

focusing on productivity improvements –

doing the same things better at a lower cost,

by developing cross-functional programmes

and benchmarking more forensically between

different parts of the business. In some cases,

this will require us to invest more in the short

term – for example, in new, standardised

IT systems – to deliver transformational

efciencies longer term.

Second, we are embedding a stronger

cost-conscious culture at an individual level

throughout the business, including personal

objectives on efciency targets for senior

management incentives. Both of these

elements will be underpinned by more

granular and consistent cost and productivity

reporting across markets and functions.

We have instigated a programme called “Fit

for Growth” to encompass both of these

objectives, and to develop an organisation with

improved competitiveness and agility for the

long term.

Performance against 2015

nancial year guidance

Based on guidance foreign exchange rates,

our EBITDA was £11.7 billion, within our

guidance range of £11.3 billion to £11.9 billion

set in May 2014, and our range of £11.6 billion

to £11.9 billion set in November 2014. On the

same basis our free cash ow was £1.3 billion,

in line with our guidance of positive free

cash ow.

Looking ahead

The key goals for the year ahead are to build

on the improving commercial execution

evident last year, and to complete the

second half of the Project Spring programme

as successfully as the rst half. We expect

EBITDA to be in the range of £11.5 billion

to £12.0 billion1, with further tight control

on costs and good progress on the integration

of our cable acquisitions. We expect free cash

ow to be positive1 even after the second

year of elevated Project Spring capex, giving

us condence that we will return to a dividend

that is comfortably covered by free cash ow

when capex returns to more normal levels

in future years.

Nick Read

Chief Financial Ofcer

Note:

1 Guidance for the 2016 nancial year is based on our

current assessment of the global macroeconomic

outlook and assumes foreign exchange rates of £1:€1.37,

£1:INR95.2, £1:ZAR18.1. It excludes the impact of licences

and spectrum purchases, material one-off tax-related

payments, restructuring costs and any fundamental

structural changes to the eurozone. It also assumes

no material change to the current structure of the Group.