Vodafone 2015 Annual Report Download - page 195

Download and view the complete annual report

Please find page 195 of the 2015 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

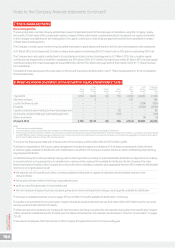

Additional tax considerations

UK inheritance tax

An individual who is domiciled in the US (for the purposes of the

Estate Tax Convention) and is not a UK national will not be subject

to UK inheritance tax in respect of our shares or ADSs on the

individual’s death or on a transfer of the shares or ADSs during the

individual’s lifetime, provided that any applicable US federal gift or estate

tax is paid, unless the shares or ADSs are part of the business property

of a UK permanent establishment or pertain to a UK xed base used for

the performance of independent personal services. Where the shares

or ADSs have been placed in trust by a settlor they may be subject

to UK inheritance tax unless, when the trust was created, the settlor

was domiciled in the US and was not a UK national. Where the shares

or ADSs are subject to both UK inheritance tax and to US federal gift

or estate tax, the estate tax convention generally provides a credit

against US federal tax liabilities for UK inheritance tax paid.

UK stamp duty and stamp duty reserve tax

Stamp duty will, subject to certain exceptions, be payable on any

instrument transferring our shares to the custodian of the depositary

at the rate of 1.5% on the amount or value of the consideration if on sale

or on the value of such shares if not on sale. Stamp duty reserve tax

(‘SDRT’), at the rate of 1.5% of the price or value of the shares, could also

be payable in these circumstances and on issue of our shares to such

a person but no SDRT will be payable if stamp duty equal to such SDRT

liability is paid.

A ruling by the European Court of Justice has determined that the

1.5% SDRT charge on issue of shares to a clearance service is contrary

to EU law. As a result of that ruling, HMRC indicated that where new

shares are rst issued to a clearance service or to a depositary within

the EU, the 1.5% SDRT charge will not be levied. Subsequently,

a decision by the rst-tier tax tribunal in the UK extended this ruling

to the issue of shares (or, where it is integral to the raising of new capital,

the transfer of shares) to depositary receipts systems wherever located.

HMRC have stated that they will not seek to appeal this decision

and, as such, will no longer seek to impose 1.5% SDRT on the issue

of shares (or, where it is integral to the raising of new capital, the transfer

of shares) to a clearance service or to a depositary, wherever located.

Investors should, however, be aware that this area may be subject

to further developments in the future.

No stamp duty will be payable on any transfer of our ADSs provided

that the ADSs and any separate instrument of transfer are executed and

retained at all times outside the UK. A transfer of our shares in registered

form will attract ad valorem stamp duty generally at the rate of 0.5%

of the purchase price of the shares. There is no charge to ad valorem

stamp duty on gifts.

SDRT is generally payable on an unconditional agreement to transfer

our shares in registered form at 0.5% of the amount or value of the

consideration for the transfer, but is repayable if, within six years of the

date of the agreement, an instrument transferring the shares is executed

or, if the SDRT has not been paid, the liability to pay the tax (but not

necessarily interest and penalties) would be cancelled. However,

an agreement to transfer our ADSs will not give rise toSDRT.

PFIC rules

We do not believe that our shares or ADSs will be treated as stock

of a PFIC for US federal income tax purposes. This conclusion

is a factual determination that is made annually and thus is subject

to change. If we are treated as a PFIC, any gain realised on the sale

or other disposition of the shares or ADSs would in general not

be treated as capital gain unless a US holder elects to be taxed

annually on a mark-to-market basis with respect to the shares or ADSs.

Otherwise a US holder would be treated as if he or she has realised

such gain and certain “excess distributions” rateably over the holding

period for the shares or ADSs and would be taxed at the highest tax rate

in effect for each such year to which the gain was allocated. An interest

charge in respect of the tax attributable to each such year would also

apply. Dividends received from us would not be eligible for the reduced

rate of tax described above under “Taxation of Dividends – US federal

income taxation”.

Backup withholding and information reporting

Payments of dividends and other proceeds to a US holder with respect

to shares or ADSs, by a US paying agent or other US intermediary will

be reported to the Internal Revenue Service (‘IRS’) and to the US holder

as may be required under applicable regulations. Backup withholding

may apply to these payments if the US holder fails to provide

an accurate taxpayer identication number or certication of exempt

status or fails to comply with applicable certication requirements.

Certain US holders are not subject to backup withholding. US holders

should consult their tax advisers about these rules and any other

reporting obligations that may apply to the ownership or disposition

of shares or ADSs, including requirements related to the holding

of certain foreign nancial assets.

Overview Strategy review Performance Governance Financials Additional

information Vodafone Group Plc

Annual Report 2015

193