Nokia 2010 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2010 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

|

|

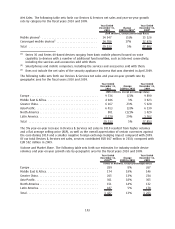

Business Combinations

We apply the acquisition method of accounting to account for acquisitions of businesses. The

consideration transferred in a business combination is measured as the aggregate of the fair values of

the assets transferred, liabilities incurred towards the former owners of the acquired business and

equity instruments issued. Acquisitionrelated costs are recognized as expense in profit and loss in

the periods when the costs are incurred and the related services are received. Identifiable assets

acquired and liabilities assumed are measured separately at their fair value as of the acquisition date.

Noncontrolling interests in the acquired business are measured separately based on their

proportionate share of the identifiable net assets of the acquired business. The excess of the cost of

the acquisition over our interest in the fair value of the identifiable net assets acquired is recorded as

goodwill.

The determination and allocation of fair values to the identifiable assets acquired and liabilities

assumed is based on various assumptions and valuation methodologies requiring considerable

management judgment. The most significant variables in these valuations are discount rates, terminal

values, the number of years on which to base the cash flow projections, as well as the assumptions

and estimates used to determine the cash inflows and outflows. Management determines the

discount rates to be used based on the risk inherent in the related activity’s current business model

and industry comparisons. Terminal values are based on the expected life of products and forecasted

life cycle and forecasted cash flows over that period. Although we believe that the assumptions

applied in the determination are reasonable based on information available at the date of

acquisition, actual results may differ from the forecasted amounts and the difference could be

material.

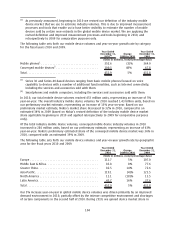

Valuation of Longlived Assets, Intangible Assets and Goodwill

We assess the carrying amount of identifiable intangible assets and longlived assets if events or

changes in circumstances indicate that such carrying amount may not be recoverable. We assess the

carrying amount of our goodwill at least annually, or more frequently based on these same

indicators. Factors we consider important, which could trigger an impairment review, include the

following:

• significant underperformance relative to historical or projected future results;

• significant changes in the manner of our use of these assets or the strategy for our overall

business; and

• significantly negative industry or economic trends.

When we determine that the carrying amount of intangible assets, longlived assets or goodwill may

not be recoverable based upon the existence of one or more of the above indicators of impairment,

we measure any impairment based on discounted projected cash flows.

This review is based upon our projections of anticipated discounted future cash flows. The most

significant variables in determining cash flows are discount rates, terminal values, the number of

years on which to base the cash flow projections, as well as the assumptions and estimates used to

determine the cash inflows and outflows. Management determines discount rates to be used based

on the risk inherent in the related activity’s current business model and industry comparisons.

Terminal values are based on the expected life of products and forecasted life cycle and forecasted

cash flows over that period. While we believe that our assumptions are appropriate, such amounts

estimated could differ materially from what will actually occur in the future. In assessing goodwill,

these discounted cash flows are prepared at a cash generating unit level. Amounts estimated could

differ materially from what will actually occur in the future.

Goodwill is allocated to the Group’s cashgenerating units (CGU) and discounted cash flows are

prepared at CGU level for the purpose of impairment testing. The allocation of goodwill to our CGUs is

made in a manner that is consistent with the level at which management monitors operations and

96