Nokia 2010 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2010 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

|

|

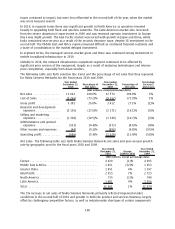

America and consumer trend towards the purchase of lowerend car classes. The following table sets

forth NAVTEQ net sales by geographic area for the fiscal year 2009 and for the period from July 10,

2008 to December 31, 2008.

For the Year Ended

December 31,

2009

From July 10 to

December 31,

2008

(EUR millions) (EUR millions)

Europe ................................................. 312 158

Middle East & Africa ....................................... 29 29

Greater China ............................................ 5 2

AsiaPacific .............................................. 18 10

North America ........................................... 293 155

Latin America ............................................ 13 7

Total . .................................................. 670 361

For the fiscal year 2009, NAVTEQ gross profit was EUR 582 million compared with EUR 318 million for

the period from July 10, 2008 to December 31, 2008. Gross profit reflects net sales, partially offset by

costs related to the delivery of NAVTEQ’s database information to its customers.

NAVTEQ R&D expenses in 2009 were EUR 653 million compared with EUR 332 million for the period

from July 10, 2008 to December 31, 2008. NAVTEQ R&D expenses included amortization of intangible

assets recorded as part of Nokia’s acquisition of NAVTEQ totaling EUR 346 million and EUR 171 million

in 2009 and 2008, respectively. R&D expenses were also driven by increased investment in NAVTEQ’s

map database related to geographic expansion and quality improvements. R&D expenses represented

97.5% of NAVTEQ net sales in 2009 compared to 92.0% of NAVTEQ net sales in 2008.

NAVTEQ selling and marketing expenses in 2009 were EUR 217 million compared with EUR 109 million

for the period from July 10, 2008 to December 31, 2008. NAVTEQ selling and marketing expenses

primarily consisted of amortization of intangible assets recorded as part of Nokia’s acquisition of

NAVTEQ totaling EUR 115 million and EUR 57 million in 2009 and 2008, respectively. Selling and

marketing expenses were also driven by investments to grow NAVTEQ’s worldwide sales force and

expand the breadth of its product offerings. Selling and marketing expenses represented 32.4% of

NAVTEQ net sales in 2009 compared to 30.2% of NAVTEQ net sales in 2008.

NAVTEQ operating loss in 2009 was EUR 344 million, with an operating margin of negative 51.3%

compared with operating loss of EUR 153 million and with an operating margin of negative 42.4% for

the period from July 10, 2008 to December 31, 2008. The operating loss in both periods was primarily

the result of the amortization of intangible assets recorded as part of Nokia’s acquisition of NAVTEQ,

which was partially offset by profits from NAVTEQ’s ongoing business.

Nokia Siemens Networks

According to our estimates, the mobile infrastructure market declined by about 5% in euro terms in

2009 compared to 2008 with the trend varying, depending on region. The primary cause of the

decline was the deterioration in global economic conditions, which caused many operators to delay

investments in network infrastructure. In many markets, this was characterized by caution on the part

of operators concerned about enduser behavior and subsequent declining revenues, but in certain

markets, including parts of Asia Pacific, Middle East and Africa and Eastern Europe, restricted access to

financing resulted in capital expenditures being cancelled. The emerging professional services

segment also continued to grow as operators sought efficiencies for their network through

outsourcing network management to infrastructure vendors. The mobile infrastructure market was

characterized by a decline in investment in 2G networks which was not offset by continued

investment in 3G. One exception was China, where investment in 3G rollouts resulted in growth in

that market. Globally, the network infrastructure equipment segment continued to be affected by

115