Nokia 2010 Annual Report Download - page 265

Download and view the complete annual report

Please find page 265 of the 2010 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275

|

|

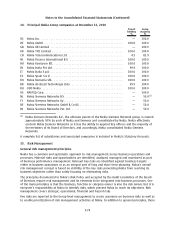

35. Risk Management (Continued)

At the reporting date, the interest rate profile of the Group’s interestbearing assets and liabilities is

presented in the table below:

Fixed rate Floating rate Fixed rate Floating rate

2010 2009

EURm EURm EURm EURm

Assets .................................... 8795 3588 5 712 3 241

Liabilities .................................. (4 156) (992) (3 771) (1 403)

Assets and liabilities before derivatives .......... 4 639 2 596 1 941 1 838

Interest rate derivatives ...................... 1 036 (994) 1 628 (1 693)

Assets and liabilities after derivatives ........... 5 675 1 602 3 569 145

Equity price risk

Nokia is exposed to equity price risk as the result of market price fluctuations in the listed equity

instruments held mainly for strategic business reasons.

Nokia has certain strategic noncontrolling investments in publicly listed equity shares. The fair value

of the equity investments which are subject to equity price risk at December 31, 2010 was

EUR 8 million (EUR 8 million in 2009). In addition, Nokia invests in private equity through venture

funds, which, from time to time, may have holdings in equity instruments which are listed in stock

exchanges. These investments are classified as availableforsale carried at fair value. See Note 16 for

more details on availableforsale investments.

Due to the insignificant amount of exposure to equity price risk, there are currently no outstanding

derivative financial instruments designated as hedges for these equity investments.

Nokia is exposed to equity price risk on social security costs relating to its equity compensation plans.

Nokia mitigates this risk by entering into cash settled equity option contracts.

ValueatRisk

Nokia uses the ValueatRisk (VaR) methodology to assess the Group exposures to foreign exchange

(FX), interest rate, and equity risks. The VaR gives estimates of potential fair value losses in market

risk sensitive instruments as a result of adverse changes in specified market factors, at a specified

confidence level over a defined holding period.

In Nokia the FX VaR is calculated with the Monte Carlo method, which simulates random values for

exchange rates in which the Group has exposures and takes the nonlinear price function of certain FX

derivative instruments into account. The variancecovariance methodology is used to assess and

measure the interest rate risk and equity price risk.

The VaR is determined by using volatilities and correlations of rates and prices estimated from a one

year sample of historical market data, at 95% confidence level, using a onemonth holding period. To

put more weight on recent market conditions, an exponentially weighted moving average is

performed on the data with an appropriate decay factor.

This model implies that within a onemonth period, the potential loss will not exceed the VaR

estimate in 95% of possible outcomes. In the remaining 5% of possible outcomes, the potential loss

will be at minimum equal to the VaR figure, and on average substantially higher.

The VaR methodology relies on a number of assumptions, such as, a) risks are measured under

average market conditions, assuming that market risk factors follow normal distributions; b) future

F77

Notes to the Consolidated Financial Statements (Continued)