MoneyGram 2008 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2008 MoneyGram annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

|

|

Table of Contents

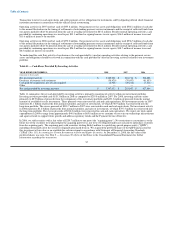

• credit rating downgrades on both our investment and the underlying collateral to the investment;

• extent of unrealized loss and the length of time the investment has been in an unrealized loss position;

• failure of structured investments to meet minimum coverage or collateralization tests;

• new information regarding the investment or the issuer;

• deterioration in the market, industry or geographical area relevant to the issuer or underlying collateral; and

• our ability and intent to hold the investment for a time sufficient to either receive all contractual cash flows or for the investment to

recover to its amortized cost.

As we have an available-for-sale investment portfolio and generally do not utilize our portfolio for liquidity purposes, we believe that our

intent and ability to hold an investment and the ability of the investment to generate cash flows are the primary factors in assessing

whether an investment in an unrealized loss position is other-than-temporarily impaired. If we no longer have the intent or ability to hold

the investment to maturity or call, and it is probable that the investment will not provide all of its contractual cash flows, then we believe

an investment in an unrealized loss position is other-than-temporarily impaired. In assessing our intent and ability, we evaluate our needs

under regulatory and contractual requirements, changes to our investment strategy and anticipated cash flow needs, including any

anticipated customer contract terminations.

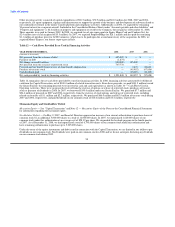

Derivative Financial Instruments — Derivative financial instruments are used as part of our risk management strategy to manage

exposure to fluctuations in foreign currency rates and interest rates. We do not enter into derivatives for speculative purposes. Derivatives

are accounted for in accordance with SFAS No. 133, Accounting for Derivative Instruments and Hedging Activities, and its related

amendments and interpretations. The derivatives are recorded as either assets or liabilities on the balance sheet at fair value, with the

change in fair value recognized in earnings or in other comprehensive income depending on the use of the derivative and whether it

qualifies for hedge accounting. A derivative that does not qualify, or is not designated, as a hedge will be reflected at fair value, with

changes in value recognized through earnings. The estimated fair value of derivative financial instruments has been determined using

available market information and certain valuation methodologies.

Considerable judgment is required in interpreting market data to develop the estimates of fair value. Accordingly, the estimates

determined may not be indicative of the amounts that could be realized in a current market exchange. The use of different market

assumptions or valuation methodologies may have a material effect on the estimated fair value amounts.

In the second quarter of 2008, the Company terminated all of its interest rate swaps and recognized a $29.7 million loss in earnings. As of

December 31, 2008, we had $0.8 million of unrealized gains on derivative financial instruments recorded in "Accumulated other

comprehensive loss," all of which related to forward currency agreements. While we intend to continue to meet the conditions to qualify

for hedge accounting treatment under SFAS No. 133, if hedges did not qualify as highly effective or if forecasted transactions are no

longer probable of occurring or did not occur, the changes in the fair value of the derivatives used as hedges would be reflected in

earnings. We do not believe we are exposed to more than a nominal amount of credit risk in our hedging activities as the counterparties

are generally well-established, well-capitalized financial institutions.

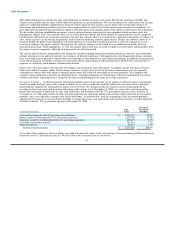

Goodwill — SFAS No. 142, Goodwill and Other Intangible Assets, requires annual impairment testing of goodwill based on the

estimated fair value of our reporting units, as well as testing whenever an impairment indicator is identified. The fair value of our

reporting units is estimated based on discounted expected future cash flows using a weighted average cost of capital rate. Additionally, an

assumed terminal value is used to project future cash flows beyond base years. Assumptions used in our impairment evaluations, such as

forecasted growth rates and our cost of capital, are consistent with our internal forecasts and operating plans. The estimates and

assumptions regarding expected cash flows, terminal values and the discount rate require considerable judgment and are based on

historical experience, financial forecasts and industry trends and conditions. If the growth rate for our reporting units with goodwill

assigned decreases by 50 basis points from the growth rates used in the 2008 valuation, fair value would be reduced by approximately

$35.7 million, assuming all other components of the fair value estimate remain unchanged. If the discount rate for our reporting units

with goodwill assigned increases by 50 basis points from

67